Editor’s Note — This article is sponsored by Chime. As with all sponsored content in Fintech Takes, this article was written, edited, and published by me, Alex Johnson. I hope you enjoy it!

As I am fond of saying around here, you are your business model.

Companies can talk all they want about their mission — about financial inclusion, customer empowerment, or building the future of money. But over the long term, what they actually end up doing is always a function of the incentives embedded in how they make money.

If you want to understand how a financial services company will behave, don’t read the marketing copy. Study the business model.

And in financial services, the dominant business model, by far, is net interest margin.

At its core, net interest margin (NIM) is incredibly simple: take in deposits at one rate, lend them out at a higher rate, and keep the spread.

That simplicity creates an equally simple incentive: maximize the spread. Keep lending rates as high as you can for as long as you can. Keep deposit rates as low as you can for as long as you can. That’s it.

This isn’t malicious. It’s not some grand conspiracy. It’s just the natural order of things — like a tiger hunting, killing, and eating a deer. The tiger isn’t evil. It’s just doing what it’s wired to do.

Banks are wired to maximize NIM.

The Hidden Cost of Multi-product Bundles

One of the more interesting downstream effects of business models in financial services is how they shape product strategy.

Financial services companies love constructing business models around multi-product bundles.

Net interest margin in banking is a textbook example.

Deposits are the raw material. Lending is the profit engine.

That dynamic has a predictable outcome: banks invest heavily in the parts of the bundle that make money and underinvest in the parts that don’t.

Look at lending. Over the past couple of decades, banks have invested tremendously in their lending products and processes, reducing friction for customers and increasing the sophistication of their risk underwriting and pricing in order to deliver more competitive offerings for their customers.

Now look at deposits.

Most bank checking accounts are basically the same. As Ron Shevlin puts it, they are “paycheck motels,” temporary places for your money to go before it is rerouted to more valuable destinations.

Minimal differentiation. Minimal innovation. Minimal strategic focus.

And you can see how banks think about deposits in moments of competition. When they need to gain share, they don’t invest in building new, more competitive deposit and payment products.

They just raise rates and attract hot money.

Because deposits aren’t the business. They’re the input to the business.

Is This What Customers Actually Want?

Here’s the question we should constantly ask in financial services: Is this what customers actually want?

Are generic checking accounts and persistently below-market savings accounts what customers want? Is the trade-off that banks have made on the business model side (deposits as an undifferentiated input, loans as the differentiated customer solution) the same trade-off that consumers would pick if we gave them the choice?

The only way to know the answer to these questions is to offer consumers a different choice and watch how they respond to it.

Fortunately, consumer fintech companies have done exactly that, and the early results are telling.

According to JD Power’s most recent research on deposit and investment account growth, fintech brands are attracting and converting new customers at higher rates than traditional banks.

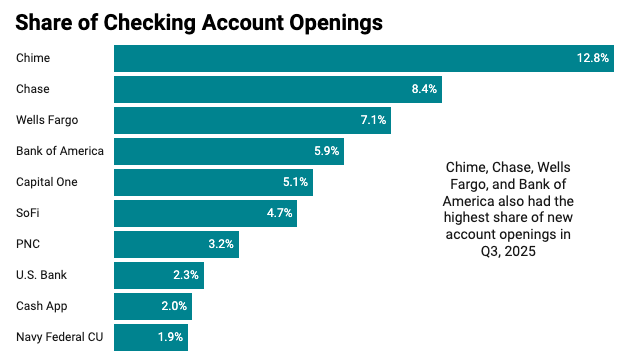

In Q4 of 2025, Chime claimed the largest share of new checking account openings with 12.8%. It was followed by Chase (8.4%) and Wells Fargo (7.1%):

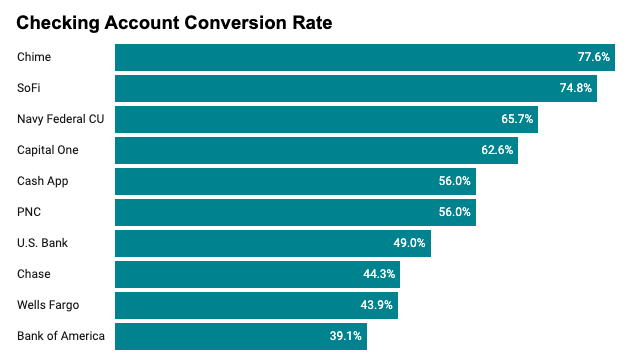

Interestingly, the success of Chime and other fintech brands was not solely due to the marketing dollars they spent to fill up the tops of their acquisition funnels. According to JD Power, their conversion rate — the percentage of customers who chose them from the set of products they were considering — was significantly better than the big banks:

Now, to be fair, the success of fintech brands in winning new customers is not universal.

Chase earned the highest share of new savings account customers in Q4 (Chime was number two). And when JD Power sliced the new account checking and deposit account openings in Q4 by wealth, it found that the big banks did better with mass affluent and affluent segments (those making more than $150,000), while Chime outperformed among mass market consumers (those making less than $150,000).

Room For New Models

Importantly, consumer fintech companies aren’t just offering different products; they’re operating on different business models. Some, like Chime, are built around fee-free, payments-driven engagement; others monetize through entirely different levers. Klarna, for example, is merchant-funded, so its product is designed to drive conversion at checkout.

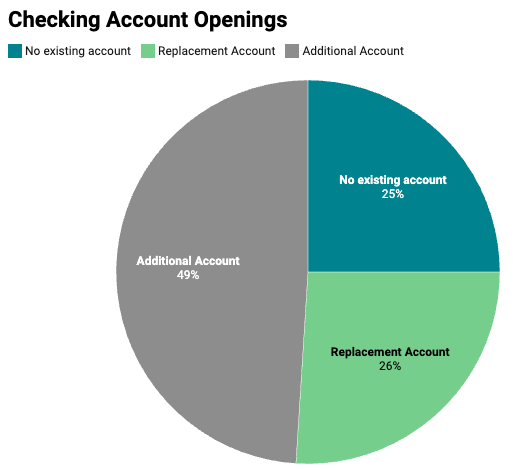

It’s still early, but the available evidence suggests that consumers, particularly mass market consumers, are open to new models. The JD Power data reveals that about half of consumers are opening up additional checking accounts, while a quarter of new checking accounts are opened by young adults opening their first accounts and the remaining quarter by consumers replacing an existing account with a new account:

What this tells me is that consumers are evaluating new deposit products, alongside their existing products, and deciding which should be their primary account. That decision will be influenced by a huge range of different factors — interest rate, rewards, utility, convenience, trust — which are, themselves, influenced by the business models of the companies offering the products.

It’s still early, but consumers appear to be telling the market that NIM doesn’t always produce their preferred products.