Imagine that you’re in a serious, long-term romantic relationship with someone. You love this person and are committed to spending the rest of your life with them. Then you discover an odd quirk about them — every two weeks they get up early in the morning, take a crisp $100 bill out of their wallet and stash it in the pocket of a random coat or pair of pants. They do this every two weeks, like clockwork. And every year, sometime in the spring, they take a couple of days off work and systematically search through their clothes to recover all the hidden money. Naturally, your first question after you discover this strange behavior is why? “Why are you doing this?” you say. “Seems like a bizarre and labor-intensive ritual.” And this person, your soulmate, says, “yeah, it’s a bit of a hassle, but I just love finding money in my clothes.”

Now, you’re probably not going to break up with this person. This isn’t a dealbreaker. In fact, you can tilt your head, squint your eyes, and almost see the logic in it. After all, it is fun to find money in your clothes. Still, it’s a ; a disquieting thing to learn about a person whose judgment and common sense you generally trust. You might, at some point in the future, gently suggest that they stop intentionally hiding their money in their clothes and instead take that cash and, I don’t know, pay off their credit card debt or save it in an emergency fund.

Last year, Americans overpaid their federal taxes by about $3,200 on average. That translates to a little more than $120 per pay period for a standard W-2 income. Essentially, they voluntarily took money out of their wallets, hid it from themselves by giving it to the U.S. government, and then spent hours or days filing a return to get the money back.

This is weird! This should concern the banks and fintech companies that are in committed, long-term financial relationships with these consumers. This should, perhaps, be something that those banks and fintech companies sit down and gently discuss with their customers and try to convince them to, you know, stop doing.

The Next Table Stakes Feature

I believe that tax planning and filing will be the next table stakes feature for banks and consumer-facing fintech companies. In the not-too-distant future, consumers will be able to dynamically manage their taxes throughout the year and quickly and easily file their taxes with the government, all from within their digital banking app.

Why do I think this?

A few reasons:

- Tax withholding is one of the most consistently bad financial decisions that most Americans make. As I mentioned above, the average amount that consumers overpaid the U.S. government this last tax year is on track to be more than $3,000. When you consider that the average U.S. consumer carries more than $5,000 in credit debt, it becomes evident that there might be better ways to use that money throughout the year than giving the government an interest-free loan. And I say this even though, yes, finding ‘free’ money every April is kinda fun.

- Taxes are one of the most significant line items on most consumers’ personal balance sheets. The average annual tax bill for a U.S. consumer is roughly $15,000. Given the relative weight of tax payments on consumers’ balance sheets, it’s really quite strange that banks have historically had no interest in helping them manage it.

- Tax filing is one of the most unnecessarily expensive, annoying, and time-consuming activities in the history of modern civilization. Americans spent roughly 6.5 billion hours this last year trying to file their taxes. They also spend something like $17 billion annually to help them do it, between tax preparation services and tax preparation software. A significant value provided by fintech and digital banking is reducing the time, and money consumers spend on unfun things. Seems like a match made in heaven!

- Tax planning and filing is becoming more complex. I’ll use two examples to illustrate this point. First, Americans are increasingly turning to freelance work to supplement or replace full-time employment, which, in the world of the IRS, means fewer W-2s and a lot more 1099s. Second, the number of people with crypto transactions nearly quadrupled from tax year 2019 to 2020, up 362%, and figuring out how to correctly file taxes for crypto gains is no joke.

- Tax planning and filing are unlikely to become less complex or burdensome anytime soon. Even though there are a ton of great ideas out there for how to simplify the system and make it easy and inexpensive to file your taxes (The IRS could, for example, pre-populate tax returns for more than 60 million Americans without having to change a damn thing), there is a shadowy and sinister force that has been spending a lot of money over the last two decades to keep things from changing. I’ll give you a hint — their name rhymes with BurboBax.

- Tax planning is a powerful tool for helping high-income earners build and protect wealth. I don’t love this from a societal perspective, but purely from a banking perspective, it’s obvious that tax planning is an essential financial lever for the high-income customers that all banks covet.

- Tax credits are a powerful and underutilized tool for putting more money in the pockets of low-income earners. The earned income tax credit (EITC), for example, is designed to mostly go to low-income people who don’t make enough even to owe income taxes. Ironically though, that creates a problem. Twenty-two percent of eligible taxpayers don’t claim the EITC in a typical year, and two-thirds of those not receiving the benefit don’t get it because they don’t file a tax return. Banks and fintech companies serving low-income customers should be focused on closing this gap.

- Tax planning sits at the intersection of many important financial and life decisions. Where you live. Where you work. How you invest. How you save for retirement and for sending your kids to college. How you plan for future medical expenses. All those decisions (and plenty more) revolve, to some degree, around your taxes. Banks (and, increasingly, fintech companies) love to be involved in those decisions!

- Filing taxes is a forcing function for financial data aggregation. Tax returns are, speaking from a data science perspective, a goldmine. Everything is in there! Income, direct deposit, significant expenses, mortgage, investments, retirement … and it’s not just at an individual level, it’s at a household level too! It is the single most comprehensive view of customers’ financial lives that a bank or fintech company could hope to get, and consumers are legally required to assemble it every year!

So, to sum up, tax planning and filing would, if it was embedded as a capability within banks’ and fintech companies’ apps, allow them to streamline one of the most obnoxious and complicated financial tasks that their customers do on a recurring basis, generate additional money for their customers to save, invest, or pay down debt with, give them an excuse to have mission-critical financial and life planning discussions with their customers, and provide them with a uniquely comprehensive view into their customers’ household balance sheets.

Sounds pretty good, but …

What Would It Take to Do This?

Let’s pretend that we work at the Bank For Brilliant Newsletter Writers and Readers, and we want to add tax management capabilities for our consumer customers into our app.

What are we going to need?

- Well, first, we’ll need a ‘tax engine.’ This is essentially just a big decision engine into which we input federal and state tax codes. The tax engine calculates tax returns for individual customers (using the data they supply) and automatically files the returns electronically with the IRS and relevant state agencies. Of course, the federal and state tax codes are big and complex, with lots of loopholes, and they’re constantly changing, so we’ll want to utilize machine learning to help us continually parse them and ensure the criteria within our decision engine is always up to date.

- We’re also going to need the ability to acquire and ingest lots of data automatically. We’re digitizing the experience of handing a box of tax forms and bank statements to a certified public accountant (CPA), which means we’ll probably want to lean on a combination of open banking data aggregation, payroll data APIs, and a little document scanning and OCR.

- Let’s not forget that we will need to be approved by the IRS and state filing agencies as an authorized electronic filing provider so that we can legally submit tax returns on behalf of our customers. We’ll also want to backstop our service with insurance in the unlikely event that our tax engine messes something up, and the IRS or a state tax authority hits our customers with an audit or penalties and interest due to our calculation error.

- And finally, we’re going to want to figure out where to plug humans into our process, recognizing that some tax planning situations (particularly for our high-income customers) might require a bit more nuance and emotional intelligence than our automated system can provide.

Who is Actually Going to Do This?

As I just described, building an intelligent, automated tax planning and filing service isn’t an easy task. There’s a reason why banks and neobanks haven’t added these capabilities to their apps yet.

So, why am I so optimistic that we will see these capabilities show up in banking apps in the not-too-distant future?

Well, because we already are.

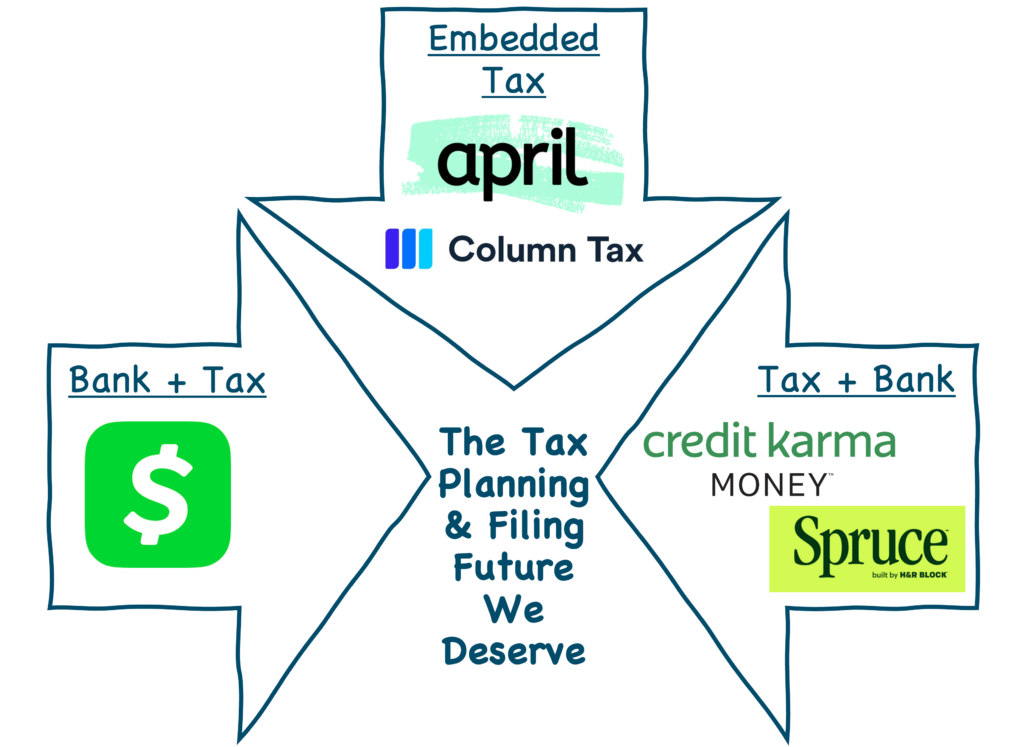

The future is here! Specifically, we are seeing massive progress towards this vision converging from three different directions:

- Banks adding tax planning and filing capabilities.

- Tax planning and filing platforms launching digital banks.

- Banks leveraging embeddable tax planning and filing services.

Bank + Tax

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

It didn’t surprise me that Cash App was the first neobank to do this. They tend to be early to a lot of the digital banking features that wind up being considered table stakes. And much like Cash App’s expansion into BNPL, the addition of tax filing happened via an acquisition. When Credit Karma was forced to sell its tax prep business (more on that in a second), Cash App snatched it up for $50 million and spent a couple of years integrating it into its core product. The result is a streamlined digital filing service that is entirely free and provides 5-day-early access to tax refunds if they are deposited into the Cash App.

Tax + Bank

Credit Karma was forced to sell its tax prep business to Cash App because it had agreed, nearly a year earlier, to be acquired by the market leader in tax prep software — Intuit — and the Justice Department wouldn’t sign off on the acquisition otherwise. At roughly the same time as this happened, Credit Karma also launched its own digital checking account product — Credit Karma Money — with all the standard neobank bells and whistles.

And with these two chess pieces moved into position, guess what Intuit did next?

Credit Karma … has launched a new tax experience with the goal of taking the stress, uncertainty and complexity out of taxes and helping members make the most of their refund. This includes seamless tax filing through TurboTax and faster access to refunds in-season through early deposit and refund advance programs, as well as deeper insights into their finances throughout the rest of the year. Through this integration, Credit Karma and TurboTax, from Intuit (NASDAQ: INTU), will offer most filers with simple tax returns the option to file their taxes with TurboTax directly within the Credit Karma app and gain faster access to their refund with Credit Karma Money.

Additionally, Credit Karma will launch a new feature to provide its members who previously filed their taxes with TurboTax with rich insights about their finances, income and taxes on an ongoing basis. Members will also be able to estimate their refund and review common tax terms to help them better understand their finances, navigate life events and plan for the future.

Interestingly, H&R Block (Intuit’s biggest competitor in the tax prep software market) has also jumped into the neobank space recently with the launch of Spruce. This digital deposit product offers, among many other features, the ability for customers to automatically allocate a percentage of their next tax refund directly into goal-based savings buckets:

Embedded Tax

Here’s a good rule of thumb for fintech these days — if a bank or fintech company is offering a product to customers directly, there will assuredly be a set of fintech infrastructure providers selling an embeddable service that can enable other banks and fintech companies to quickly add that product to their own stacks.

Tax planning and filing is no exception to this rule.

April and Column Tax are two such infrastructure providers. They both provide tax management APIs, which banks and consumer-facing fintech companies can consume to offer their customers services like streamlined tax filing and tax withholding adjustments.

The beauty of this embedded approach, in my view, is that it gives each bank and fintech company more flexibility to tailor the tax management offerings that will best meet the needs of their customers. Propel, a fintech company focused on low-income consumers, is working with April to embed tax management capabilities into its app and is an excellent example of what I’m talking about:

“Tax filing is stressful and complicated, especially for families with limited income. We’re excited to partner with April to offer these families a simple solution to access benefits such as the Child Tax Credit and the Earned Income Tax Credit, which are a lifeline for financially vulnerable households,” said Jimmy Chen, Founder and CEO of Propel

When Will We Get There?

Between Cash App’s acquisition of Credit Karma’s tax management business, Intuit and H&R Block getting into digital banking, and infrastructure providers like April and Column Tax, I think the pieces are in place to get tax planning and filing features into most consumers’ hands via digital banking apps … eventually.

When, precisely, we get there will depend on the answers to a couple of key questions:

- How big can Credit Karma Money and Spruce get? Both of these products are new, so it’s too early to say how successful they will be at acquiring and retaining a large number of customers. At first blush, I would say I’m a bit more bullish on Credit Karma, given their brand and marketing prowess.

- Will Cash App influence other neobanks’ product roadmaps? Usually, the answer to this question is a definite yes. However, as fintech funding gets tight and neobanks pivot to focus on profitability, I wonder if capabilities like lending might leapfrog tax management on those neobanks’ priority lists?

- Will regular banks and credit unions get in on the act? April and Column Tax selling their APIs to traditional banks and credit unions would significantly boost the adoption of embedded tax planning and filing in the industry. And I think banks and credit unions would see these features as compelling additions to their core products. However, selling software to banks and credit unions is tough sledding, and I’m not willing to bet that either company will get significant traction here in the next few years.

- What new products and experiences get built on top of these tax engines? What April and Column Tax have built represents a major unlock for the entire industry. We have a few early examples of what can be built on these platforms (streamlined filing, tax withholding adjustments, etc.), but there are undoubtedly many more use cases to be explored. More innovation built on top of tax engines = more reasons for banks and fintech companies to offer these services to their customers.

- Will revisions to the federal and state tax codes slow down or speed up innovation? This is the great unknown. There are many ways that states and the federal government could make tax management easier for consumers. Ironically, such changes could reduce the value of some of these embedded tax management features we’ve been discussing. Or the tax codes could continue on, slowly evolving in the uniquely complex and terrible ways that they have been for decades. Given the incentives involved, I’d bet on the latter.