3 Fintech News Stories

#1: Fintech + Construction

What happened?

A fintech company focused on the construction industry raised a seed round:

Adaptive, an 11-month-old startup that has set out to give construction teams better tools to manage their back offices, has raised $6.5 million in a seed round led by Andreessen Horowitz (a16z). This adds to the $750,000 the company raised in pre-seed funding last August.

Adaptive’s offering is targeted toward general contractors, but not giant ones — think more SMBs, many of which might not have the resources to hire accounting staff. It’s being built on the premise that current methods for GCs to stay on top of spending are “time consuming, error prone, and yield very limited visibility into project performance,” which can cause disputes between parties. There are many transactions conducted in any given project, and each requires multiple steps for approval and reconciliation.

And another such fintech-for-construction company, Built, introduced a new tool for lenders:

Built Technologies … announced Project Pro, the first-of-its-kind contractor management and project monitoring solution for lenders. Construction lenders around the world are limited in their ability to monitor and manage the risks of their construction portfolio. They often lack specialized tools built for construction financing that provide actionable insights, and in many cases this situation prevents them from keeping money moving smoothly throughout the ecosystem of stakeholders. Built’s Project Pro, available today, changes this paradigm for lenders from reactive to proactive.

So what?

The construction industry is quickly becoming a case study for the value of verticalized fintech.

We have Built, which has solutions for both construction companies and the lenders that serve them. We have Siteline, which is designed to streamline billing and payment processes for construction companies. We have Briq, which is built for CFOs and finance teams at large construction companies. And now we have Adaptive, which is focused on leveraging AI and automation to simplify bookkeeping and back-office work for smaller construction companies.

In all four cases, the secret ingredient is the domain expertise that is built into the software. This expertise is hard-won — the team that founded Adaptive, for example, spent months running a white-glove accounting service for construction companies in order to learn the ins and outs of how those companies handle their finances — which makes the resulting solutions all the more differentiated.

#2: What Problem is this Solving?

What happened?

Apple apparently wants us to pay for our gas before getting out of the car:

Apple Inc wants you to start buying gas directly from your car dashboard as early as this fall, when the newest version of its CarPlay software rolls out, accelerating the company’s push to turn your vehicle into a store for goods and services.

A new feature quietly unveiled at Apple’s developer conference this month will allow CarPlay users to tap an app to navigate to a pump and buy gas straight from a screen in the car, skipping the usual process of inserting or tapping a credit card.

So what?

To quote Josh Baskin, I don’t get it.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Electronic toll collection, as a replacement for toll booths, makes sense. It’s safer and faster for everyone. Locating and paying for parking directly from your dashboard is similarly convenient. Love it.

I don’t get this one. Until my car can also pump its own gas (or, I suppose, if I lived in New Jersey or Oregon), this isn’t gonna save me much time or effort. It’s not going to keep me from freezing to death when I’m filling up my tank in January.

Payments is a funny space. Product managers just can’t seem to help themselves from integrating the latest cool ideas, regardless of how useful they are.

#3: Building Momentum for Black Homeownership

What happened?

Ready Life, a fintech company focused on closing the racial homeownership gap, will be launching in September:

A new digital banking and payment processing platform, Ready Life, led by two Black entrepreneurs, is taking aim at the racial wealth gap by starting a mortgage fintech. Ashley D. Bell and Bernice A. King, respectively the CEO and advisory council chair of Ready Life, are behind the fintech and hope to turn 100,000 renters into homeowners.

Customers who open an account with Ready Life will get a checking account and associated debit card that they will use to make payments — primarily rent and other housing expenses, but not limited to those.

Additionally, underwriting technology launched in September by Fannie Mae will also provide technical support for turning Ready Life customers’ rental payments into mortgage underwriting fodder.

So what?

I wrote last month about Fannie Mae’s multi-part plan to close the racial homeownership gap. A big part of that plan is incorporating on-time rental payment history (a strong willingness to pay signal) into the mortgage underwriting process.

Part of that effort is technical — enabling Desktop Underwriter (the system that lenders use to establish a home loan’s eligibility to GSE standards) to incorporate and use rental payment data.

The other (likely bigger) part of Fannie Mae’s effort is building awareness and demand — they need to make consumers aware that rental payment data can be used to underwrite a conforming mortgage and put pressure on the credit bureaus to collect that data and on lenders to use it.

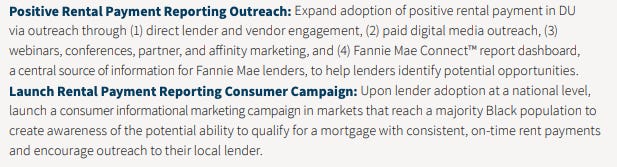

Fannie Mae has a plan to do this outreach:

However, there is only so much they can do by themselves, which is where Ready Life comes in.

The product that Ready Life has put together feels, to me, a little overbuilt (why do you need a dedicated checking account to collect rental payment data?), but that’s not really the point. The point is to build momentum for Black American homeownership by aggregating as much consumer demand for Fannie Mae’s rental payment solution as possible. That’s what Ready Life appears to be doing:

Ready Life and Bell are taking a marketing-forward approach to attract the customers they are looking to help — mainly Black Americans and other people of color who feel cheated by the current lending system that prioritizes good credit when considering mortgage eligibility.

To help reach their target demographic, Ready Life will sponsor this year’s Denny’s Orange Blossom Classic, a four-day celebration of historically Black Colleges and universities culminating in a nationally televised football game between Florida A&M and Jackson State on Sept. 4: one day before its scheduled launch.

2 Fintech Content Recommendations

#1: As Regulatory Scrutiny of BaaS Grows, Rumors Swirl (by Jason Mikula, Fintech Business Weekly)

A few weeks ago, I asked in this newsletter — What’s going on right now with bank-fintech partnerships?

I’d been hearing some rumors that banks (and BaaS Platforms) were having trouble onboarding new fintech clients due to increased regulatory scrutiny.

Jason apparently heard these rumors too and did a great job reporting on them. His piece outlines the concerns that regulators have been publicly expressing about BaaS and rent-a-charter arrangements and some of the consequences of those concerns that are currently playing out behind the scenes.

#2: Why the Time is Right for More Immigration-focused Fintech (by Misha Esipov, Nova Credit)

Misha makes a very strong case for both the economic benefits of immigration and the importance of fintech in unlocking those economic benefits. This article is focused on the UK, but I think the broad strokes are applicable everywhere.

One thought that struck me while reading this piece — it seems like we’re seeing a definite uptick in B2C fintech solutions focused on immigrants (neobanks, lenders, etc.), but I don’t know that we’ve seen a corresponding increase in the number of immigration-focused fintech infrastructure companies. What else needs to be built to fully unlock this opportunity?

1 Question to Ponder

#1: Who are the sharpest, most interesting fintech generalists you know?

I’m putting together an event and would be curious to get your nominations. Major bonus points if you say someone other than you 🙂

If you have someone to recommend, please DM me on Twitter or LinkedIn.