Take a look at this chart from CB Insights of all of the private companies in the world worth $1 billion or more and tell me what stands out.

It’s a lot of fintech.

I mean, I knew fintech was popular, but wow. And those are just the unicorns! That graphic doesn’t include public fintech companies (Affirm, Sofi, etc.) nor the thousands of private fintech companies that aren’t (yet) worth a billion dollars.

It makes me wonder — what do all of these fintech companies do?

There’s a bottoms-up way of answering that question, but quite frankly, we don’t have the time or column inches to do that in this essay.

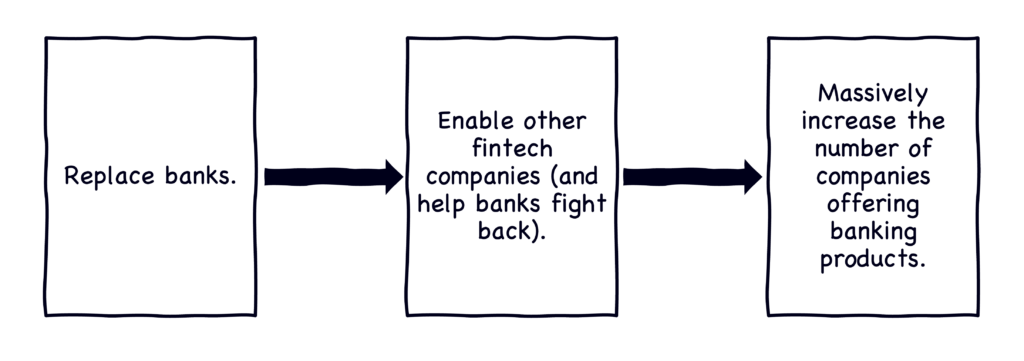

Instead, let me run a theory for how to understand the fintech ecosystem by you. A theory, to paraphrase Lester Bangs, for you to disregard completely — fintech has, up to this point, been focused on three objectives, and almost all fintech companies can be categorized based on which of these objectives they are optimizing for:

- Replace banks. This one is straightforward. Pick a job to be done that a bank currently does and do it better.

- Enable other fintech companies (and help banks fight back). Pick your metaphor — selling picks and shovels, arming the rebels, whatever. If you are in this category, then you are in the business of selling enabling infrastructure.

- Massively increase the number of companies offering banking products. There are infrastructure companies in this category as well, but their focus is on expanding the market by enabling non-finance companies to embed financial products.

(Editor’s note: before anyone freaks out too much, the companies listed in this graphic were just the ones I quickly pulled out of the CB Insights’ graphic to illustrate the broader point.)

As the relative distribution of companies in the graphic above suggests, we’ve been trying to replace banks for a while now (with a decent amount of success, FWIW). The ‘enabling infrastructure’ category is slightly less mature, and the ’embedded finance’ category is still quite new (though fast-growing).

From this perspective, these categories are perhaps better understood sequentially:

What’s interesting about this ‘timeline view’ of the fintech ecosystem is what it suggests about our ultimate destination.

According to some of the most respected voices in our industry, the endgame for fintech is embedded finance.

Here’s Angela Strange:

In the not-too-distant future, I believe nearly every company will derive a significant portion of its revenue from financial services.

Every company, even those that have nothing to do with financial services, will have the opportunity to benefit from fintech for the first time.

the really exciting part comes to us as consumers. With new financial services companies spinning up—and some of our favorite brands launching financial services—our existing services are getting better.

And here’s Matt Harris (the Bain one):

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

If the analysts are right, and 40 percent of the payments industry will move to an embedded model, and if we stipulate that lending and insurance will reach, say, 20 percent each, then this fourth platform shift — whereby fintech underpins all software companies — will be the big one.

At a five times revenue multiple this transformation will create $3.6 trillion of value. I’ll happily acknowledge that the internet is a big deal, sure. Cloud, mobile, great. But to put things in perspective, those three platforms together produced just under $3 trillion of value for founders, venture capitalists and everyone involved in the startup ecosystem. But we think, and the data clearly suggests that the opportunity in front of us now is even larger.

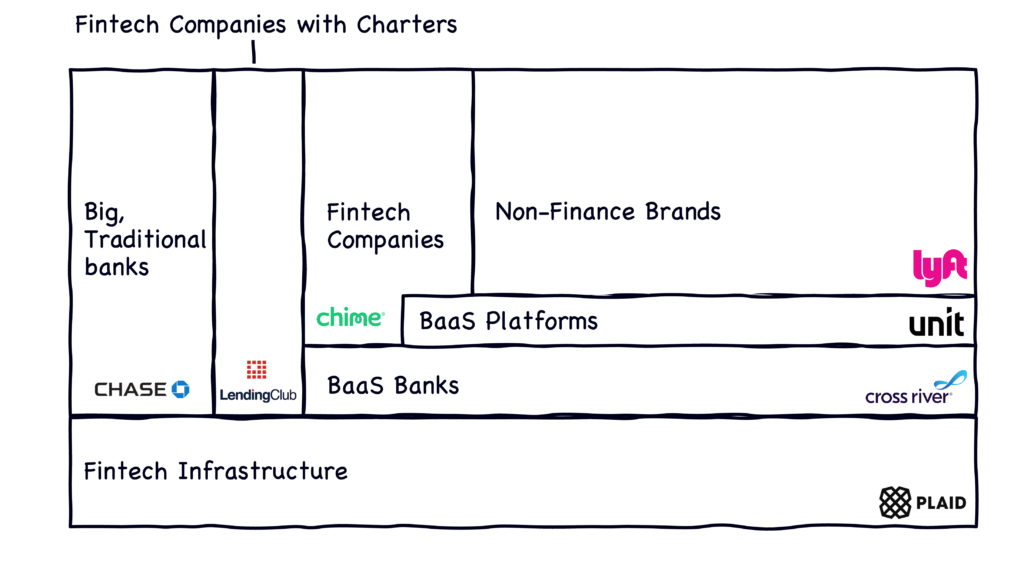

If we accept this line of thinking — that fintech will eventually lead to nearly every company embedding financial services products into their core offerings — and fast forward a decade or two, the financial industry might look something like this:

A new generation of fintech infrastructure companies provides enabling technology for the industry. A few large banks survive and continue to serve customers directly. They are joined by a smaller number of fintech companies that acquire bank charters. Most community and mid-size banks are either acquired or pivot primarily to a banking-as-a-Service (BaaS) model. A few of the banks that choose BaaS work directly with fintech partners, but most end up working through BaaS platforms. Those platforms enable a decent chunk of customer-facing fintech companies, but, more importantly, they onboard a vast and diverse set of non-finance brands, all of which embed value-add financial products into their core offerings.

This is a compelling and easy-to-grok vision of the future. If nearly every company embeds financial products into their offerings, you’re suddenly looking at a MASSIVE TAM (Mr. Harris’s $3.6 trillion estimate might be conservative). And if the embedded financial products are skeuomorphicly similar to the ones that customers are already using, then the transition to a mostly-embedded financial future will feel comfortably familiar.

It all sounds great … in theory. However, there are two critical questions we need to answer:

- Are customers interested in embedded finance products?

- Would we, as an industry, be delivering the maximum amount of customer value by going all in on an embedded finance future?

Let’s take these one at a time.

Are Customers Interested in Embedded Finance?

It’s a little weird how, despite all the hype around embedded finance, no one has done any quantitative research to try and confirm if customers would actually be interested in getting financial products from the non-finance brands they interact with. That seems like a vital assumption to validate!

Well, Ron Shevlin and Cornerstone Advisors just validated it.

In a recently-released research report, Cornerstone found a strong level of interest from U.S. consumers in acquiring financial products from the non-finance brands that they like and frequently interact with:

Three-quarters of gamers are interested in an in-game account where they could deposit money and use it to buy and sell virtual in-game items and collect rewards for game achievements/progress.

Two-thirds of home fitness fans expressed interest in getting health insurance from home fitness providers with rates based on their personal fitness habits.

Nearly two-thirds of fashion aficionados would consider getting an investment account from a luxury brand that allowed them to easily invest in that company’s stock.

Six in 10 car buffs would investigate auto insurance—with rates based on their personal driving history and behavior—directly from a car manufacturer.

Half of home improvement do-it-yourselfers are interested in a savings account that automatically sets aside money to save for large home improvement projects from Home Depot or Lowe’s.

Remember, this survey asked consumers what they would do, hypothetically, if a brand they like and interact with offered them a specific financial product. These are projections of what might happen, not findings on what has happened.

That said, this data strongly suggests that consumers will acquire embedded financial products in large numbers if/when non-finance brands offer them.

Should We Go All In on Embedded Finance?

OK, the answer to the first question was yes. Customers appear interested in embedded finance.

Now, the second question — is this the future that we should be putting all our chips down on?

No.

Let me explain why.

Embedding traditional financial products into non-finance companies’ websites, mobile apps, and business processes makes perfect sense. It’s a smart distribution strategy, and, as early test cases like indirect auto lending and BNPL have demonstrated, customers have an appetite for it.

It’s not that embedded finance is bad; it just misses the point.

Embedded finance is about distribution, but our most important challenge in financial services is manufacturing.

Bank Products are the Problem

Last year, I wrote in my newsletter:

When we measure the rate of unbanked and underbanked consumers, we do so under the implicit assumption that the goal is to get consumers to become fully banked. As if owning every product a bank offers today is synonymous with having all of your financial needs met.

Customer satisfaction surveys suffer from a similar flaw. When we ask consumers if they are satisfied with their current bank we are, in practice, asking them to make a comparative judgment — compared to what you would expect from an average bank, how satisfied are you with your bank?

We’re missing something important.

We should be trying to understand, holistically, how well customers feel they’re doing financially and what they think they need in order to improve. We should be asking questions like are you achieving the financial future that you want? And is your bank helping you achieve that financial future?

I wrote that in reaction to a finding from a survey that I was fascinated with at the time, and that continues to shape my thinking today. The survey asked:

What is crucial to the future of your financial success?

And, in the responses to that question, only 1% of U.S. consumers mentioned a bank.

1%.

The other 99% of the answers covered a vast range of financial needs that are largely unaddressed by traditional financial products.

So, when I say that financial services has a manufacturing problem, this is what I’m talking about. The traditional financial products we’ve gotten so good at efficiently manufacturing only address a small percentage of customers’ holistic financial challenges. Given this, it’s a mistake to assume that embedding traditional financial products in as many places as possible will somehow fix everything for our customers.

It won’t. This isn’t a distribution problem.

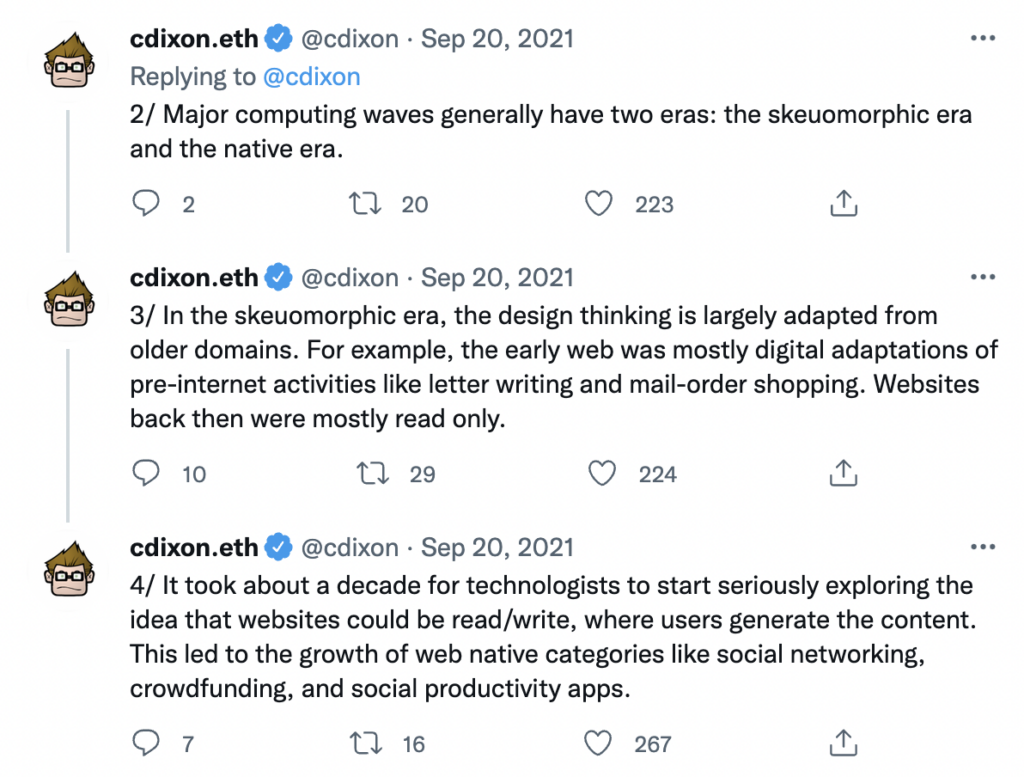

Folks in the crypto/web3 space are fond of pointing out that skeuomorphic thinking in product development can often lead us to miss opportunities to build something fundamentally new:

This is a crucial point.

The most important opportunity in fintech isn’t adapting traditional banking products to new distribution channels. It’s reprogramming banking to help power entirely new product concepts that solve money-adjacent problems that traditional banking products have never gotten close to solving.

Reprogrammed Banking > Embedded Banking

The concept of ‘reprogrammed banking’ is simple.

Fintech has atomized banking. We have the building blocks — the primitives, to borrow a term from CS — to create any type of financial product we want. More importantly, we can combine financial services primitives with non-financial services primitives to build SaaS products that can address customer problems that are money-related but not money-exclusive.

This is a realm in which banks and fintech companies have mostly not yet tread.

However, there are a few examples where we are starting to see some traction.

B2B: Back-office Problems

Small businesses share a common challenge: efficiently managing back-office processes like scheduling, billing, payments, collections, and accounting. Most small businesses are started by people who have a passion for their profession but who don’t necessarily excel in these operational areas. Consequently, they are interested in software that can alleviate their operational headaches.

The trouble is that every industry is different. The back-office challenges faced by a small medical clinic are only superficially similar to the back-office challenges faced by a general contractor. Under the surface, the workflows and datasets are significantly different.

What’s needed are back-office software solutions — for functions like accounting and billing and customer service — that are tailored to the precise needs of the industries that they are serving. These SaaS products need to have financial services components (payments, for example), but, crucially, they are not bank products.

In the case of healthcare and construction specifically, a number of companies are building these types of tailored back-office solutions, including Rivet (healthcare billing and payments) and Siteline (construction billing and payments).

B2C: Relationship Problems

Money plays a foundationally important role in many different types of relationships. It causes couples to fight. It stresses out parents who don’t feel that they’re adequately preparing their children to go out into the world. And it creates a lot of awkward silences between adults and their elderly parents.

What’s weird is that there aren’t any traditional bank products specifically designed to solve these money-adjacent relationship challenges.

A joint checking account will allow both people in a couple to deposit and spend their money, but it won’t help them have productive conversations about their shared financial goals and priorities.

Parents can open a custodial or joint checking account with their teenage child, but that account won’t give them any guidance on how to talk to their teen about money or teach them the financial literacy skills they’ll need later in life.

Fortunately, companies like Zeta (couples banking) and Copper (teen banking) appear to be taking a relationship-centric approach to product design, which is a welcome change and one I hope other founders push the boundaries on even further.

How Do We Encourage More Reprogrammed Banking?

There are two imperatives:

1.) Continue to build more granular fintech infrastructure. The more flexibility and granular control we give to SaaS product developers, the easier it will be for them to build these money-adjacent SaaS products.

I feel great about our progress on this front. The march of fintech infrastructure is relentless. Take debit card issuing as an example. We’ve taken a quantum leap from partner bank-based issuing and program management (inflexible and labor-intensive) to Lithic and Highnote (granular and fully programmatic).

2.) Recruit and support founders with non-fintech backgrounds. In the early days of fintech (PerkStreet, Moven, Simple), having at least some knowledge of financial services was, I would imagine, an important asset. There were no established examples or models that you could follow back then. Everything had to be built from scratch, and having a baseline knowledge of how banking worked was likely a handy tool in the toolkit.

Today, we have the opposite problem. We don’t lack founder-friendly infrastructure and resources. What we are missing is an outsider’s perspective, a view into how to solve the money-adjacent problems that consumers and businesses quietly wrestle with beyond the purview of established banks and fintech companies.

This is the downside to the phenomenal success that fintech has had over the last 15 years, the success that minted so many of those unicorns on CB Insights’ list. We now have an abundant supply of experienced fintech founders and operators from which to source new founders. That’s not a bad thing in and of itself, but it can become problematic if that fintech talent pipeline (which early-stage investors understandably like to bet on) crowds out new, less experienced founders.

There’s a great quote from one of my favorite fantasy authors, Patrick Rothfuss, in which the main character, Kvothe (a highly accomplished musician), explains what makes his friend Denna (an amateur musician) so compelling:

Think of music as being a great snarl of a city […]. In the years I spent living there, I came to know its streets. Not just the main streets. Not just the alleys. I knew shortcuts and rooftops and parts of the sewers. Because of this, I could move through the city like a rabbit in a bramble. I was quick and cunning and clever.

Denna, on the other hand, had never been trained. She knew nothing of shortcuts. You’d think she’d be forced to wander the city, lost and helpless, trapped in a twisting maze of mortared stone. But instead, she simply walked through the walls. She didn’t know any better. Nobody had ever told her she couldn’t. Because of this, she moved through the city like some faerie creature. She walked roads no one else could see, and it made her music wild and strange and free.

We need more founders working in and around fintech who don’t know any better.