If you gave a bank executive a blank canvas and asked them to paint you something, they might come up with something like this:

If you showed the first painting to an executive at a second bank and asked that executive to come up with something better, they’d likely come back with something this:

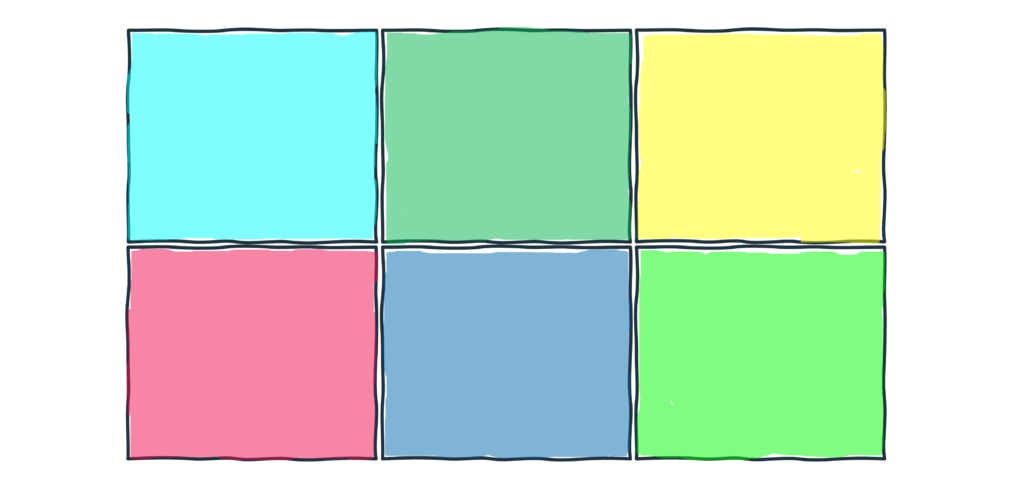

And on and on and on, until you end up with a collage of slightly differently colored squares:

This has been the competitive dynamic within banking, when it comes to product innovation – tiny variations on a theme.

It makes sense. Manufacturing bank products has, for most of banking history, been expensive and time consuming. It was much easier to build and sustain a competitive advantage through differentiated distribution (having the most branches in a particular region) and a metric ton of marketing. Product innovation was largely an afterthought.

Then came fintech.

And suddenly manufacturing bank products became much cheaper and faster (thanks fintech infrastructure!) and branch-based distribution advantages were rendered moot and we had a whole bunch of fintech founders with no background in banking being asked to paint a better painting than what the banks had come up with and, well …

Now, for the most part, this is good! Fintech is painting way outside the lines and consumers are benefiting from the resulting innovations.

As I wrote about a while back, fintech is making some long-overdue upgrades to deposit products. And sure, hands-on-the-wheel money is a bit of a disconcerting concept at first blush, but there are some interesting product ideas coming out of it.

I am generally a fan of the wild experimentation and product cross-pollination that fintech has brought to banking.

However, there are a couple of product categories where I hope fintech exercises some caution.

One in particular.

Credit Cards

Credit cards are already really weird products.

We’ve gotten used to them, so it can be a bit hard to see anymore, but if you ever try to explain how a credit card works to a 14-year-old, you’ll quickly remember just how complicated and strange they are.

It’s a way to pay for things that’s a loan, but it doesn’t have to be a loan if you pay it back on time but it can be a loan if you need money in an emergency. It doesn’t cost you anything, except if you don’t pay it back right away, but if you do then it’s free, except if it has an annual fee, but most don’t, but a few do and they might be worth paying for because of the rewards. Rewards are great. You have points and miles and cashback and rotating categories and some rewards expire and some don’t, but make sure that you don’t just spend money to get the rewards because that’s how they get you. They are accepted pretty much everywhere because stores love them, but you might see some stores refusing to take certain types or asking you to spend a certain amount in order to use them because stores actually hate them. And oh yeah, they’re a great way to establish and build your credit score, but you probably won’t be able to get one because you don’t have a credit score yet.

And they’re weird and challenging for banks too!

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

The big issuers are accustomed to them, but there’s a reason that most community banks either don’t offer credit cards or offer them through white label partnerships with larger issuers. They are complex.

They are challenging to underwrite from a risk perspective because there is no collateral and customer risk profiles are constantly shifting and it’s highly profitable to have customers revolving a balance … right up until it isn’t. They present a massive fraud management challenge because customers carry their cards everywhere and use their cards everywhere and issuers own almost all of the liability for fraud losses. And they require issuers to be outstanding at marketing (because it’s a ruthlessly competitive product category), collections (determining collections treatment strategy is tough when customers are constantly rolling in and out of delinquency), and compliance (credit cards are subject to tons of different regulations).

This is why the idea of more fintech companies jumping into credit cards makes me a bit nervous. The natural inclination of fintech founders to paint outside the lines combined with the already-complex nature of credit cards seems like a potentially dicey mix.

And yet …

Fintech is Diving Into Credit Cards

There are a whole bunch of converging factors that are driving fintech companies to enter the credit card business.

Let’s quickly talk through a few of them:

Fintech companies are trying to pivot to profitability.

Mary Ann Azevedo at TechCrunch recently surveyed a handful of fintech VCs about the shifting investment landscape and what they are looking for. Here are a few quotes from her interviews. See if you can pick out a theme:

- “Last year, investors were routinely investing in early-stage companies at roughly 50x to 100x ARR multiples and growth-stage companies at 30x to 50x ARR multiples. Given very low interest rates, investors were seeking yield anywhere they could find it and paying a premium for growth.”

- “Investors are increasingly differentiating between tech-enabled financial services companies and true software/technology businesses — with their respective business models and margin profiles — and valuing them as such (i.e., a neobank or tech-enabled vertical insurance carrier, which previously were valued at software multiples, are now getting valued similarly to their more true bank or insurance public comps).”

- “Many fintech companies will shift to maintaining fundamentally sound business models rather than chasing growth, and that is a positive development because it makes these companies more sustainable in the long term.”

- “the best consumer fintechs are taking this opportunity to optimize their models so they are positioned for profitable growth.”

Translation – the market is not rewarding unprofitable growth anymore, nor is it defaulting to always valuing fintech companies like software companies rather than banks.

Positive unit economics and profitability are, once again, sexy.

The credit card market is booming.

With inflation increasing, consumers are absolutely piling into credit cards right now. According to recent research from the New York Fed:

US household debt surpassed $16 trillion for the first time ever during the second quarter, the New York Federal Reserve said Tuesday.

Even as borrowing costs surge, the NY Fed said credit card balances increased by $46 billion last quarter.

Over the past year, credit card debt has jumped by $100 billion, or 13%, the biggest percentage increase in more than 20 years.

Americans opened 233 million new credit card accounts during the second quarter, the most since 2008, the NY Fed report found.

While this increased debt – along with the fact that the personal savings rate fell in June to 5.1%, the lowest since August 2009 – is certainly cause for concern, the New York Fed reports that consumers’ overall balance sheets are still in fairly good shape:

By and large, Americans continued to pay down debt on schedule last quarter, a reflection of the very strong job market. The NY Fed said the share of current debt transitioning into delinquency remains “historically very low,” though it did increase modestly.

This might explain why credit card issuers don’t appear worried:

Bank executives say low unemployment and credit-card delinquencies that remain below prepandemic levels give them confidence in consumers’ ability to keep up with their debts. And inflation isn’t such a bad thing for card companies, some executives say, since it can result in higher spending that translates into more fee revenue.

A slowing economy would usually prompt banks to pull back on lending. The opposite is happening with credit-card debt—an unsecured form of borrowing that is hard to recover when a borrower stops paying. Banks, it seems, aren’t convinced a downturn would significantly damage Americans’ finances.

In fact, they’re doubling down:

Card issuers are pouring more money into marketing expenses such as credit-card mailers, advertising and extra rewards, betting that it will translate into new business.

Capital One’s marketing costs increased 62% in the second quarter from a year prior to a quarterly record of $1 billion, mostly due to its U.S. credit cards. Discover’s marketing expenses increased 45%, the company said, also largely due to efforts to increase credit-card sign-ups.

Who knows if this optimism will prove to be wise. All we can say for sure right now is that the companies in the best position to understand the risks and opportunities of investing in the credit card business are investing heavily.

Gen Z is aging into credit cards.

There’s this persistent myth in financial services that young consumers don’t like credit cards. Neobanks have been the most recent standard bearers for this myth, first with Millennials and now with Gen Z.

It’s not true.

Gen Z, like Millennials before them, is adopting credit cards in increasingly large numbers:

During the height of the pandemic in mid-2020, card issuers pulled back and tightened new card volume. Since then, credit card originations have nearly doubled – increasing from 8.6 million in Q2 2020 to a record 19.3 million in Q2 2021. The return in consumer demand was most pronounced for Gen Z as the share of originations increased to 14.2%, a jump from 13.3% last year and 9.5% just two years prior.

On top of the record level of credit card originations is a return to consumer spending, particularly among the younger generations. In Q3 2021 Gen Z average balance per consumer increased 13.9% YoY – the only generation with two consecutive quarters of growth.

The reality of credit card adoption – and we have decades of data to demonstrate this – is that young consumers don’t like credit cards until, suddenly, they do. Older Gen Z consumers are reaching this point.

Credit invisible consumers are a particularly compelling target.

There are a lot of credit invisible consumers in the U.S., along with other consumers that can’t get access to credit at mainstream prices:

28 million American adults are credit invisible and another 21 million are unscorable. Of those with scores, 57 million are categorized as subprime, which typically indicates they could borrow only at significantly elevated interest rates. Hence, 106 million Americans, or 42 percent of the adult population can’t get credit at mainstream interest rates. Of course, many of these individuals genuinely pose greater credit risk. But among those 106 million are many millions who could qualify for credit at mainstream rates if additional data were brought to bear.

Fintech companies love to serve this customer segment. It’s less competitive (banks tend to focus on prime and super-prime borrowers). It’s aligned with their missions (democratize access to financial services!) And it starts them off on the right side of most discussions with regulators and consumer advocates.

No wonder we’re seeing an uptick in credit cards for credit invisible consumers (which we’ll get into more in a sec).

The infrastructure is finally (somewhat) ready.

If fintech companies want to launch a credit card, they now have infrastructure that can help them do so quickly and cost-effectively.

If you are looking for a one-stop shop, you have your credit card-as-a-service (CCaaS) providers – Deserve, Cardless, Zeta, Imprint, Concerto – which provide full-service issuance and management platforms. Think of these as the more modern versions of Synchrony and ADS, specializing in enabling non-finance brands to launch credit cards.

If you are comfortable with a little assembly required, then you can construct a credit card using a combination of partner banks (Cross River Bank, Column, etc.), card issuing platforms (Lithic, Highnote, etc.), Banking-as-a-Service platforms (Bond, Stripe, etc.), Lending-as-a-Service platforms (OnBo), and debt facility providers.

What Fintech is Doing with Credit Cards

We’ve covered why fintech companies might want to launch credit cards and how they can do so in an expedited way.

Now let’s see what fintech companies are actually building in the credit card space and assess just how far outside the lines they are painting.

The Credit Builder Card

Examples: Chime Credit Builder Card, Varo Believe Secured Card, Tomo Card

What is it?

A credit card for credit invisible consumers and consumers with poor or insufficient credit.

They’re basically the modern version of a secured credit card, except that instead of requiring an upfront deposit, these products find other, more customer-friendly ways to offset the risk to the issuer. Tomo has a 7-day payment cycle with automated repayment. Chime and Varo allow customers to put money aside from their checking accounts into separate secured accounts, which sets their cards’ limits and makes repayment easy.

The result is that these cards are low risk, low cost, and generally effective as credit-building tools. However, like traditional secured cards, these credit builder cards don’t offer much in terms of rewards.

Why I’m Intrigued

In practice, these cards virtually eliminate the possibility of missed payments, which makes them an unusually safe on-ramp for consumers into the U.S. credit system.

Why I’m Concerned

The downside to these cards’ safe design is that the use of these cards doesn’t generate repayment data that is all that useful for lenders. They make customers’ credit scores go up because on-time payments are being reported to the bureaus, but the data itself isn’t that indicative of the customers’ willingness to repay debt because the customer, practically speaking, isn’t being given much of a choice. The long-term effect of this data filtering into the credit bureaus is something that everyone who lends money for a living should be concerned about.

The Credit Card for Credit Invisible Consumers

Examples: Petal Card

What is it?

Pretty simple – a credit card for credit invisible consumers.

It differs from credit builder cards in that it doesn’t have a built-in mechanism to guarantee repayment. Petal – which actually offers two different but structurally similar cards – underwrites applicants based on their credit scores (if they have them) or their cashflow history (if they don’t have a credit score sufficient to be approved). Petal takes more credit risk, but also offers rewards that are more competitive than those you typically see for secured or entry-level credit cards.

Why I’m Intrigued

This is one of the few credit cards I’ve seen that strikes a good balance between giving credit invisible consumers a fair and accessible on-ramp into the credit system while not making it so safe that it would impact the usefulness of the repayment data Petal is reporting to the credit bureaus.

Why I’m Concerned

This seems like a challenging product type to build a business around. It’s riskier than the credit builder cards and it requires net-new customer acquisition to build a portfolio (rather than cross-selling off an established customer portfolio like Chime and Varo do). And given how much competition there is in the credit card business, that acquisition can’t be cheap. Petal is clearly gaining traction, but I wonder if that’s more of a testament to its specific execution prowess than it is to the obvious business appeal of this product type.

The AmEx Card for Rich, Credit Invisible Gen Zers

Examples: X1 Card, Point Titan

What is it?

American Express reborn, apparently.

X1 is, according to its marketing copy, the “smartest credit card ever made”. These smarts include features like auto-expiring virtual cards for subscriptions and instant notifications on refunds (my Capital One credit card does both of these things too, FWIW). Applicants are underwritten using their cashflow rather than their credit scores. The card earns customers 2X points on every dollar spent or 3X points on all dollars spent in a year if the customer spends more than $15,000. It doesn’t have an annual fee and its interest rate varies between 15% and 22%.

Point got its start offering a debit card with credit card-like rewards. It has since decided to sunset that product and pivot to offering a charge card (basically a credit card without the ability to revolve a balance) with premium rewards. The charge card will come with significant rewards (points based on categories starting at 5X for every dollar spent), perks (TSA Precheck and Global Entry, etc.), and similar smart features to what X1 offers. It has a whopping $399 annual fee and requires customers to have an income of at least $100,000 or at least $10,000 in liquid assets.

Why I’m Intrigued

Both companies have clearly sniffed out the ‘Gen Z likes credit cards now’ trend, which speaks well of them. And I love that Point is brining charge cards back! I actually have no idea why charge cards have fallen out of style, but a credit card that you can’t revolve a balance on? Sounds great!

Why I’m Concerned

Success for both products would seem to hinge on the companies’ ability to efficiently acquire customers. Indeed, X1 suggested in a recent interview that the reason it can afford to offer its product without an annual fee is that it relies on WOM rather than spending money on marketing. I doubt that will continue to be the case. Prime and super prime consumers are the most sought after customer segment in the credit card business. The big issuers spend a ton of money to acquire and retain them. And those customers tend to be a mercenary bunch. They will hop from one issuer to another if they see an opportunity to rack up more points/status/perks.

The Split Repayment for a Monthly Fee Card

Examples: Klarna Card, Possible Card

What is it?

It’s a no-interest credit card that allows customers to split up their repayments into smaller installments in exchange for a small monthly fee.

Let’s use the Klarna Card as an example. You make a purchase with the card, of any amount, and it automatically gets split out into 4 payments. You do this over and over again until you have a whole bunch of payments all due at different times (like when you use Klarna’s pay-in-4 BNPL product!) But then, the magic – the card automatically rolls up all those payments and consolidates them into one bi-weekly payment, which you can make via a linked debit card. The card has a $3.99 monthly fee (waived for the first year) and merchant rewards, which you get for completing unspecified “missions”.

The Possible Card, which has been announced but not yet released, is similar – a no-interest credit card that gives customers the option to split payments out into 3 or 4 installments in exchange for a monthly fee. The Possible Card appears to be built for a higher-risk, lower-income demographic (lower credit limit and no rewards), but it’s functionally similar to the Klarna Card.

Why I’m Intrigued

Well, the no interest part is pretty cool I guess.

Why I’m Concerned

I honestly don’t get this product category, especially the Klarna Card. What’s the virtue of splitting every payment into 4 installments only to rebundle those installments back into 2-week repayment cycles? Isn’t that just a credit card with a shorter repayment cycle and a $50 annual fee and substandard rewards? I mean, yeah, I know that they aren’t charging any interest, but couldn’t I get that same utility by combining my existing credit card with good old fashioned BNPL, when I need it? Or, alternatively, I could use a BNPL debit card …

The Debit Card With a Little Bit of Credit Card

Examples: Affirm Debit+ Card, Upgrade OneCard

What is it?

A decoupled debit card with the ability to finance specific purchases.

By default, transactions made on these cards are debit transactions (which are repaid the day after the transaction via an ACH transfer from a linked deposit account), but customers have the option to designate specific transactions to be “pay later”, which are then broken out into a number of installments.

The Affirm Debit+ Card allows customers to split almost any transaction between $100 and $1,000 out into 4 installments at 0% interest. The card, which isn’t widely available yet, will require customers to have a positive repayment history with Affirm and doesn’t charge any fees.

The Upgrade OneCard is similar, but it charges interest (8.99%-29.99%) on purchases that customers designate as “pay later” (presumably it allows any purchase to be designated as “pay later”). The Upgrade card also provides cashback rewards if customers link the card to Upgrade’s Rewards Checking account.

Why I’m Intrigued

I like the convenience of building optional financing directly into a debit card. The ability to stretch out bigger purchases while being able to avoid the temptation of credit cards (a real problem for many consumers!) is powerful, especially when the financing has a 0% interest rate.

Why I’m Concerned

Decoupled debit cards can create some financial management challenges for consumers. Because the transactions are paid via ACH out of a linked deposit account (rather than being debited instantly as the transaction is authorized), the potential exists for customers to overdraw their accounts and incur overdraft fees. This problem could be minimized if the decoupled debit card is the only payment method regularly drawing on that account (possible but not guaranteed) or the checking account is provided by the same company providing the debit card (I’d be curious to learn how Upgrade addresses this concern for customers that also have its Rewards Checking account).

The Investor’s Credit Card

Examples: M1 Owner’s Reward Card, BlockFi Crypto Credit Card, Gemini Credit Card, SoFi Credit Card

What is it?

Credit cards that offer enhanced rewards for customers that utilize the issuer’s investment products.

The M1 card offers 1.5% cashback on all purchases and higher reward rates (up to 10%) for purchases made with companies that the cardholder invests in through M1’s investment platform. Cashback can be automatically reinvested in the customer’s portfolio. The card has a $95 annual fee (waived if the cardholder pays for an M1 Plus subscription).

The Gemini and BlockFi cards offer crypto rewards for users of their cryptocurrency trading platforms. Gemini offers a 3%-2%-1% rewards structure for purchases made on dining, groceries, and all other purchases. BlockFi offers a flat 1.5% reward on all purchases, with special rewards for purchases made at specific merchants. Neither card has an annual fee.

SoFi’s card allows customers to earn up to 3% cashback on purchases when that cashback is allocated directly to paying down a SoFi loan, saving money in a SoFi deposit account, or investing (in either stocks or crypto) in a SoFi investment account. The SoFi card doesn’t have an annual fee.

Why I’m Intrigued

Rewards are a powerful behavioral driver. It’s nice to see that driver being applied in this product category to help consumers save and invest. The M1 approach of tying rewards to specific merchants that customers also invest in is clever. I like the flexibility SoFi gives customers to earn more rewards by investing, saving, or paying down debt.

Why I’m Concerned

Given the volatility, I’m not a huge fan of crypto rewards. I feel the same way about services that automatically convert a portion of your paycheck into crypto. I get the upside argument, but in practice, it seems more likely to encourage short-term speculation.

Final Verdict

It’s a bit of a mixed bag!

I like the debit card + credit product category. I also like the investor’s credit card category. The Klarna and Possible cards make no sense to me and seem like they’re just going to confuse consumers. The long-term impact of the credit builder cards on the credit bureaus’ data continues to concern me. And the rest of the products seem challenging to succeed with (particularly in the current VC environment), but more power to the founders that are building them.

Overall, it seems like fintech is doing what it does best – experimenting.