Most bank executives that you speak with tend to be quite rational.

Sometimes coldly so. I remember talking to a chief lending officer at a small regional bank operating out of the Southeastern U.S. about his need to mitigate the geographic concentration risk of his bank’s loan book and only later realizing what he was actually talking about – hedging against the risk of a bunch of his customers having their homes destroyed by a hurricane.

Now, to be clear, this is generally a good mindset for these folks to operate with. This is what bankers are supposed to do – dispassionately evaluate risk and return and allocate capital accordingly. And, for the most part, it is what they do.

Except when it comes to person-to-person (P2P) payments.

When you talk to bankers – especially community bankers – about P2P payments, rationality quickly gets tossed overboard. They start saying things like, “we can’t let ourselves be disrupted by fintech,” and “my granddaughter and all of her friends use Venmo. We need to offer P2P payments, or our customers will leave!”

There are no presentations of business cases or data-driven discussions about retention and customer acquisition costs and price sensitivity. It’s just, “we have to do this immediately, or we’ll go out of business.”

It’s irrational. Jarringly irrational.

And bankers aren’t the only ones.

I’ve noticed that P2P payments – which we can define simply, for the purposes of this essay, as the ability for consumers to easily send money to each other – has become something of a vision board for executives working in or near the financial services industry; a canvas on which to optimistically project their ambitions for the future.

These ambitions usually have a small kernel of truth at the center – some rational and achievable goal – but they have been inflated by a level of irrational exuberance that would make Oprah proud.

I’m not sure why P2P payments has become a magnet for executives’ most irrational aspirations, but it has. And I think it’s worth trying to unpack some of the visions that different financial services (and financial services-adjacent) companies have of P2P payments and what those visions tell us about the future of money movement.

So that’s what we’re going to do – jump through four different, wildly optimistic visions for P2P payments and try to pick out what is real and what is delusional.

Customer Retention!

The Vision: Stem the tide of customer attrition, especially Gen Z and Millennial customers, by offering modern P2P payments functionality (for free!) that can compete with the likes of Venmo and Cash App.

The Kernel of Truth: This vision has been the driving force behind the growth of Zelle – a P2P payments network for banks, launched by Early Warning Services in 2017 – which has grown to 2,400 financial institution members (up from 766 in early 2020).

Most of that growth has been fueled by community banks and credit unions (financial institutions with less than $10 billion in assets make up more than 90% of signed financial institutions on the Zelle network), which have proven very receptive to EWS’s pitch – if you want to compete with big banks and fintech companies, you need a modern P2P payments solution.

There is some evidence to support this pitch.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Modern P2P payments tools – services that enable consumers to digitally send and receive money via mobile apps and/or web browsers – have proven to be extraordinarily popular. By 2019 (just 10 years after Venmo, one of the first modern P2P payments tools, launched), 40% of the P2P payments made by U.S. consumers were made electronically using a payment app.

Impressive, but not terribly surprising when considering the costs of previous money movement options. For example, when Walmart introduced a domestic money transfer service through its stores in 2014, it was seen as a huge improvement over the status quo (Western Union and MoneyGram). Today, these “low prices” from Walmart look scandalous.

Since 2019, usage of P2P payments apps has surged, thanks to consumers’ increasing usage of digital services during the COVID-19 pandemic. A recent survey from Cornerstone Advisors found that:

A little more than half (56%) of P2P payments users said that, since March 2020, they send money using digital payments tools more frequently than they did before the pandemic. Just 16% said they send money less frequently than pre-pandemic.

And:

One-third of P2P users report sending larger amounts of money using P2P payments tools since the start of the pandemic, in contrast to the 23% who said they’re sending smaller amounts of money.

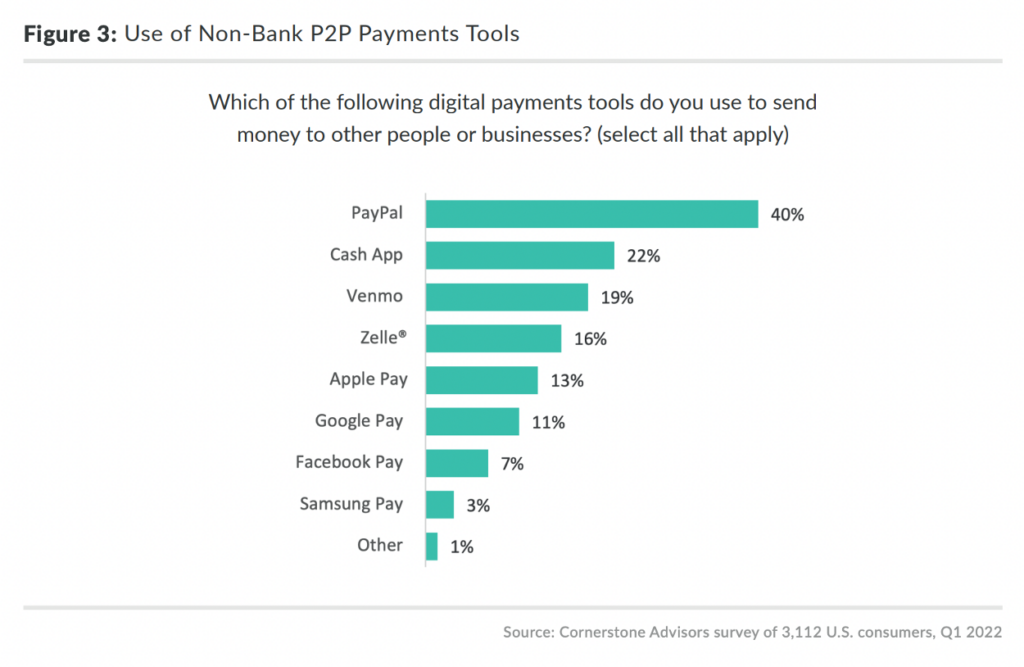

And that same Cornerstone Advisors survey found that many consumers rely on their banks’ P2P payments functionality and would be displeased if such functionality was taken away:

Among consumers with a checking account, six in 10 send money to other people using a payment service like Zelle or from their primary checking account provider’s website.

This capability is critical to consumers. Roughly three quarters of them said that if their primary checking account provider stopped offering P2P payments capabilities, they would take action. What would they do? The most popular actions were using an account from a different bank more frequently [30%], closing their existing account [24%], and opening an account with a different institution [23%].

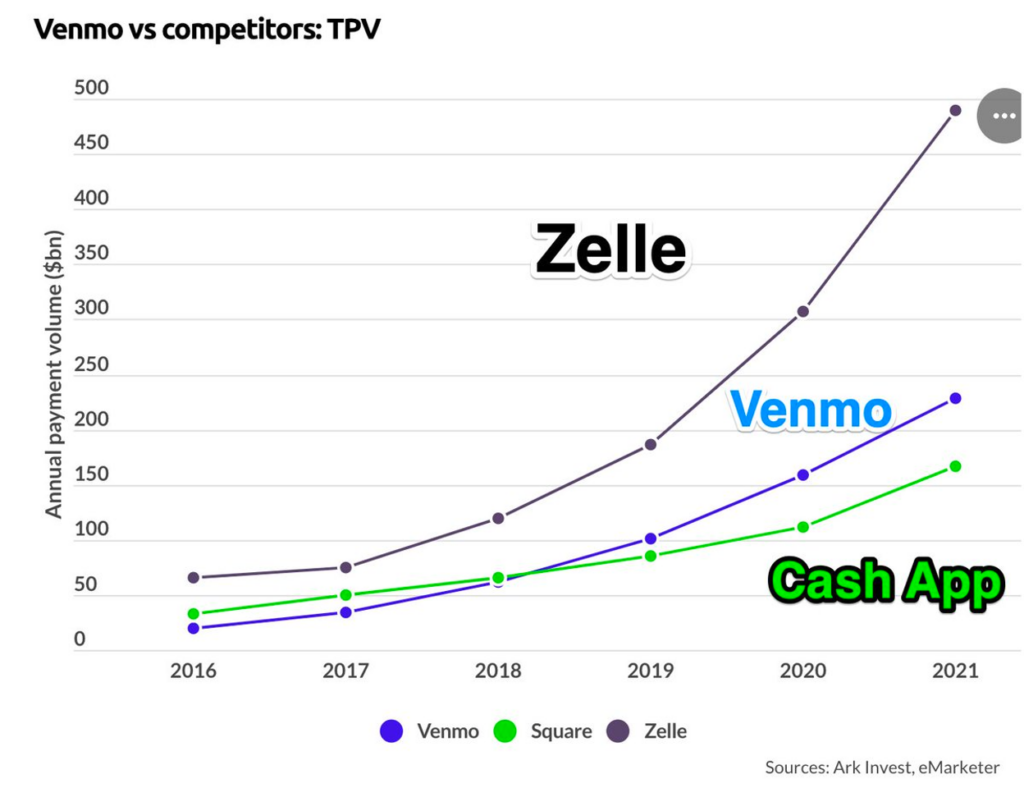

The Delusion: There’s no arguing with the fact that Zelle is thriving. EWS has been enormously successful in selling the vision of Customer Retention! to community banks and credit unions, and the expansion of Zelle’s network has driven a corresponding increase in payment transaction volume (1.8 billion payments made in 2021, a 49% increase from 2020) and, even more notably, in total payment volume ($490 billion in 2021, up 59% from 2020). I mean, just look at this chart that Rex Salisbury shared with me on Twitter:

Having said that, I’ll now admit – I don’t really buy the argument that EWS has been using to sign financial institutions up for the Zelle Network.

Consumers like and use P2P payments tools, yes. But would a community bank or credit union really be at a greater risk of losing customers if they didn’t offer Zelle (or something like it)? Consumers are already accustomed to using a variety of different apps and services to manage their finances. Indeed, the Cornerstone Advisors survey referenced above found that this is exactly what many consumers do when it comes to P2P payments:

If a consumer absolutely loved the community bank that they work with – let’s just imagine – would the lack of Zelle really cause them to leave? Wouldn’t they just keep using that bank’s products and just also start using Venmo or Cash App? And flipping that around, if they hated their community bank, would the addition of Zelle magically prevent that consumer’s eyes from wandering?

It’s important to ask these questions because Zelle isn’t free.

Far from it.

Here’s a nearly word-for-word conversation I had with a community bank executive who had recently implemented Zelle:

Me: How much does it cost?

Community Bank Executive: Roughly 90 cents per transaction.

Me: Wow, that seems pretty high. But I guess you’re at least offsetting that somewhat by charging a fee for the real-time transactions like Venmo and Cash App do.

Community Bank Executive: Nope. Every payment is instant, and we don’t charge for any of them.

Me: OK, but I’m assuming you’ve got a good handle on your fraud rates?

Community Bank Executive: Ohh no, we’re getting hammered by fraudsters.

Me: So … why are you doing this?

Community Bank Executive: Well, we just have to.

No! No, you don’t!

Faster Payments!

The Vision: Differentiate our P2P payments tool by enabling instant money movement by default.

The Kernel of Truth: The growth of Zelle, the only mainstream P2P payments app that moves money instantly by default, supports this vision.

Refer back to the chart above. One of the big reasons that Zelle is outpacing Venmo and Cash App in annual payment volume is that the average transaction size for Zelle is significantly higher (nearly $300 compared to roughly $60 for Venmo).

Why?

A big reason is that many of the larger P2P payments that consumers make – think paying rent or for a service like landscaping – are ones where the payer wants (or is required) to make the payment in a timely manner. Using a P2P payments tool that, by default, moves money instantly holds obvious appeal for these use cases. Indeed, data from EWS confirms that these consumer-to-small business use cases were the fastest-growing use cases between 2020 and 2021:

Businesses, including property managers, contractors, and health and beauty providers, relied on Zelle for sending and receiving money throughout the year. In 2021, payments received by small businesses increased 162% over the previous year’s totals.

The Delusion: Consumers, independent contractors, and small business owners all benefit from faster payments. This is true.

Do you know who else benefits?

Fraudsters.

Fraud and social engineering scams are not new phenomena in the world of P2P payments. The FTC recently sued Walmart for allegedly ignoring scams in its money transfer service (the same one that disrupted Western Union and MoneyGram back in 2014).

However, an elemental law of financial services is that any technology that delivers more convenience to consumers will, inescapably, also attract more fraudsters. This was the case when Venmo (and then Cash App) digitized P2P payments. And it has certainly been the case with the real-time-ification of P2P payments, courtesy of Zelle.

Faster payments is catnip for criminals and con artists. All that is required is a little social engineering to convince the customer to initiate the payment, and then poof, the money is gone, with no window of time to reverse the transaction or recover the funds.

EWS claims that fraud and scams impact only a tiny slice of transactions (less than 0.1%), but my conversations with bank executives that have implemented Zelle suggest that it is much higher (at least for mid-size and community banks). The Cornerstone Advisors survey also found a high incidence of fraud across all P2P Payment apps:

One in four P2P payments users said they have been a victim of fraud or scams involving digital payments

The problem has gotten so bad – and attracted so much attention from consumer advocates, regulators, and legislators – that EWS is considering making a rather dramatic change:

JPMorgan Chase, Wells Fargo and Bank of America are among the banks in advanced discussions to create a playbook for refunding customers and each other for illegitimate transfers, according to people familiar with the matter. The idea is to boost security and consumer trust in Zelle, the peer-to-peer payment system jointly owned by a consortium of banks, the people said.

Here is how the plan would work: If the banks determine that a customer was tricked into sending money, the bank that houses the deposit account where the funds were sent would return the money to the victim’s bank. The scam victim would get a refund from her bank.

This would be a huge concession for the seven large banks that own EWS, which have assiduously argued that Reg E consumer protections on unauthorized transactions do not apply to the vast majority of P2P payment scams.

And here’s the thing – none of this was really necessary!

Most P2P payment use cases don’t require the money to actually move instantly. All that’s required is an instantaneous acknowledgment that a payment has been initiated. You don’t need the $20 that Bill owes you for lunch in your account at this moment; you just need Bill to satisfy his social obligation to you. This was Venmo’s most important innovation – overlaying standard 1-3 day ACH transfers with a real-time social network for money movement. For most use cases, this is what consumers needed. And for the few use cases where the money actually does need to move right now, there are other rails (like the card networks) for Venmo to leverage while passing along a reasonable fee to the consumer.

If Zelle had gone this route, they would have saved themselves some headaches.

Super App!

The Vision: Leverage P2P payments as one of the initial building blocks in the development of a super app.

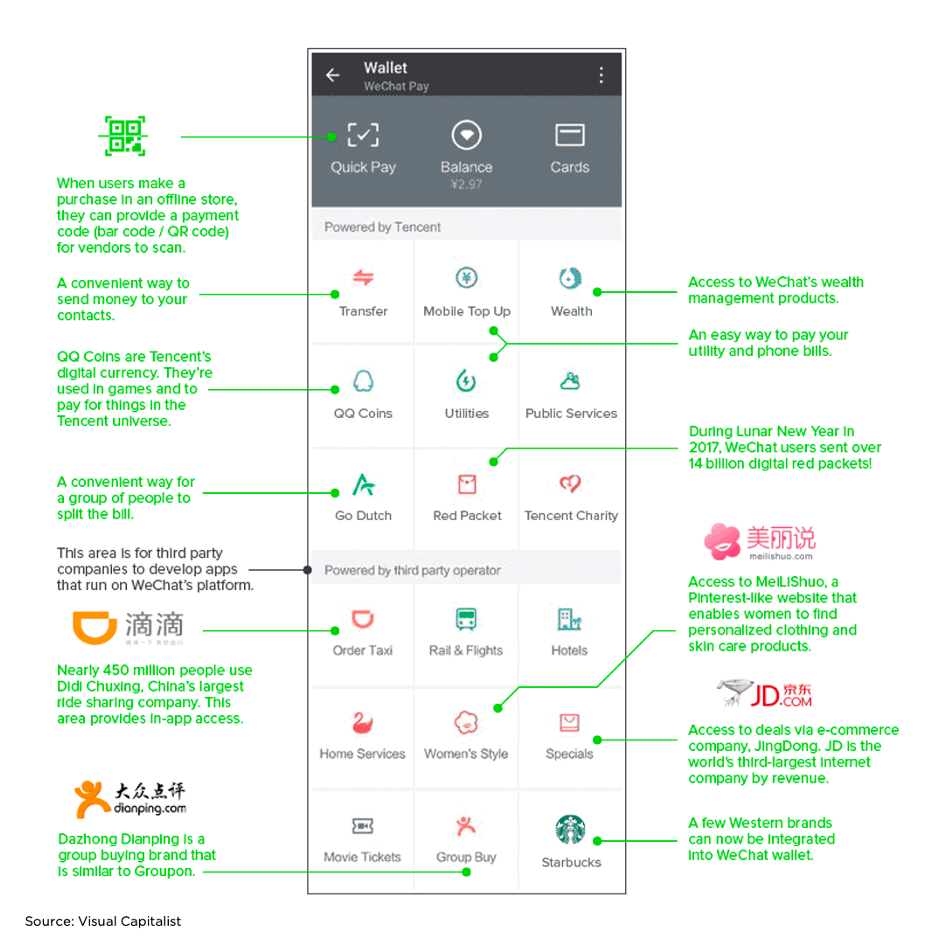

The Kernel of Truth: Super apps – enclosed digital ecosystems that enable users to accomplish a wide range of financial and non-financial tasks – do usually revolve around some type of P2P messaging and payments functionality.

WeChat and Alipay in China are the best-known examples.

And not only is P2P payments functionality central to the operation of a super app, but it can also be a cost-effective way to acquire an initial base of users. Cash App provides a good case study here:

Due to strong network effects associated with P2P payments (give me your $Cashtag and I’ll pay you back for lunch), Cash App has maintained an average customer acquisition cost of less than $5 per customer. That’s astonishingly good compared to traditional banks, which would be hard-pressed to acquire a new checking account customer for less than $250.

The Delusion: Super apps are essentially just app aggregators; they combine multiple apps into a single one, creating a more streamlined and convenient experience for users (one of the reasons super apps originally flourished in Asia was because Asian consumers owned under-powered smartphones that weren’t conducive to managing dozens of separate apps).

Every tech company in the U.S. wants to offer a super app.

The problem is that none of those companies wants to participate in another company’s super app. It’s like Highlander – there can only be one.

Many of the companies that have assembled the core messaging and money movement pieces necessary to execute a super app strategy see the opportunity ahead of them quite clearly.

The idea came to [PayPal CEO Dan] Schulman during a dinner three years ago with Martin Lau, the president of WeChat parent company Tencent Holdings. As the two dined, a picture began forming in Schulman’s head: Consumers could come to the PayPal app for more than just paying for things online. It could be their one-stop shop for all things shopping and finance.

Jack Dorsey’s Cash App plans to become a super app in order to rival PayPal as it aggressively integrates its buy now, pay later (BNPL) subsidiary Afterpay.

Block, formerly Square, executives outlined the plan to investors at an event on Wednesday.

The plans involved fully integrating buy now, pay later provider Afterpay into the company’s “ecosystem of ecosystems” and greatly expanding Cash App’s capabilities as it races against other payments providers to become a super app, according to Business Insider.

Cash App’s co-creator Brian Grassadonia, wanted to expand the app’s shopping and discovery features, alongside Afterpay cofounders Nick Molnar and Anthony Eisen.

“Afterpay can help transform Cash App into a super app,” Molnar said.

Musk has talked about using Twitter to create “X, the everything app.” This is a reference to China’s WeChat app, which started life as a messaging platform but has since grown to encompass multiple businesses, from shopping to payments and gaming. “You basically live on WeChat in China,” Musk told Twitter employees in June. “If we can recreate that with Twitter, we’ll be a great success.”

And yet none of them have gotten anywhere close to reaching the heights reached by Alipay and WeChat.

It’s really hard!

Perhaps the best evidence of this is Apple, which has everything you’d want when building out a super app – a huge base of captive users, complete control over its ecosystem, deeply integrated identity, messaging, and financial services capabilities, a community of third-party app developers that it has managed to keep under its thumb, etc. Apple has offered P2P payments as a part of Apple Cash for more than five years, and according to Cornerstone Advisors, only 13% of consumers use Apple to send money to other people or businesses.

If Apple can’t unlock a super app with P2P payments, it seems highly unlikely that any tech company in the U.S. will be able to.

Universal Money Movement!

The Vision: Enable every adult to send and receive money, anytime, anywhere in the world, instantly and for free.

The Kernel of Truth: We’ve saved our most ambitious vision for last!

This is the P2P-payments-as-a-public-utility vision, the one that causes Visa and Mastercard executives to wake up in terror in the middle of the night.

And it has some grounding in reality, especially in large, rapidly digitizing markets outside the U.S.

Let’s quickly run through two examples.

The first is the Unified Payments Interface (UPI) in India. Launched by the National Payments Corporation of India (which is governed by the Reserve Bank of India) in 2016, the UPI allows consumers to set up a virtual payment address (kinda like an email address, but for money movement) and use that address (via smartphone apps or offline via India’s digital ID system) to instantly make and receive payments, for free, 24/7/365. UPI serves a number of different purposes, including enabling more efficient disbursement of government benefits, accelerating the migration away from cash, and helping unbanked and underbanked consumers. It has been an unqualified success – in April 2022, nearly 5.6 billion transactions were carried out through the UPI, up from roughly 300 million transactions in August 2018.

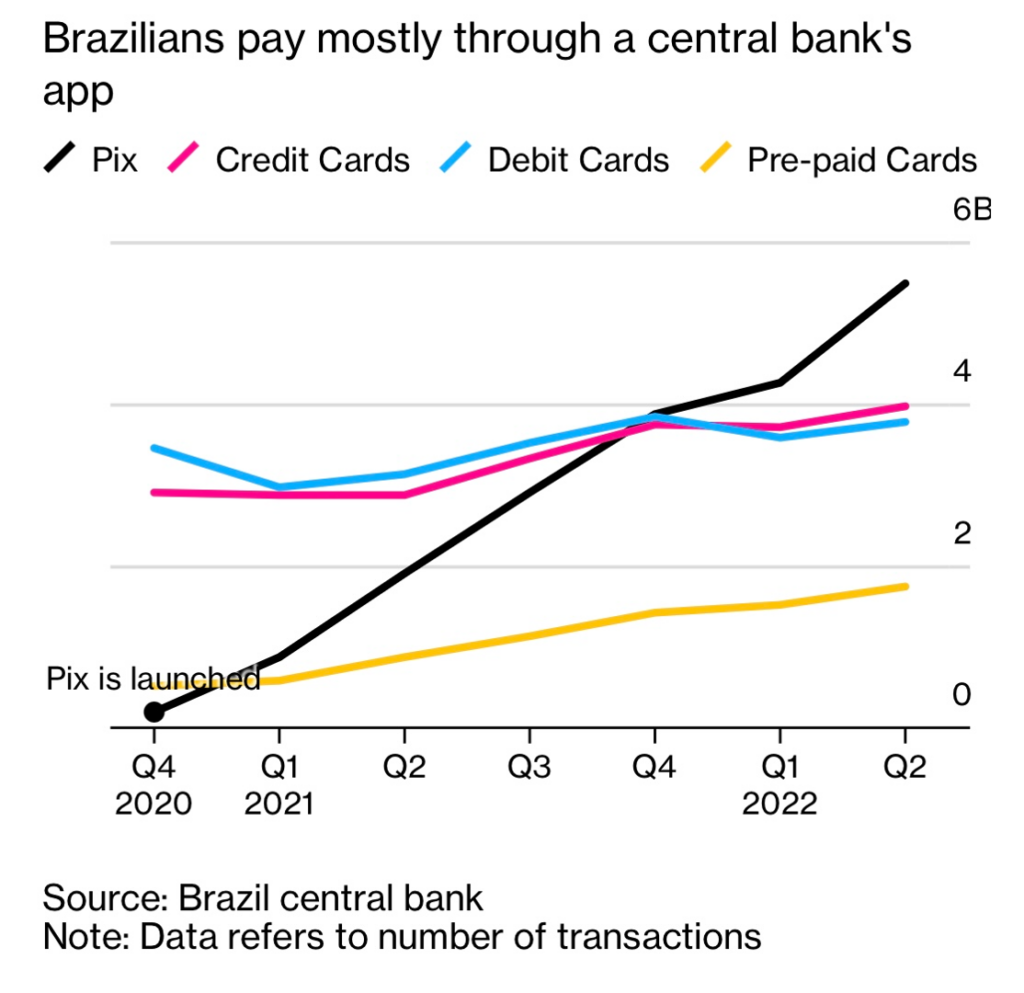

The second example is Brazil’s Pix, the fastest-growing national real-time payments system in the world, which is currently processing 2x more real-time transactions per capita than India:

Launched in November 2020 and developed by Brazil’s central bank (Banco Central Do Brasil), the PIX network provides free and instant settlement of digital money transfers within two accounts registered with participant institutions. Less than two years since implementation, adoption has exceeded expectations: PIX processes the wide majority of B2B payments, and over 75% of the adult population has either sent or received a payment via PIX. While initial adoption was mostly driven by the replacement of bank wires and cash payments in a B2B / P2P context, new features added in 2021 (e.g., payment in installments, scheduled payments, cash back, merchant initiation) and growing merchant adoption have led to an accelerating use for P2B transactions. PIX is now processing ~$250B in annualized P2B payments, equivalent to more than 40% of card volume and 20% of total consumer spend.

That last point is also worth pausing on for a moment. Pix hasn’t just replaced cash as the primary mechanism for P2P payments; it has also surpassed credit cards and debit cards as the primary P2B (person-to-business) payment method in Brazil, proving especially popular with small businesses:

The Delusion: So, could something like UPI or Pix ever exist in the U.S.?

In theory, yes, but if we’re being realistic, probably not.

But wait! I hear you saying. Isn’t the Federal Reserve doing this exact thing with FedNow?

Sort of, but not really.

Allow me to explain.

FedNow is a real-time payments system being built by the Federal Reserve. After many, many, many years in design and development, FedNow is (supposedly) going to be launched in late spring or early summer of this year. The service will be available for any bank in the Fed system (the settlement model will leverage participating banks’ existing master account at the Fed), and it will initially support payments up to $500,000 (although the default will likely be closer to $100,000).

FedNow is essentially a new payment rail, one that is faster and lower cost than pretty much any rail available to banks today. That’s cool! It will be valuable to banks, and some of that value will trickle down to consumers and businesses.

However, the Federal Reserve doesn’t appear interested in building a full-stack, public utility payments service, like India and Brazil (and many other countries) have done. Usage of FedNow will be restricted to banks, but they won’t be required to utilize it. Consumer fees will be left up to the discretion of banks, and added functionality will be built by the banks and their technology partners, not the Fed.

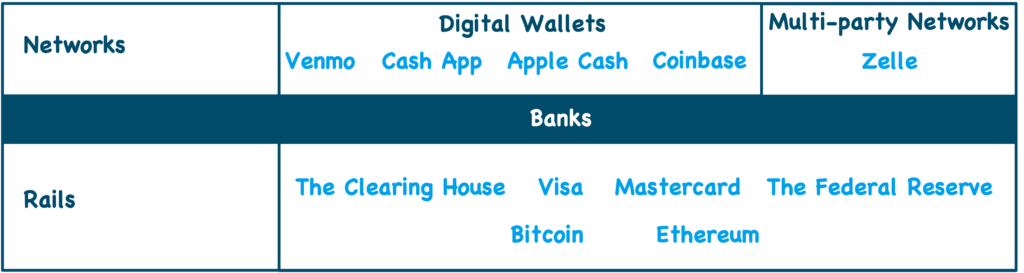

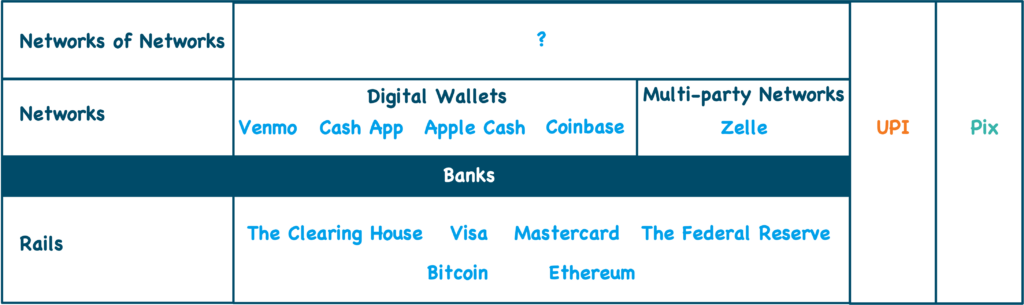

If you think about it as a stack, the whole picture looks something like this:

The payment rails all have different combinations of virtues – speed, cost, security – that make them better or worse fits for different use cases. The networks leverage different rails (usually a combination) and their own proprietary databases of user profiles to create easy payments experiences for the end customers. And banks provide the compliant on-ramps and off-ramps between the payment rails and the customer-facing networks.

Most of the networks encourage their customers to keep funds within their ecosystem, thus enabling the networks to reduce their usage of the payment rails over time and save money (these are often referred to as closed-loop digital wallets). Zelle, being owned by a consortium of banks, takes more of an open approach, facilitating an easy flow of funds between all participating network banks (although all users are required to use Zelle, of course).

In contrast to FedNow, UPI and Pix are vertically integrated payments solutions. They provide the rail (real-time, always-on money movement facilitated by the central bank) and the customer-facing network (most provide their own app as well as integrations with third-party apps as well as a central database of user profiles). They usually require an account with a licensed bank, but, in theory, they wouldn’t have to, given that the central banks are the ones operating these services.

We don’t have anything close to this in the U.S. Our regulators don’t build systems; they write rules. We’ll be lucky if we actually get FedNow this year.

The closest we might realistically be able to get to this Public Utility P2P Payments Service in the U.S. is another layer of abstraction on top of the customer-facing networks – a ‘network of networks’ if you will.

A solution built at this layer would be completely open. It wouldn’t require a customer to join a specific network in order to receive money from it. The customer wouldn’t need to download Venmo and Cash App and Zelle onto their smartphone; they would all just be integrated endpoints within an open ecosystem. The customer would simply specify where the money was going, when it needed to be there, and how much they were willing to spend to send the money, and the service would determine and execute the optimal money movement route.

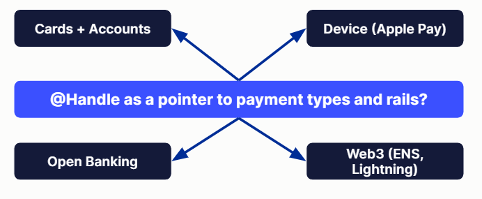

As I understand it, this is the vision for Alloy Labs’ CHUCK. It’s how Jack Henry has been talking about P2P payments since its acquisition of Payrailz. And it’s somewhat similar to the developer-oriented vision that Simon Taylor outlined for Twitter’s hypothetical payments service in an excellent essay a few months ago:

The Twitter @handle approach could create a different consumer experience by intentionally being more abstract. If each payment rail has its own gateways and domains, the @handle becomes a pointer to those.

What are the odds of success of building out an open payments solution at this ‘network of networks’ level?

I don’t know. I would imagine that some level of cooperation would be required from all the individual networks, which might be difficult given the “no, we want to be the super app!” mentality that I described above. But who knows! Maybe this is where we will eventually end up once Zelle and the P2P digital wallet providers get tired of fighting with each other for market share for a product that doesn’t make money.

Finally, let’s circle back to the “anywhere in the world” part of the Universal Money Movement! vision. After all, we’re living in an increasingly borderless world. Shouldn’t we consider cross-border payments an essential function of any modern P2P payments app?

Probably, but it’s going to be difficult to get there.

All of the P2P payments apps that we’ve been discussing in this essay are domestic services. They only work in one country. Adding in the ability to move money across borders introduces compliance risk (dealing with KYC and AML across multiple countries, with different regulatory requirements, is super painful) and FX risk (fluctuations in exchange rates between currencies can lead to losses in cross-border transactions if not managed carefully). These additional risks can certainly be mitigated (there are plenty of banks and fintech companies offering cross-border payments today), but it tends to add enough complexity and cost into the equation so as to not be worth it for most providers (including central banks!)

And before you say, “crypto solves this!” (boy, I haven’t heard that line in a while), remember – regardless of the rail being used to send the money, you still have compliance risk (assuming you’re planning to comply with the law) and FX risk (assuming the parties on either end of the transaction don’t want to keep the money in one token forever).

A Few Final Questions About P2P Payments

OK, phew! That takes us through the four quadrants of our P2P payments vision board.

Let’s wrap up with a few stray questions:

Why are community banks signing up for Zelle but not RTP? With all the talk about FedNow, it’s easy to forget that there’s already a real-time payments network in operation in the U.S. The Clearing House (TCH), a banking association and payments company owned and operated by a consortium of the 26 largest national banks, launched its own real-time payments (RTP) network in 2017. RTP also offers an instant payment ability, but adoption has been slow and mostly among large rather than small banks. This is because smaller banks have been reluctant to work with a network that was created by the big banks. But, like, EWS is owned by the big banks too! Why are smaller banks cool with EWS but not with TCH? BTW, community banks may be losing their cool with EWS in response to the company’s plan to require Zelle banks to refund customers for scams. Community banks that offer Zelle are reportedly PISSED about it (I’ve also heard that there’s some significant dissension in the ranks of EWS’s seven owner banks about this proposed change as well).

Does Reg E apply to fraud losses due to scams? As I mentioned above, all of the P2P payment providers strongly believe that it doesn’t because the customers are authorizing the payments. I think there’s a decent argument that it should apply (here’s Patrick McKenzie forcefully making that case), and I wonder if EWS’s move to have its bank members take on more liability (but not all of it!) is an attempt to head off possible regulatory intervention on this question.

How do we effectively limit fraud in real-time P2P payments? Putting more liability on banks is a good first step IMO because banks tend to summon up marvelous levels of ingenuity when they are responsible for preventing fraud losses. But what’s the next step? How do we actually throttle fraud in real-time payments while letting good customers sail through? My semi-educated guess is that it will require us to develop new consortium models that are able to identify risky receiving accounts (the places the scammers are tricking consumers into sending money to) by analyzing the network level (what is the reputation of the bank that this account is at?), the account level (is this phone number or email or device associated with high-risk accounts?), and the transaction level (is this combination of transaction characteristics concerning?)

Will P2P payments grow within context and audience-specific apps? I think we tend to imagine the future of P2P payments as continuing along the trajectory it’s currently on – a few big players all trying to increase the size and strength of their networks. But what if P2P payments evolves in a different direction? What if it fractures and becomes embedded in all of the context-specific and audience-specific apps that we are increasingly using? For example, could we see the emergence of P2P payments for college students within the apps they use to manage their education and campus social calendars? (Now that I think about it, a P2P-payments-enabled app that facilitates the resale of textbooks makes a lot of sense!) (Thanks to Itai Damti for suggesting this question!)

Is the future of P2P payments sending money and hints on how to use the money? I’m fascinated by the ability in Cash App to send people fractional stock and crypto, along with USD. You can literally embed a specific value judgment on how someone should invest their money inside the money that you are sending them! The best we used to be able to do in the old days was write a passive-aggressive note in the memo line of a check! How far can we take this? How far should we take this? Should I be able to send my brother $50 worth of a single-family residential property in Boise? Do you think he would take that the wrong way?

Created By

Alex Johnson

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

THe Fintech Takes Newsletter

Get breakdowns of the latest product launches, funding, acquisitions, and crypto news delivered to your inbox twice a week.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.