What happened?

Janet Yellen, Jerome Powell, and Martin Gruenberg shared an update:

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

So what?

This news capped off a rather wild few days, so to sort through it all, let’s assign some winners and losers.

Winner: SVB Depositors

The most important story here is that SVB depositors can get back to work this week. It was a stressful last four days, but payrolls are going to run on Wednesday, MVPs are going to continue being built and refined, and California vintners can refocus on their very important work.

I’m really happy to be able to type those sentences.

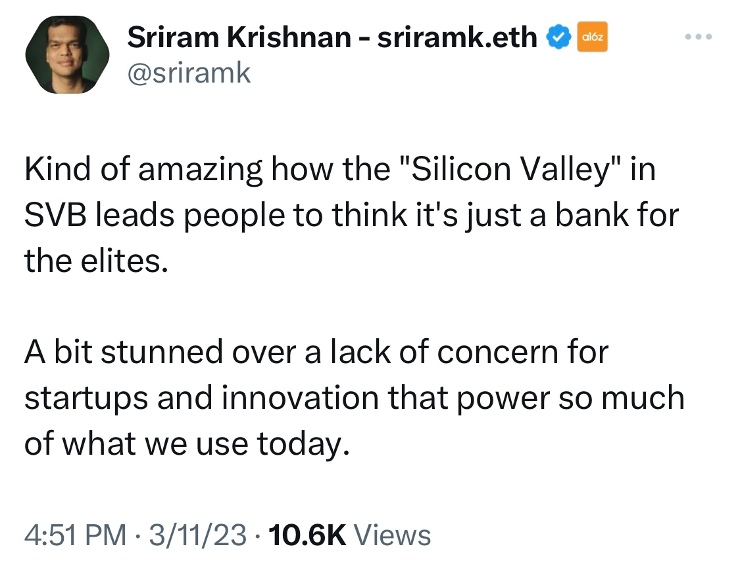

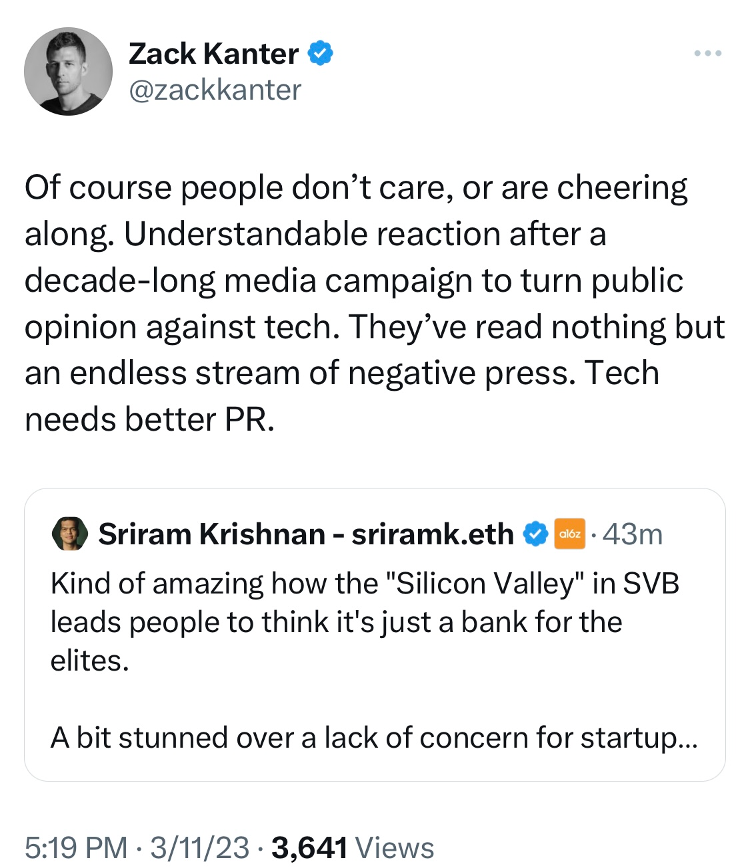

Loser: Investors on Twitter

After this weekend, we can divide investors into two groups – those who we didn’t hear much from because they were too busy helping their portfolio companies (often going to extraordinary lengths!) and those who spent 7 minutes reading about how this banking thing works on Wikipedia and then tweeting non-stop about WHAT WE SHOULD ALL DO OR ELSE.

Let us immortalize a few of them.

First, this guy.

Way to be super vague and ominous! That won’t cause any panic!

Unless your goal is to create panic and cause a bank run because you’re an infamous short seller.

Or a less famous short seller trying to make a name for himself.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

And then, of course, we have the pod boys, who I wrote about a bit in last week’s essay.

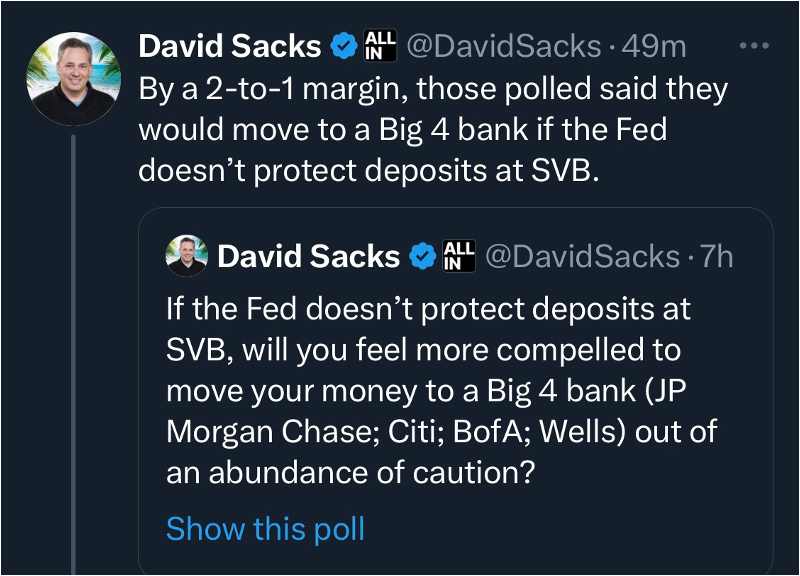

First up, David, who polled his Twitter followers in order to [checks notes] tell the federal government how to regulate all banks in the U.S.

Secretary Yellen started working at the Federal Reserve five years after this dude was born, but come on! A 2-to-1 margin! That’s overwhelming evidence, Janet!

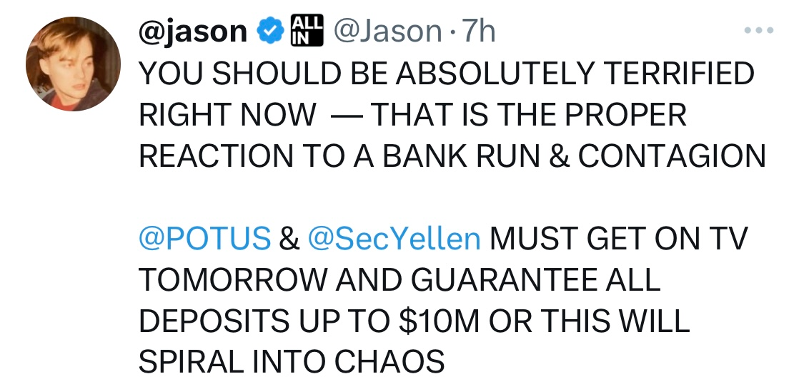

Then we have Jason, who apparently couldn’t get the caps lock disengaged on his iPhone but didn’t let that stop him from warning us.

What kind of chaos, Jason? What might that look like?

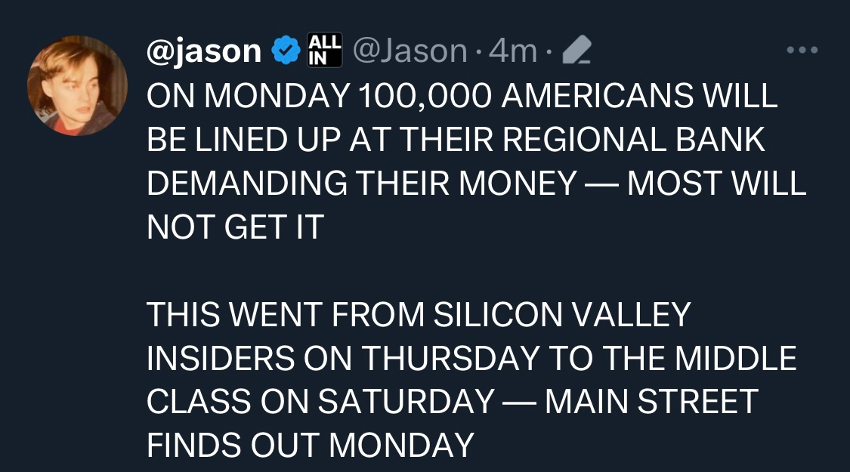

What happens then, Jason? What will those 100,000 Americans do? And, more importantly, who shall lead them?

I think Treasury, the Fed, and the FDIC did the right thing to address the crisis (more on that in a second), but even if I didn’t, I still would have been in favor of it just to get these people to shut the fuck up.

Indeed, I’d love it if the FDIC could go further.

Alas.

Winner: Federal Regulators

Shamir, who was an extremely calm and knowledgeable resource over the last four days, got it exactly right when he tweeted this on Thursday:

The FDIC, and federal regulators more broadly, are extremely competent at dealing with bank failures, and they demonstrated that this weekend. They have my gratitude for a job well done.

A couple of stray thoughts:

- The speed of last Thursday’s bank run seemed to catch regulators off guard. As did the rampant and unhinged panic among Silicon Valley luminaries. These factors likely made it more difficult for them to resolve the SVB situation without needing to resort to a larger intervention.

- I’ll be curious to see how this intervention impacts the sale of SVB’s assets and the balance between the FDIC’s urgency to complete the process and its mandate to get the best possible deal.

- Saying that taxpayers won’t bear the costs of this intervention makes for nice messaging (and helps smooth out political concerns), but that’s not really true. The FDIC is going to recover any losses to its Deposit Insurance Fund with a special assessment on banks, and banks are going to recover that special assessment expense by increasing costs for all of us. Dog bites man.

- The new funding program being set up by the Federal Reserve (details here) seems well-designed. It will allow any depository institution to borrow money by pledging the securities that have been wreaking havoc on many banks’ balance sheets as collateral. These assets will be valued at face value (rather than market value), which is a smart way to sidestep the interest-rate risk problem. Hopefully, just making this program available to banks (along with the FDIC fully reimbursing all depositors) will cut off any risk of contagion because I’m guessing that a bank actually taking out a loan through this program would still spook its depositors.

Loser: SVB’s Executives

As regulators made clear in their statement, these folks (and the executives at Signature Bank) are out of a job.

Makes sense why.

As my Workweek teammate Trung pointed out, the risk-taking was absolutely insane:

Combined with the CEO reportedly selling a decent chunk of stock a few weeks ago, I’m guessing that regulators and shareholders are going to have some questions.

Winner: The Fintech Ecosystem

Despite nearly giving myself a stroke watching the All-In podcast crew attempt to tweet new bank runs into existence, I have to say that, on balance, I came out of this weekend feeling very hopeful, and that is due entirely to the effort of so many folks in the fintech ecosystem.

When I talk to people who are new to fintech, I always tell them that my favorite part of working in this industry is the people, who are some of the kindest, most helpful, and intellectually curious humans I’ve ever met.

This opinion was validated by the incredible work that everyone in this ecosystem did to help each other navigate this unplanned stress test. I saw competitors cooperating to help founders find safe places for their money. I saw teams of people, at banks and fintech companies, working all weekend, with no sleep, to onboard new customers and answer questions. I saw VCs and executives using their personal capital to bridge startups’ cash shortfalls.

Incredible stuff. It’s a privilege to work in this industry.

Loser: Crypto

The failure of Signature Bank is another blow for crypto:

After the financial crisis, the lender grew rapidly and became an investor darling. In 2018, Signature hired bankers specializing in crypto as part of an effort to branch out beyond commercial real estate. Other banks were reluctant to take on crypto customers, and Signature became one of the crypto market’s leading banks.

That focus and a bespoke payments system for crypto companies helped the bank more than double deposits in two years. In early 2022, some 27% of its deposits were from its digital-asset clients.

The bank’s exposure to crypto became a problem as the year wore on. A market rout that deepened following the November collapse of Sam Bankman-Fried’s crypto exchange, FTX, drained billions of dollars in deposits.

Late last year, the bank said it was dialing back on crypto and parting ways with some crypto clients. It cut ties with the international business of Binance, the biggest crypto exchange. But the moves failed to calm investors. The spiral deepened after the closures last week of Silvergate Capital Corp., another bank to the crypto world, and tech-focused Silicon Valley Bank.

The bank’s failure threatens to further cut the crypto industry off from the regulated U.S. banking system. Some of the largest digital asset companies, including Circle Internet Financial Ltd., Coinbase Global Inc. and Payward Inc.’s Kraken, used Signature Bank.

U.S. regulators seem to have landed on a unified position for how they, ideally, want to treat crypto, which can roughly be summarized as “banks aren’t allowed to touch crypto, and any crypto thing that isn’t a regulated bank product is a security that needs to be registered with the SEC.”

The recent failures of Silvergate and Signature aren’t unhelpful in regard to this goal.

Winner: Appreciation for FDIC Insurance

If there was a Bad Takes Hall of Fame and the Hall had a Fintech Wing, this article from Eco would absolutely be displayed:

(Editor’s note – Eco scrubbed this article from its website, but thanks to the Wayback Machine, it lives on.)

A silver lining from this mess is, I hope, a renewed appreciation for the importance of FDIC insurance.

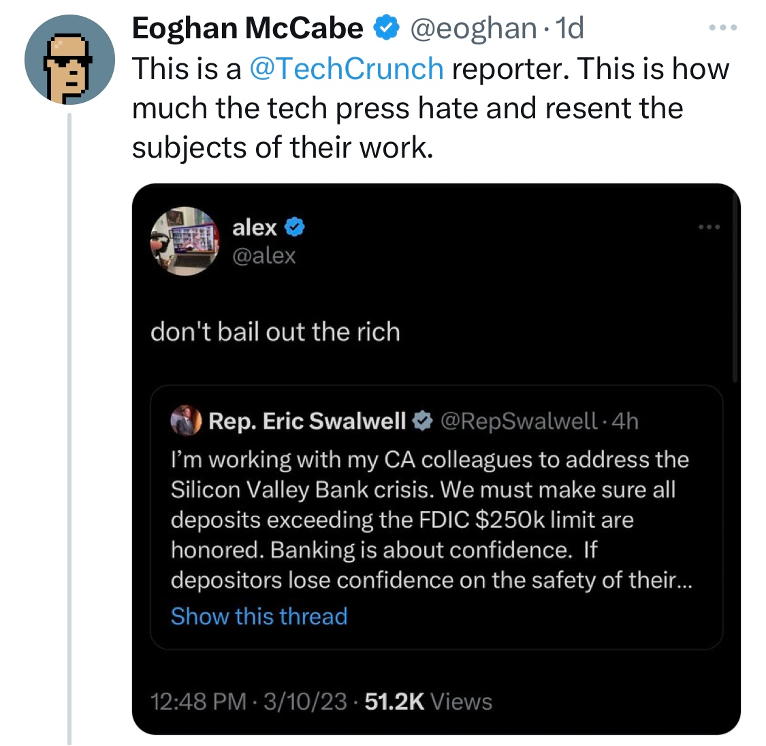

Loser: Tech’s Persecution Complex

Amidst all the tweeting, I noticed a specific line of thinking from some VCs and tech founders.

(Editor’s note – in reference to the tweet above, Alex at TechCrunch deleted his original tweet after … you’ll be shocked to hear this … he changed his mind upon getting more information.)

As a member of the tech media and someone who doesn’t live on either coast, allow me to say this – we were rooting for all SVB depositors to get their money back. We don’t feel disdain, resentment, or hatred toward you. We like California and New York (and Miami!) We enjoy the iPhones and food delivery apps you’ve created for us. We’re not wild about play-to-earn gaming, but that’s cool. No one bats a thousand. We’re not out to destroy you. We do think you could stand to chill out, just a touch, about your press coverage.

Winner: All of Us Being Spared From These Bad Ideas

Finally, I think we’re all winners because these two ideas didn’t end up being necessary.

OK, that’s it!

Here’s to a normal-ish week!

— Alex