My Workweek colleague Nick Van Osdol graciously agreed to chat with me about the intersection of fintech and climate tech, which is the most important crossover topic I’ve ever covered in this newsletter.

If you’re not familiar with Nick’s work, today is your lucky day. He is the brain behind the wonderful Keep Cool newsletter and podcast, which are required reading/listening for everyone in the climate tech industry (and, you know, humans in general).

In today’s conversation, which has been edited for length and clarity, we chat about the emergence of “green banks”, trends in climate tech investment, and the importance of enabling consumers to steer where their deposits go.

Alex: I want to start by asking you about the emergence of these green banking products. According to a consumer survey from Cornerstone Advisors, at least one-third of all consumers would be very interested in checking accounts with the following features: rewards for purchases made from sustainable brands, debit cards made from renewable or upcycled materials, policies that prevent deposits from funding fossil fuel exploration or production, and an option to plant a tree with every purchase roundup.

That’s a pretty diverse set of features, but it does a good job of describing the general feature set of these new green banks and fintech companies, like Aspiration and Atmos.

I’m curious – what’s your overall take on these green banks?

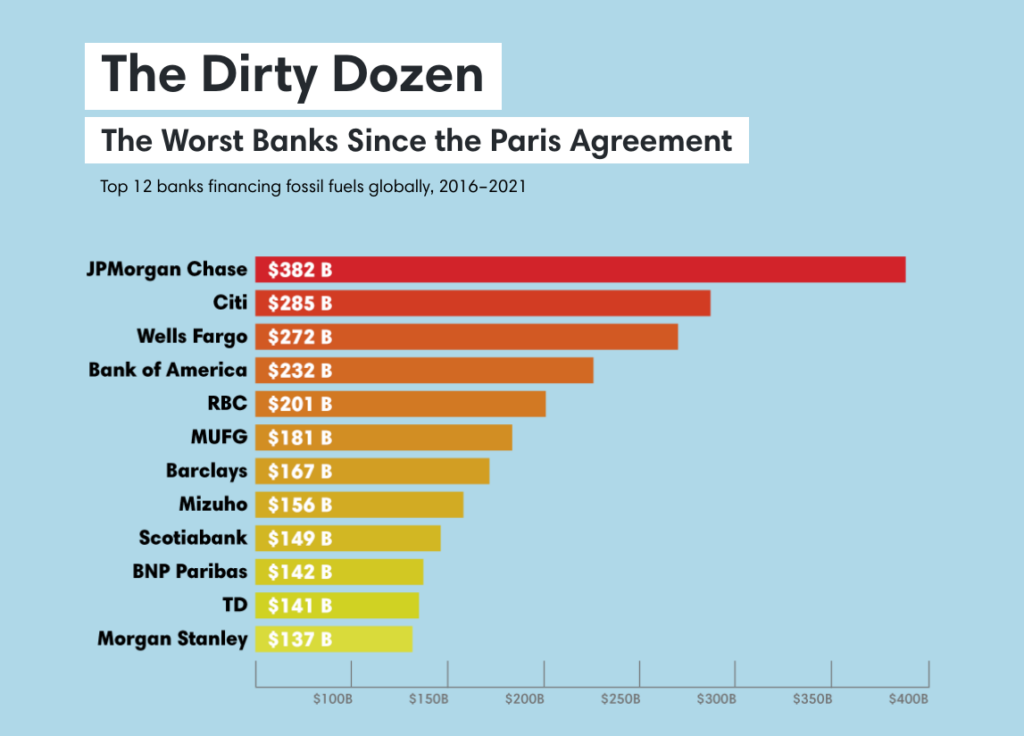

Nick: Yeah, that’s an interesting list because the ‘divesting from the fossil fuel industry’ one is, by far, the most impactful. I bank with Chase, even though I think about switching all the time and should switch, frankly. Chase has this massive fortress of a balance sheet, and it funds a lot of oil and gas infrastructure. And if you want to make a big impact on the climate, as an individual, moving your deposits so that they’re not funding that infrastructure is probably the single ‘biggest’ thing you can do. There’s plenty of debate about whether divesting or proactive investing (a la what Engine No. 1 does) is more impactful, but both approaches can make a serious dent at scale.

It’s been a while since I looked at Aspiration, but from my understanding, it’s focused on planting trees and other ecosystem restoration work. When done well, that can be super impactful. The challenge is that while there are some stellar ecosystem restoration projects out there, there are also a lot of mediocre ones. I would say that the modal project in this area doesn’t have the impact that you might imagine, especially when evaluated and reevaluated on long time horizons.

It’s not easy work to regrow a forest and then to make sure that it’s still standing in 10 or 15 years, let alone 50, and hasn’t been logged or destroyed by bark beetle or burned down. And if you’re planting a new forest, it’s likely not going to feature the biodiversity that an old-growth or existing forest would because you’re probably just planting a certain set of trees. So all of that is to say that tree planting is great, but it’s really difficult for project developers to consistently do it well and to maintain the benefits of reforested lands over time.

I think what Atmos does, which is a little more diverse, is pretty interesting. They are more involved in actual renewable energy infrastructure funding and lending, and that strikes me as a bit more impactful.

For example, if they’re using deposits to help build community solar projects, that is impactful on a lot of levels, and the playbook is a bit easier and more replicable than trying to regrow a forest in South America. And the benefit isn’t only in emissions abatement. It’s also better for that community; they probably save money and breathe cleaner air.

At the end of the day, however, the fact that your deposits with either Atmos or Aspiration aren’t funding fossil fuel projects is perhaps the biggest lever. And it’s a powerful one.

Alex: That’s a really good point, and it touches on a larger challenge I’ve noticed in fintech, which is this push and pull, when you’re building consumer-facing products, between stuff that looks and feels good versus stuff that actually has the most tangible impact.

The idea that every time I swipe my debit card, a tree gets planted somewhere is a really easy thing for me as a consumer to grok, right? I can understand that I did this thing, and now a good magical thing happens somewhere else in the world. And I don’t really need to know the details. I don’t really need to be responsible for any of the execution of that. I don’t really need to spend too much mental energy thinking about what’s happening or making sure that it’s happening the right way. It’s just a very clean sort of transaction in my mind. I swipe the debit card, and a good thing happened. I get to move on with my life.

But, to your point, I think a lot of things that are harder to understand from a consumer perspective actually have a great deal more impact.

Where our deposits collectively go and what our deposits are used for is way more important, in terms of impact, than any amount of trees that you could plant based on a roundup of your debit card transactions.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

As it relates to all of these green banking features, do you see these as viable standalone businesses – green banks – or do you think we might see these features migrate into all banking products as more companies try to appeal to this broad audience of consumers who are at least moderately concerned about climate change and the environment?

Nick: I think if I were Aspiration or Atmos, I’d be worried that in five years, every bank might present a decent amount of their work and products in a similar way. I could see a lot of these product features becoming table stakes.

I’m sure Wells Fargo and Chase are already seeing this shift as their customers want to align their product choices and behaviors with their values and are thinking about ways that they can design specific products to appeal to them. Big banks feel the pressure; BNP Paribas committed to not funding net new oil and gas infrastructure. It’s happening.

Alex: A big role that we have in the financial services industry is allocating capital, and, you know, candidly, banks are pretty agnostic when it comes to making money. If they see a good opportunity to make money, they will jump on it. Can you give me a lay of the land on where capital is being allocated in the climate tech space right now and what the funding dynamics are?

Nick: Yeah, for sure. Start with the early-stage venture side. It’s been really hot for the past three years, which is exciting, but the big question is whether and when we’ll see large exits into the public markets or other significant liquidity events. Will these investments ultimately perform for early-stage VCs? Venture investing is a long-term game, and we’re still a little early in the second major climate tech and cleantech venture cycle to make prognoses.

Alex: Right, that makes sense. Venture, as an asset class, is really reliant on those big, return-the-fund winners.

Nick: Everyone is trying to figure out what the next big bet is, and I hope that we see those bets get placed on hardware. If you want to really move the needle on climate change, you ultimately need a lot of hardware. Where I see a lot of oversaturation on the investment side is in software focused on stuff like the carbon markets and carbon emissions accounting. There’s just so much of that already, and I get that those are more traditional venture-backable businesses, but I think it’s going to be really hard for most of those businesses to stand out from one another over time.

Alex: That makes sense. It seems like one of the core challenges here is that there’s really boring stuff that needs to happen, which is capital-intensive and requires coordination with state and local government, and is really just not your typical tech/VC business. Stuff like nuclear power plants and upgraded electrical grids. But then there’s the really cutting-edge science and technology and innovation, which is also needed and is much more in the realm of at least some VCs.

And the trick is finding ways to meld all these together in order to actually make progress.

Nick: Right. That’s the challenge. You need companies like Tesla (whatever you think about them today) to make electric cars cool and attainable. They probably accelerated the adoption of EVs by 5-10 years. You need that really ambitious, innovative entrepreneurship. But, as you said, a lot of the problem is just doing the boring, big stuff that we have known how to do forever but that we’ve gotten away from. Like, if we had just kept building nuclear power plants in the 1970s, we’d still have plenty of other issues, but we’d certainly have less of an emissions problem in the power sector.

Alex: You’re a really calm and rational person, but I want to push you on the nuclear power plant point a bit because I know you have a rant you want to unleash on that topic, so the floor is yours. Go off.

Nick: The problem is that people want to have their cake and eat it too. There are problems with every form of power generation. You build a giant hydroelectric dam, which is great. Produces minimal full lifecycle emissions and provides very steady power. But there are people who (rightly) point out all the impacts it has on the (literal) downstream ecosystems. It might disrupt the migratory pattern of salmon, for instance, which is a really amazing thing. No one knows how they do it, but salmon swim upstream to the very ponds they were born in to mate. It might seem trivial to humans and our giant energy needs, but it’s a marvel of nature, and it’s a shame when something like that, that scientists still fully don’t understand, is disrupted. But I can say all that and still say we should build hydroelectric dams, as well as pumped hydro storage facilities, where possible.

Solar? The sun doesn’t always shine. Wind? Doesn’t always blow. And the grid wasn’t designed to handle variable power generation from all of these less-than-totally-reliable sources.

And look, concerns about nuclear are fair when balanced. There’s the waste that we have to put somewhere. There’s this tail risk of catastrophe, which is scary and grips people’s imagination. But we also need to acknowledge that we’ve gotten a lot better at building and managing nuclear power plants. And that they’ve killed far fewer people, even when catastrophes happen, than air pollution from coal power plants or catastrophic cave-ins at coal mines.

Alex: OK, excellent. I want to end by asking you to help me manifest some ideas that you’d like to see come to life at the intersection of climate tech and fintech. What would you most like to see?

Nick: Returning to our earlier discussion, I’d like to see consumers get a lot more control over where their deposits ‘go.’ If I want my deposits to help fund solar projects across disadvantaged regions in the U.S. or ecosystem restoration in South America, I should be able to help steer investment into those specific areas. I want a marketplace solution for what my deposits fund. As climate becomes more of a ubiquitous concern for consumers, I think we’re going to need to give them a lot more granular control over which problems they want to help solve and help them do it at a level that really moves the needle. Because this gets back to the ‘have your cake and eat it too’ problem. With your deposits, you should be able to fund what best aligns with your values. Whether that’s solar, reforestation, or something entirely different (within reason).

Alex: I like that!

Building on that point, I wonder if we need better banking-as-a-service infrastructure? Today, most neobanks and other fintech companies (including Atmos and Aspiration) work with a single, somewhat generic partner bank. They don’t have a lot of choices, so even doing something simple, like promising that no customer deposits will go into the oil and gas industry, is really tough.

But the direction that banking-as-a-service is already evolving is into this multi-bank network, where fintech companies can spread their accounts and deposits and loans out across a much wider set of partner banks, which all have different characteristics. Today, those characteristics are mainly balance sheet and business considerations (How many deposits can they accommodate? What price are they willing to pay? What is their appetite for risk?).

But I don’t see why you couldn’t add other layers to that. Like, if a fintech company is working with a customer and the customer says, “I want my deposits to do X, Y, and Z,” and some of those things are investing in specific climate projects, why couldn’t we have a BaaS infrastructure behind the scenes that is capable of doing that routing?

I know this would introduce a lot of additional complexity on the backend, but I think the general concept of BaaS evolving into a steering mechanism for consumers to direct their deposits with more intention is really interesting. And a nice side benefit of this would be giving the banks on the other end of that infrastructure a different, less price-sensitive way to differentiate themselves and attract and retain deposits. So it’s a really interesting idea to try to manifest.

Nick: Let’s make it happen!