Mario Gabriele, the creator and author of The Generalist, recently published a piece on the past, present, and future of Plaid.

With a word count just shy of 15,000, calling this thing comprehensive would be a big understatement. It’s an incredible collection of reporting and analysis, built on interviews with multiple Plaid executives (including CEO Zach Perret), investors, and customers.

If you haven’t read it yet — and, look, I get it, it’s 15,000 words – you really should. I’ve been a diligent student of Plaid (and the broader data aggregation space) for years, and still, I learned a ton from reading (and rereading) it.

However, one thing you will notice in reading Mario’s piece is that it takes a very Plaid-centric viewpoint. This isn’t surprising, given that Plaid paid to sponsor it and provided much of the input for Mario’s analysis.

To be clear, this isn’t a bad thing. Mario is very upfront about how The Generalist’s Partner Program works, and I think his analysis is, as usual, excellent. However, it did serve to obscure what I think is a critical part of the Plaid story – the importance of good timing.

As a general rule, humans don’t really like to attribute their success to factors outside of their control. So a piece like Mario’s was never going to highlight the moments of extraordinary good timing that Plaid has experienced throughout its history.

However, I think these moments in Plaid’s history provide a critical context for understanding the company.

Moment #1: Catching the Fintech Unbundling Wave

Data aggregation in the 2000s and early 2010s wasn’t an especially compelling market.

Building coverage and connectivity in those days – when digital banking was in its infancy and APIs were essentially unheard of within banks – was brutally difficult. There really were only two use cases that companies were willing to pay for: wealth management (providing insights for financial advisors) and personal financial management (banks, in those days, were irreversibly convinced that offering a Mint.com-like PFM experience was crucial for their success).

This was the environment that Plaid, founded in 2013, was born into. However, it would not be the environment that the company would grow up in.

As Mario relates in his piece, Plaid’s first customer helped push the company down a very different path from the one that the data aggregation behemoths in those days (Yodlee and CashEdge) had taken:

Around the time of Venmo’s initial acquisition [by Braintree], a friend at the company reached out to Perret and Hockey. The payments app sought a better way to connect to consumers’ banking accounts. Could they help?

It was an early inflection point. Signing Venmo validated the need for Plaid’s product and brought a wave of end-users through the door. Critically, it acted as an important proof point, too. A new generation of “fintech” companies had bubbled up in Venmo’s wake; those upstarts turned to Plaid to address their infrastructural problems.

Specifically, the infrastructure problem that Plaid solved for Venmo (and the other fintech startups that bubbled up in its wake) was account verification.

Account verification – the process of linking an external deposit account to a newly created account and validating customer ownership of that external account – was, traditionally, a stupidly long and friction-filled process. Two small test deposits would be sent, via ACH, from one bank to another with the goal of verifying the second account’s information and ownership. Due to the speed of the ACH network, the process typically took 3-5 days to complete.

Given that every additional 10 seconds added to a digital bank account opening process directly correlates to a 5% increase in application abandonment, you can see how unappealing account verification via microdeposits would be to fintech startups obsessed with customer acquisition and conversion rates.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Plaid’s solution – instant account verification via the consumer’s third-party banking credentials – was a game-changer. It knocked the account verification process down from 3-5 days to just a couple of seconds.

Plaid had built a great surfboard, but it wouldn’t have meant much if it hadn’t been followed by a massive wave. That wave was the great unbundling of financial services, which occurred, roughly, between 2010 and 2021. During that period, fintech companies, globally, attracted more than $1 trillion in outside investment, according to an analysis by the Bank for International Settlements. This investment fueled the creation of thousands of B2C fintech products, each designed to attack a very specific part of the traditional bank product bundle.

For Plaid, it didn’t matter that the vast majority of these products had challenging (or, in some cases, non-existent) business models. The VCs pouring money into fintech wanted to see growth, and the fintech founders that had taken those VC checks saw Plaid, in how it had helped Venmo and a few other early customers, as a critical ingredient for achieving that growth.

Thus, Plaid was able to harness this unprecedented wave of momentum in consumer fintech to raise progressively larger rounds of capital (a $12.5M Series A in 2013, a $44M Series B in 2016, and a massive $250M Series C in 2018), which it used to build out its connectivity and coverage among large banks (predominantly through screen scraping), and to buy connectivity and coverage among smaller banks (through arrangements with other aggregators) and into adjacent areas (Plaid acquired Quovo, a competitor focused on the wealth management space in 2019).

Moment #2: Thanks for the Antitrust

By the end of 2019, Plaid had achieved impressive scale – 11,000+ U.S. financial institutions, 5,000+ fintech apps, and hundreds of millions of consumer accounts.

It was big enough to be a threat.

Such a threat, in fact, that Visa decided to try and take it off the board.

Visa’s $5.3 billion acquisition offer, which was made in late 2019, was motivated by the network’s fear that Plaid’s scale could enable it to significantly disrupt its U.S. debit card business. As the subsequent lawsuit from the U.S. Department of Justice famously made clear, Visa saw Plaid as a sleeping giant:

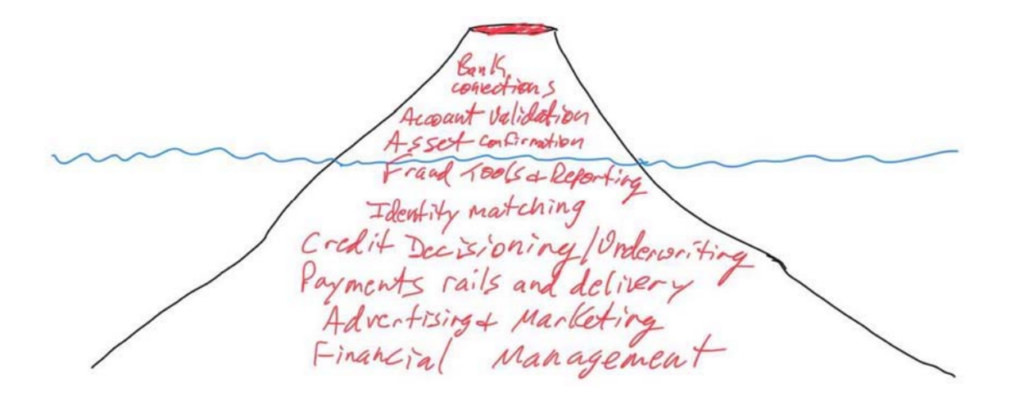

In evaluating whether to consider Plaid as a potential acquisition target in March 2019, Visa’s Vice President of Corporate Development and Head of Strategic Opportunities expressed concerns to his colleagues about the threat Plaid posed to Visa’s established debit business, observing: “I don’t want to be IBM to their Microsoft.” This executive analogized Plaid to an island “volcano” whose current capabilities are just “the tip showing above the water” and warned that “[w]hat lies beneath, though, is a massive opportunity – one that threatens Visa.” He underscored his point by illustrating Plaid’s disruptive potential:

2020 was a very weird year for fintech.

From a numbers perspective, global VC investment in fintech was nearly even between 2019 and 2020.

From a sentiment perspective, it was all over the place.

At the beginning of 2020, sentiment around fintech was cautiously optimistic. 2019 had been a banner year, in terms of both funding and growth in market share for fintech startups (and the infrastructure providers powering them).

Then the pandemic hit, and, initially, fintech froze along with the rest of the global economy, while investors and founders tried to understand what the impact of COVID-19 would be on their industry. However, by the end of 2020, it was abundantly clear that fintech was going to be one of the big winners from the pandemic-driven shift to digital channels.

It is against this backdrop that we need to analyze Visa’s attempted acquisition of Plaid.

At the beginning of 2020, a $5.3 billion exit for a private fintech infrastructure company was seen as an outrageously great outcome. I remember the discourse among fintech founders, operators, and investors at the time. They were dancing in the streets.

By the end of 2020, with fintech companies seeing explosive growth across all customer segments (Plaid saw its own customer base increase by 60% in 2020) and interest rates cut to 0%, $5.3 billion was seen as a bargain for Visa.

This is why the DOJ’s antitrust lawsuit, filed in November of 2020, was such a fortuitous event for Plaid.

As this excellent article in Fortune magazine on the Visa – Plaid breakup explains, the real killer for the deal wasn’t the strength of the DOJ’s antitrust argument itself, but rather the amount of time it would have taken to fight it:

Inside both Visa and Plaid, the feeling was that the Justice Department’s discovery process had given the companies a raw deal. Though the documents procured—the volcano sketch, the disclosure of boardroom deliberations—were damning, there was a sense that the DOJ had front-loaded its case in the complaint, and that it would have struggled to produce additional evidence at trial depicting a deliberately anticompetitive effort by Visa.

In any case, Visa and Plaid now found themselves on the verge of a drawn-out court battle—one that likely would have dragged on through 2021, if not longer—in order to consummate their merger. “I think a turning point for us was seeing how long it was going to take,” Plaid general counsel Meredith Fuchs tells Fortune. Fuchs notes that the DOJ’s “single-minded focus” on blocking the transaction—as opposed to working out a settlement—was another deterring factor. “It wasn’t like there was another route [for the Justice Department] other than the merger ending.”

The DOJ’s fervent desire to scuttle the deal was particularly strange when you consider that this was President Trump’s DOJ, and Republican administrations have traditionally taken a very lax, pro-business approach to antitrust enforcement. This was the case for the first half of Trump’s term, but not the second half:

Statistics show that after two years of relatively modest enforcement, the number of significant merger enforcement actions in 2019 and 2020, the final years of the Trump administration, were similar to the totals from the final year of the Obama administration. The number of merger challenges in 2020 exceeded any year of the Obama administration, and the number of merger challenges in 2019 equaled the Obama administration’s high-water mark in 2015.

And so Plaid entered 2021 as a free agent, which turned out to be another amazing bit of timing because 2021 was the absolute-never-ever-will-we-ever-again-see-something-like-this peak for fintech funding, with private fintech companies globally pulling in an astonishing $140 billion in funding.

Plaid, for its part, raised a Series D that year – $425M at a $13.4B valuation (up from $2.4B after its Series C), which was literally the best time in human history for a late-stage private fintech company to raise a round (Ramp, a similarly impressive late-stage fintech company just raised a $300M Series D at a $5.8B valuation, which represented a 28% cut in its value).

Talk about picking a good time to bet on yourself.

Moment #3: Building New Moats

And that brings us to today.

Since raising its Series D, Plaid has been investing like crazy to build out the lower levels of its volcano (h/t: Jason Mikula for helping me orient my metaphors).

This includes:

Identity verification and fraud management, which has been built around Plaid’s 2021 acquisition of Cognito for $250 million.

Payments facilitation (the thing Visa was originally afraid of), which comprises both risk-scoring solutions designed to speed up traditional ACH payments as well as new, multi-rail payment services centered around real-time payments.

Credit decisioning, powered by the cash flow data derived from Plaid’s core data aggregation capabilities. This is a newer area for Plaid, but one that it seems to be aggressively pursuing, often in partnership with regulators and non-profits.

This represents a significant shift in strategy. Prior to 2021, Plaid was very focused on owning as much of the data coverage and connectivity layer as possible, hence its acquisition of Quovo. Since then, Plaid has increasingly demonstrated a willingness to deprioritize this work in pursuit of building out the rest of its volcano, as its recent partnerships in the payroll space have illustrated.

I think this is smart.

Rules on open banking in the U.S., via Dodd-Frank Section 1033, are coming soon. The CFPB has told us that these rules will mandate that financial institutions offering deposit accounts, credit cards, digital wallets, prepaid cards, and other transaction accounts set up secure methods (such as APIs) to share consumer data, with consumers’ permission. Over time, these rules will expand to encompass other types of financial data, including lending data, investment and wealth management data, and (I’m guessing) payroll data.

Importantly, the CFPB has made it clear that their rules will be designed to encourage competition at an infrastructure level:

Third, we are exploring safeguards to prevent excessive control or monopolization by one, or even a handful of, firms. A decentralized, open ecosystem will yield the most benefits for creators and consumers alike. At the same time, there will be strong incentives for gatekeepers and intermediaries to emerge, extract rents, and self-preference. In consumer financial services, we have a number of highly concentrated submarkets: the credit reporting conglomerates, the card networks, the core processors, and more. It’s critical that no one “owns” critical infrastructure.

The implication of this for Plaid is significant – if we have new rules for open banking in place in the near future (the end of 2024 or beginning of 2025 seem most likely), which are designed (in part) to limit the competitive moats of any existing players in the data aggregation business, then the best-positioned companies will be those that have built value-added services on top of their core aggregation capabilities.

Since 2021, Plaid has been building a big head start in this area, which (according to Mario’s article) will be followed by a ramping down of R&D investment and a return to profitability in 2024. With the IPO window looking like it may be open again, this may turn out to be yet another well-timed move by Plaid’s brain trust.

The Residue of Design

Hopefully, at this point, I’ve convinced you that exceptionally good timing has been an ingredient in Plaid’s success to date.

However, I don’t want to leave you with the impression that Plaid’s success is solely due to good timing nor that good timing is solely the result of good luck.

As Branch Rickey, the famous President and General Manager of the Brooklyn Dodgers, once observed, “Luck is the residue of design”.

This is very much in evidence at Plaid.

As Mario observed in his piece:

Among its compelling properties, Plaid is a company that grasps the importance of a secret ingredient: time. It understands where and when time is needed and what it will add to its mixture. This quality manifests in unusual patience, focus, and a long-term orientation.

More specifically, I think Plaid deserves a lot of credit for the following:

Building for Developers. This was an unusual choice back in 2013 (Twilio was only five years old at the time, Stripe was four), but it paid off. In contrast to Yodlee and CashEdge, Plaid’s modern APIs and clean documentation were a dream come true for the fintech developers who came to dominate infrastructure and product development decisions in the mid-2010s.

Investing in policy. Starting with the hiring of John Pitts, Plaid’s Head of Policy and a former official at the CFPB, in 2018 (Fortune has a great anecdote on that in its story) and continuing to the present day. Plaid has been way ahead on influencing the development of open banking rules in the U.S.

Walking away from Visa. Mario covers this in a lot of vivid detail in his piece, but it bears repeating here – despite favorable tailwinds at the end of 2020, it still took a lot of guts to walk away from Visa and a $5.3 billion exit for executives, employees, and investors.

Executing on the product pivot. It’s one thing to sketch out a coherent strategy on a whiteboard. It’s another to actually execute it. I would give Plaid fairly high marks on the development of its value-added services, so far. The suite of IDV and fraud management tools is about as comprehensive as you’ll find in the market, even though some of the individual components may not be best-of-breed. And the incorporation of RTP and FedNow into its payments stack shows at least some willingness on the part of Plaid to cannibalize its own products, where necessary. Credit decisioning is a bit of a black box to me at the moment, so we’ll have to wait and see how that one develops.

Investing in better relationships with the banks. This has been another big shift at Plaid and, perhaps, the most difficult – defrosting the once-frigid relationships that it has with many of the biggest banks in the country. Plaid has invested significantly in personnel on this front (Ginger Baker, Plaid’s Chief Network Officer, is fantastic). It has also worked hard to accelerate the transition to APIs (banks justifiably loathe screen scraping) and get banks onboard as users (not just suppliers) of open banking data. There is a lot more work to be done here, but credit to Plaid for recognizing the necessity of this investment.

If Plaid’s perfect timing continues to hold, let’s make sure to remember that it was due, at least in part, to Plaid’s designs.

Created By

Alex Johnson

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

THe Fintech Takes Newsletter

Get breakdowns of the latest product launches, funding, acquisitions, and crypto news delivered to your inbox twice a week.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.