In the piece, I hypothesized that the emergence of modern fintech infrastructure would reduce the barriers to entry in financial services enough for this question to become extremely relevant – if a consumer can get a secure, compliant, and reliable financial product from anyone, why would they choose to get it from a bank?

The obvious answer, at least for some consumers, is that they wouldn’t.

This posed an intriguing follow-up question – who would they get financial products and services from?

Here’s 2021 Alex’s answer:

Just because anything can be fintech doesn’t mean everything will be fintech. Financial services will be a better fit for certain companies and industries than others. The monetary, legal, and reputational risks won’t be for everyone. Focus will continue to be a virtue for many entrepreneurs and executives who may view financial services as a distraction from their core business.

In much the same way that the remnants of old stars, scattered by supernovas, eventually coalesce and collapse back into new stars, the atomized state of financial services will eventually coalesce around new centers of gravity.

The question is, what will those centers of gravity be?

I have three guesses.

In 2021, these were all reasonable guesses.

Employer-sponsored fintech was a hot category, spanning everything from earned wage access (EWA) to savings and wealth management. Community-focused B2C fintech – most notably niche neobanks focused on specific demographic and values-based customer segments – were popping up all over the place. And merchant-centric fintech products and value propositions like BNPL were all the rage.

However, after experiencing the last three years – witnessing the death or strategic pivots of most niche neobanks and the slower-than-anticipated adoption of fintech by employers (outside of EWA) – I am left with only one answer: merchants.

And it’s not simply a process of elimination that is leading me to this conclusion. I believe that merchants are becoming the single most important and influential stakeholders in the financial services ecosystem.

Allow me to explain.

Serving Consumers (and Small Merchants)

Until relatively recently, consumer-facing financial services in the U.S., particularly lending and payments, were the province of merchants and specialty finance companies, not banks. As Joe Nocera points out in his remarkable book A Piece of the Action, this was primarily a cultural issue:

Within the culture of banking, it was corporations that mattered, not consumers. Making loans to large companies was the most prestigious activity in all of banking; making consumer loans, on the other hand, was considered slightly disreputable, and such loans were ceded to finance companies, which were also considered slightly disreputable.

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Until Bank of America came along.

Founded in 1904 by A.P. Giannini, the son of an Italian immigrant, Bank of America grew to become the largest bank in the U.S. by ignoring this cultural tradition and eagerly embracing the financial needs (particularly credit needs) of the average American consumer.

This crested, of course, with the launch of the BankAmericard – the first all-purpose credit card – in Fresno, California, in 1958.

There are a couple of things that are very important to note about the famous “Fresno drop”.

First, as is the case with all network businesses, Bank of America had to do something dramatic to overcome the cold start problem:

A successful credit card program requires the participation of not just customers but store owners as well. In fact, it requires thousands of store owners, who have to be recruited with the promise that there will be enough cardholders to make accepting the card – and handing over 6 percent of the purchase price to a bank – worth their while. At the same time the bank is recruiting merchants, though, it must also recruit cardholders – promising them that there will be enough merchants signed up to make carrying the card worth their while. It was a chicken-and-egg dilemma. Which came first, the customer or the merchants?

The “drop” was [Joseph] Williams’s [creator of the BankAmericard] solution to this problem. Rather than recruit cardholders, he decided to create them. He would mail cards to anyone who did business with Bank of America, free of charge.1

Second, the reaction of merchants to the introduction of the BankAmericard, was a bifurcated one:

The big merchants, like Sears, which had its own proprietary credit card, saw the bank’s entry into the credit card business as a form of poaching. Rather it was the smaller merchants who first came around. [Kenneth] Larkin [a lifelong Bank of America executive] remembers visiting a drug store in Bakersfield, hoping to persuade its owner to accept BankAmericard. “When I explained the concept of our credit card,” he says, “the man almost knelt down and kissed my feet. ‘You’ll be the savior of my business,’ he said. We went into his back office,” Larkin continues. “He had three girls working Burroughs bookkeeping machines, each handling 1,000 to 1,500 accounts. I looked at the size of the accounts: $4.58. $12.82. And he was sending out monthly bills on these accounts. Then the customers paid him maybe three or four months later. Think of what this man was spending on postage, labor, envelopes, stationery! His accounts receivables were dragging him under.”

This is important.

All merchants need to embed financial services – payments, lending, deposits, insurance – into their businesses. Commerce doesn’t work without them.

However, the largest merchants always prefer to control these services directly. They have the scale and resources to do it, and they’re incentivized to optimize their margins as much as possible. If you want to get Sears to accept your new credit card, you’ll need to get their customers onboard first (which BofA did with the drop), and you’ll need to cut them a sweet deal on the unit economics (BofA got Sears and other big merchants onboard by charging them a 3% merchant discount rate). And even then, they’ll still be pissed about it.

Smaller merchants are very different, as that story about the drug store owner in Bakersfield illustrates. Every financial services task that they are forced to handle directly becomes an anchor around their necks. They simply do not have the time or resources to turn those activities into profit centers or competitive differentiators, as Sears does. They are happy, no, thrilled, to pay 6% to offload that work onto someone else.

In 1958, Bank of America showed the banking industry just how much value could be created by empowering small merchants with innovative financial products and services.

Then the entire banking industry (including Bank of America) promptly forgot this lesson.

1958 – 2021

BankAmericard was a successful proof of concept, but it quickly became an operational nightmare.

Joseph Williams, who had never worked in lending, had predicted that the initial launch would lead to modest credit losses, with expected delinquencies around 4%. The actual delinquency rate was 22%, with fraud losses being significantly higher.2 Bank of America lost more than $20 million on BankAmericard within the first year.

Remarkably, the bank decided to stick with the program (with some major changes to risk management), and by 1961 it was turning a profit. However, due to the prohibition on interstate banking, Bank of America was forced to grow its credit card business by licensing it to banks in other states. This helped grow the program and build national brand awareness, but it created a massive coordination problem – merchants and banks across the country were constantly on the phone with each other, trying to authorize and settle customer transactions and resolve disputes.

In 1970, a manager at Rainier Bank named Dee Hock convinced Bank of America to spin off the BankAmericard program to a bank-owned consortium that would focus solely on solving these coordination challenges and further growing the network, which would later be renamed Visa.3

This was, obviously, the correct decision at the time, but it catalyzed an important change – merchants went from being partners of Bank of America (and its licensee banks) to network counterparties. Visa (and Mastercard) became the arbiters of disputes between banks, merchants, and consumers, and, for the most part, they spent the next five decades prioritizing the interests of banks and consumers over merchants. The emergence of credit card rewards, which Joseph Williams never envisioned, is a great example. They cemented the value proposition of credit cards to consumers, to the benefit of banks and the detriment of merchants (who were funding them).

These evolutions infuriated the largest merchants (Walmart took over for Sears as the standard bearer for raging against the card networks).

And smaller merchants? They mostly became an afterthought; too small, individually, to have much influence in negotiations with Visa and Mastercard, and too medium-sized to be appealing to banks (which prefer working with either consumers or large companies).

Fintech Wakes Up Small Merchants

This was the status quo in the U.S. until the emergence of the modern fintech industry in the wake of the Great Recession.

Fintech, as we know, specializes in bringing innovative financial solutions to segments of the market that have been ignored by market incumbents.

In the case of small merchants, which had, for decades, been mostly ignored by banks and the payment networks, this took the form of payments, lending, and commerce enablement.

It started as a trickle, with early innovators like Square introducing mobile payment acceptance and revitalizing merchant aggregation as a business model.

By 2021, with the COVID-19 pandemic driving a surge in digitization and ZIRP fueling an outrageous deployment of capital, it had become a flood. Fintech and fintech-adjacent companies focused on helping small merchants sell to consumers – Square, Shopify, Stripe, Affirm, Klarna – saw their valuations (public and private) explode. And this led these companies (and many more) to aggressively invest in building out their products and growing their customer bases, at an astonishing and unsustainable pace.

It was actually a lot like the Fresno drop – a once-in-a-generation investment that served to move the entire market forward.

In the case of small merchants, it woke them up.

Suddenly, they found that they had – through the plethora of new SaaS software tools at their fingertips – the ability to efficiently exert similar levels of control over the commerce experiences of their customers that Sears, Walmart, and Amazon had always had.

This manifested in numerous ways, all of which benefited small merchants tremendously.

Fast food restaurants and coffee shops using Square’s POS terminals discovered that they could exert a great deal more control over their customers’ tipping behaviors than they had previously thought. Shopify merchants found that by offering BNPL payment options to their customers, they could significantly increase average order values and significantly decrease cart abandonment rates. On-demand platforms like Doordash learned that intelligent embedded payment capabilities could streamline the user experience and reduce fraud.

Put simply, over the last 3-5 years, commerce has become more deterministic for small merchants and startups. You no longer choose to accept a particular form of payment out of fear that a customer walking in the door will be mad if you don’t. Instead, you design every step of your commerce journey (including payments and lending) to deliver the exact outcome you want.

Now, obviously, not every merchant has attained an Amazon-like sophistication when it comes to deterministic commerce. In fact, I would argue that most merchants are still in the very early stages of experimenting with these new tools. It’s still very common, as a shopper, to encounter the “NASCAR checkout page”.

That said, small merchants (and the many fintech and commerce enablement companies that are vying to serve them) are working to become more sophisticated. I am seeing this continuing evolution playing out in a few different areas:

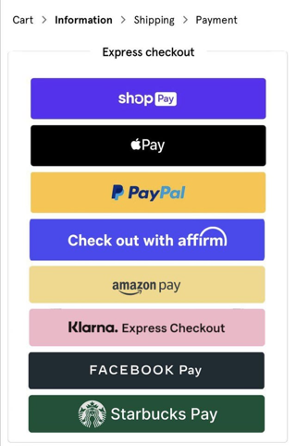

Closed-loop Networks. The idea here is to create a unified environment in which buyers and sellers can discover and transact with each other without ever having to utilize an external payment network or other financial service. On a macro level, I see this starting to play out in merchant ecosystems that are controlled by companies that also have scaled-up consumer financial services businesses. Block, with its Square and Cash App ecosystems, is probably the best example. Klarna and Affirm have the potential to get here. PayPal theoretically does too. Even Shopify has dipped its toes in these waters with its consumer-facing Shop app. On more of a micro level, I am starting to see this manifest with infrastructure providers like Ansa, which just raised a Series A to help coffee shops, quick-service restaurants, and other merchants with habitual, low-value transactions construct their own closed-loop payments environments (a la Starbucks).

Digital Wallets. The basic concept is to create a non-leather container (an app, a secure chip in a smartphone, etc.) that consumers can load money into and then use to transact with a variety of merchants (and, in the case of P2P payments, other consumers).4 Several of the closed-loop network providers mentioned above started the consumer side of their networks with digital wallets. Apple and Google have also gotten into the digital wallet game with Apple Pay and Google What’sItCalledTM. Digital wallets work through a variety of technologies at the physical point of sale (NFC, QR codes, etc.) and compete for limited real estate on e-commerce checkout pages (Stripe has thrown its hat, partially, in the digital wallet ring with its Link product, which is focused on optimizing checkout page conversion rates).

Embedded Finance. The SaaS-ification of every industry has made it substantially easier to embed financial services for merchants directly into the software that they use to run their businesses. Several of the closed-loop network providers mentioned above built out the merchant sides of their networks with embedded finance capabilities. However, the growth of embedded finance, as a category is increasingly being found in more verticalized niches, where commerce enablement platforms for specific industries (Toast for restaurants, MindBody for wellness businesses, etc.) leverage their customer data to build narrowly-tailored financial products and services.5

Obviously, there’s a lot of overlap between these different areas, and each presents its own opportunities and risks to the merchants that dabble in them.

But still, the opportunities to dabble have increased exponentially in the last 3-5 years, and that is undoubtedly a positive development for small merchants.

It also presents a risk to banks.

Traditionally, for all but the biggest merchants, commerce has always been the tail of the financial services dog. An area that banks could pay attention to or not, with few meaningful consequences either way.

Today, for merchants of all sizes, commerce is becoming the tail that wags the financial services dog.

Banks have to worry about the choices that all merchants (not just Walmart and Amazon) are making because those choices (expressed through commerce enablement platforms and fintech infrastructure) are playing a larger and larger role in determining the financial decisions that those banks’ customers are making.

Banks, to their credit, seem to have woken up to this threat. They are beginning to invest and innovate in the same veins that fintech has been mining:

Closed-loop Networks. The most obvious example here is Capital One acquiring Discover6, which Richard Fairbank explained by saying, “This deal accelerates our long-standing journey to work directly with merchants.” JPMorgan Chase, which also expressed an interest in acquiring Discover, has a number of new, merchant-focused initiatives underway, including a first-party advertising business and a biller-focused pay-by-bank product, both of which could (in combination with JPMC’s massive consumer business) be the seeds of a closed-loop network. Additionally, several large banks (Citizens Bank, U.S. Bank) have recently launched their own merchant-focused BNPL offerings (these are distinct from the BNPL features that large issuers like American Express have added to their credit cards), which they have tied (to varying degrees) into their consumer-facing products and channels.

Digital Wallets. The big play here is Paze, the digital wallet built by Early Warning Services (EWS), the fintech infrastructure provider owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo. As it did with Zelle, EWS should be able to leverage the market share of its owner banks to help solve the cold start problem for Paze (EWS claims to bring 150 million credit and debit cards to the table on day one). However, it’s still unclear to me what reasons merchants might have to carve out room on their e-commerce checkout pages for Paze.

Embedded Finance. Obviously, banks have always played a role in embedded finance. For the most part, you can’t do embedded finance without a licensed bank sitting somewhere in the stack (i.e. BaaS). However, in the last few years, larger banks such as Fifth Third, JPMC, and (briefly) Goldman Sachs have invested in owning more of that embedded finance stack, particularly for embedded payments and other transactional, non-balance sheet use cases. This has been the very quiet story playing out beneath the surface of all the recent BaaS drama, but I expect it to become a bit more prominent in the years to come.

As is the case with all fintech innovations, banks have some natural advantages when it comes to competing to address the financial services and commerce enablement needs of smaller merchants. However, after squandering a 60-year head start, they now also have a lot more competition.

We’ll see who (besides the merchants) ends up winning.

It’s difficult to imagine. Bank of America sent roughly 60,000 pre-activtaed credit cards to their customers in Fresno, without them asking and with no warning. Just, boom. Now you have a credit card. Have fun out there. This practice of dropping credit cards onto consumers’ unsuspecting heads was banned in 1970. ↩︎

A fun type of fraud, which was possible because all the cards were pre-activated – criminals would steal newly printed BankAmericards straight from the warehouse and then ransom them back to the bank. ↩︎

If I had a real fintech time machine, my first stop would be to observe the negotiations led by Dee Hock to spin off BankAmericard into Visa. Hock was 39 years old when he convinced the largest bank in the U.S. to give up control over its most profitable asset. That blows my mind. ↩︎

This interview with the GM of Fintech at Toast gives a good window into the thinking that goes into building these verticalized embedded finance offerings. ↩︎

This is a fun twist of irony because Discover was originally the credit card division of … Sears! ↩︎

Created By

Alex Johnson

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

THe Fintech Takes Newsletter

Get breakdowns of the latest product launches, funding, acquisitions, and crypto news delivered to your inbox twice a week.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.