This is the most important lesson I’ve learned writing Fintech Takes:

In keeping with this spirit, I’ve made it a habit in this newsletter to periodically share a list of all of the dumb questions that I’ve been thinking about.

It’s been a while since I last did it (and actually, the questions from my last post turned out to be decently insightful, if a little crypto-heavy), so I thought it was time to do it again.

So here it is – my list of foolish fintech questions.

As always, please reply to this email or hit me up on LinkedIn or Twitter if you have thoughts on any of these (or questions of your own that you’d like to share).

How do we ensure fintech companies’ operational resilience?

On Monday, I suggested that perhaps we shouldn’t allow FBO accounts to be used in BaaS.

As expected, this elicited some passionate disagreement. The crux of the pro-FBO account argument is that A.) they are the only practical solution for integrating with community banks’ legacy core systems, and B.) they can be implemented in a safe and responsible way. That requires (among other things) that the bank maintain or ingest data from a real-time ledger, avoid co-mingling money from different programs (an easy way to do this is to maintain one FBO account per program), and have strong reconciliation and monitoring controls in place to alert the bank of any discrepancies.

That’s a very fair (and very nuanced) perspective, and I appreciate multiple folks sharing it with me. I completely agree that BaaS via FBO accounts can be done in a responsible.

However, what this Synapse/Evolve mess has driven home for me (more so than the similar mess that engulfed Voyager and Metropolitan Commercial Bank a few years ago) is that just because BaaS via FBO accounts can be done responsibly doesn’t mean that it is being done responsibly today or that it will be moving forward.

And that’s a problem because, as the early outcomes of the Synapse bankruptcy dispute are making clear, there’s no safety net for customers hanging underneath fintech.

In my Fintech Office Hours event this week, I was delighted to be joined by my bank nerd friends Kiah Haslett, Jason Mikula, and Jason Henrichs. During the conversation, Kiah and Mikula both reminded the audience that FDIC insurance (should it be available on a pass-through basis to the end customers of Synapse’s fintech clients) only protects against the threat of one of Synapse’s bank partners failing. Not Synapse itself.

This is both obvious and incredibly important. Neither Evolve nor any of Synapse’s other bank partners appear to be in danger of failing. And yet, the end customers on the Synapse platform are already losing access to their funds and essential banking services.

Who do those customers call? Who is looking out for them? What recourse do they have (apart from the slow-moving processes of Chapter 7 bankruptcy)?

(Editor’s Note – Please spare me the caveat emptor arguments. It’s not reasonable to expect consumers and small business owners to parse neobank terms and conditions to understand the nuances of bank-fintech partnerships. They expect bank and bank-like service providers to be safe.)

Somehow, over the last couple of decades, we’ve managed to mostly avoid this problem.1 When customer-facing fintech companies failed, they did so quietly and in an orderly fashion. But there’s no reason that fintech companies can’t end in a much more dramatic and messy fashion (and, indeed, crypto companies seem incapable of failing in any other way). And when that happens, consumers and businesses that were relying on those companies discover just how screwed they are.

The Acting Comptroller of the Currency recently testified to Congress that federal banking agencies (including the OCC) are working to improve banks’ operational resilience:

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Another critical area for banks to address is operational resilience, which ensures that banks can adapt to and withstand or recover from disruptions. … These disruptions may impede services, like payments, clearing, and settlement, or adversely impact systems or corrupt data. Ensuring that critical operations and banking services can withstand or recover from disruptive events requires planning, prudent investment, well designed systems, and regular testing. To this end, the federal banking agencies have been engaged in discussions to consider potential changes to the operational resilience framework.

I’m becoming increasingly convinced that someone needs to be providing this same type of regulatory oversight for fintech companies.2

How do money management and money movement change when a large percentage of consumers’ liquid assets sit in non-cash vehicles?

Liquid assets used to be a relatively small category. You had cash, bonds, mutual funds, money market funds, CDs, and stocks.

Fintech has really expanded the field. It has enabled companies to capture and store value in a number of different, cash-like mechanisms. This includes everything from gift card balances and stored-value accounts to reward points to P2P payment balances to crypto tokens to in-game currencies and other assets in video games.

It’s easy to see how the use of these new cash-like stored value mechanisms will become more popular over time, as the utility of the apps, platforms, and ecosystems promoting or requiring those mechanisms garner more and more use.

How do consumer protections around things like fraud and disputes and UDAAP apply to these new liquid assets? How will consumers be able to holistically manage their finances when their money is fractured across all of these apps, platforms, and ecosystems?

I don’t know, but I am glad that the CFPB is thinking about these questions.

Is embedded back-office software the new embedded finance?

Embedded finance is getting complex

The simple version – an infrastructure company enabling a non-finance brand to embed financial products like loans or deposit accounts into its product – is seemingly morphing into a fight to embed financial-adjacent back-office software into the products of those non-finance brands.

Two examples:

- Embedded payroll: Companies like Check and Rollfi are enabling vertical SaaS companies and other software platforms to offer their business customers payroll and benefits solutions directly within their products.

- Embedded accounting: Companies like Layer are now doing the same thing for accounting.

It’s fascinating because controlling the payroll or accounting system would give the infrastructure provider (and its vertical SaaS clients) a path to providing all kinds of related financial products (deposit accounts, loans, insurance, etc.) to end customers, from an even greater position of strength.

How big is the market for better KYB solutions, and how many suppliers can that market support?

Know Your Business (KYB) is a HOT category right now. Among the newer startups in the space, you have Baselayer, Ballerine, Coris, TrueBiz, Parcha, Accend, and Greenlite.

To say nothing of Middesk, which isn’t exactly old, but that feels, in comparison, like the elder statesman in the room.

My goodness! That is a lot!

I know many of the folks at these companies, and they’re all very sharp. And this is an area in financial services that hasn’t, historically, gotten a lot of love.

But maybe it’s getting a bit too much love now?

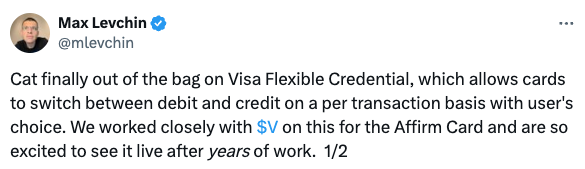

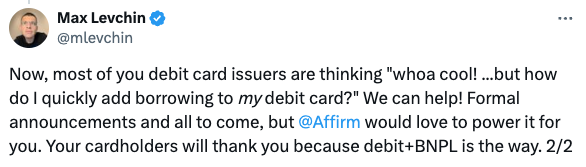

Did Visa just productize the Affirm Card?

Visa announced a slew of interesting new things this week. One is the Visa Flexible Credential:

One of several new product features is the Visa Flexible Credential, which enables banks to issue a single card that toggles between payment methods. This enables consumers to choose to pay via credit or debit, spread payments out in four equal installments, assign payment to a virtual card with custom controls or pay with points.

For example, consumers could use their bank’s online platform to set preferences so purchases under $100 are paid by debit, purchases over $100 go to credit and specific purchases could be designated for installment loans through the bank or purchased with a bank’s rewards points, said Mark Nelsen, Visa’s head of product for consumer payments.

My first two thoughts when I saw this were:

- Finally, Matthew Goldman’s vision for Wallaby is finally feasible (the perils of being too early!)

- This seems a lot like Visa just productized Affirm’s debit card (which allows users to convert specific purchases into installments).

In the case of point #2, apparently, that’s exactly what happened:

Whoa! Pretty interesting!3

Should Klarna buy Ansa or Accrue?

Someone on Twitter (forgive me, I can’t remember who) astutely pointed out that gift cards and merchant-specific stored value wallets can be considered Pay Now, Buy Later (PNBL).

This sent me down a whole rabbit hole, and I wondered why none of the big BNPL providers have (to my knowledge) built or acquired merchant payment and loyalty capabilities to complement their flagship lending product.

Why does Klarna not offer me Buy Now, Pay Later, Save Now, Buy Later, and Pay Now, Buy Later?

Acquiring a company in this space (Accrue, Ansa, etc.) would seem like an obvious way to round out their payment product stack while bringing them into new merchant categories and use cases.

How, if at all, are Visa and Mastercard applying their expertise in fraud and dispute management to pay-by-bank, which they are both pushing through their open banking acquisitions (Tink and Finicity)?

The card networks obviously have many competitive advantages that they can leverage as they scale up their pay-by-bank offerings, but one of the biggest would (I think) be their expertise in managing disputes and preventing fraud. These are areas where legacy infrastructure and regulations have often proven insufficient and where new infrastructure (i.e., faster payments) has the potential to make the problem much worse.

A different announcement from Visa – Visa Protect for A2A Payments – suggests that the company understands this and leaning into it. Smart.

Who is building bank-led identity verification in the U.S. now that EWS has blacked away from it?

Authentify, the short-lived identity verification service from Early Warning Services, seemed incredibly promising – a digital identity verification service for non-banks, powered by the KYC processes of the largest banks in the U.S.

It’s baffling to me that EWS backed away from this idea (and ran towards Paze), but I know someone else will pick it up.

I’m curious who that will be. I’ve spoken to a few folks who are working on something in this area, but would love to talk to anyone else who is working on this.

How do we enable non-customer use cases for consumer-permissioned bank transaction data?

I have no idea what the secondary use restrictions in the final rule on 1033 will look like (my guess is that they will be a bit more flexible than what was in the draft rule, but who knows).

There are obviously a lot of different use cases for consumer-permissioned bank transaction data beyond what is directly authorized by the consumer. Some of these (like passive account monitoring and cross-sell) benefit the consumer directly. Some (like analytic model development) do not, but can work with de-identified data (thus minimizing the risk to the consumer) However, the ones I’m most curious about are those that require an individual’s identifiable data, but that don’t directly benefit that individual.

One example I’ve been noodling on – loan analysis by secondary market investors. How can we enable consumer permission (for looking at cash flow data) to persist all the way through the loan securitization process? I think this would be enormously valuable for lenders and investors, but the mechanics will be tricky.

What crazy fintech idea that is currently being discussed has the best chance to become the way that things are done by the time my eldest son graduates from high school?

Something related to generative AI seems like the safest bet.

Maybe too safe?

How about the use of NFTs for real-world asset transfer? Could my son’s first home-buying experience be significantly streamlined due to distributed ledger technology? Too crazy?

- Beam was an early and very small example of what this looks like when things get messy. ↩︎

- Kiah floated the idea of the fintech industry creating a self-regulatory organization, similar to FINRA. I like this suggestion a lot. This isn’t the job of prudential banking regulators, but it’s clear (to me at least) that it’s a mistake to leave this entirely in the hands of individual fintech companies. ↩︎

- Terry Angelos, who knows a thing or two about Visa, had the most useful take that I’ve seen on Flexible Credential. ↩︎