3 FINTECH NEWS STORIES

#1: Devolve

What happened?

Evolve Bancorp was hit with a cease and desist order:

Evolve, perhaps the most prolific fintech partner bank, was hit with a wide-ranging enforcement action stemming from its 2023 safety and soundness examination by its regulators, the St. Louis Federal Reserve Bank and the Arkansas State Banking Department.

So what?

Here was my initial reaction when the news was first announced by the Federal Reserve:

And that’s still my main takeaway, to be honest – what the hell took so long?

As Jason Mikula did a good job recapping in his newsletter, Evolve’s BaaS business has been a compliance nightmare for years, and while not all regulatory enforcement actions against banks become public, it sure seems like Evolve did more than enough wrong to warrant a public enforcement action a long time ago.

But whatever. At least we have something now.

And it is quite something.

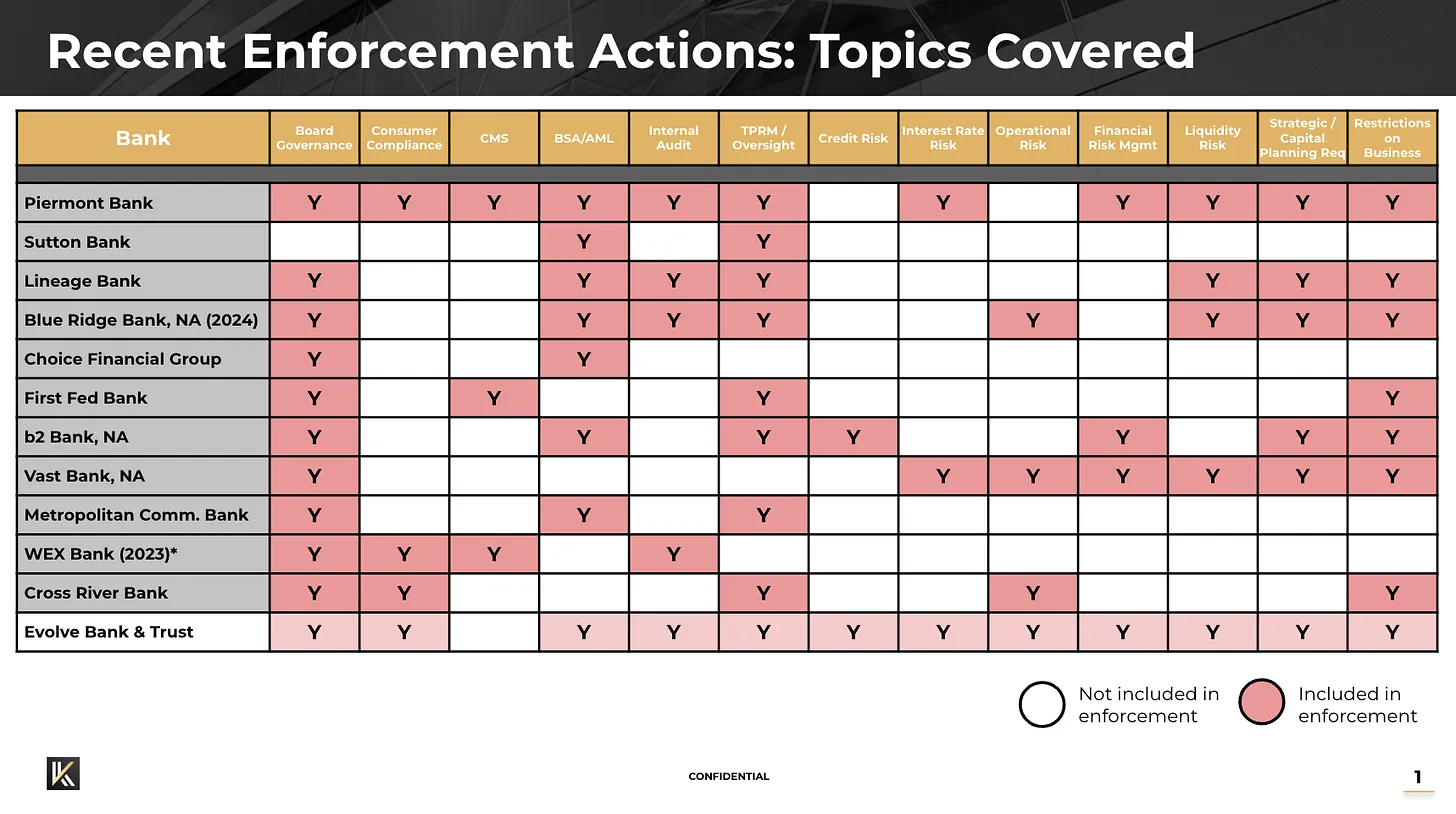

The enforcement action covers a lot of ground, more than is typical in these types of BaaS regulatory interventions, as this chart from Jonah Crane at Klaros Group illustrates:

The last column in Jonah’s chart is the one that stood out to me the most in regard to this enforcement action. The Federal Reserve will require Evolve to check with it and obtain a supervisory non-objection before it can establish any new fintech partners, subsidiaries, business lines, products, programs, services, or program managers related to Evolve’s Open Banking Division (OBD), or new products, programs, or services to an existing fintech partner, program manager, or subsidiary of OBD. Additionally, Evolve must provide supervisors with a liquidity impact analysis before exiting any existing fintech relationship.

That’s A LOT, and it will make life incredibly difficult for Evolve’s existing fintech partners, which include Mercury, Stripe, Dave, Affirm, Airwallex, Branch, Step, and Prizepool.

#2: Layer

What happened?

Plaid introduced a new product called Layer:

Layer helps you satisfy KYC requirements, link bank accounts, and onboard tens of millions of people who have saved their information with Plaid—just by collecting a phone number. Layer reduces the time it takes for someone to sign up for an app by nearly 90% by unifying identity verification and bank account linking into one secure experience.

When a customer collects and shares a user’s phone number, we’ll check if 1) they exist in the Plaid network and 2) their saved information with Plaid meets your onboarding needs with our new eligibility API. Only when both things are true, Layer is presented to the user.

This ensures users never share more information than needed and companies receive exactly the information needed to fully onboard a customer. Users who don’t meet your onboarding requirements go through your existing onboarding flow without any latency.

So what?

This is smart.

One of the big problems for all open banking data aggregators (including Plaid) is that banks and fintech companies are very reluctant to ask consumers to link their bank accounts early in the onboarding process. The concern is that asking a user to link their account at the beginning of the process risks ruining their experience (coverage and connectivity in open banking still create a lot of friction for users) and driving them to abandon the application.

This concern severely inhibits the adoption of open banking data for certain use cases, such as cash flow underwriting.

With Layer, Plaid is flipping that dynamic on its head.

Instead of asking a financial services provider to run the risk of requiring account linking for all prospective customers up front, it is dynamically presenting this fast pass-type experience only when the user has already authorized their data to be saved by Plaid during an earlier interaction with a Plaid-powered product.

Plaid is essentially leveraging the popularity of its network for back-end use cases (account verification, account funding, PFM, etc.) to bootstrap the adoption of its network for front-end use cases like KYC and credit underwriting.

#3: What Am I Missing?

What happened?

Brex launched a new version of its business bank account product in partnership with Column Bank:

Brex business accounts now benefit from new advanced security features including comprehensive fraud protection, authentication tools and built-in payment approval flows, all accessible directly from the Brex mobile app with 24/7 support via the app, by phone, or through WhatsApp. Customers can now access three distinct accounts within business accounts to:

- Confidently open accounts and transfer funds around the world with the new Checking account powered by Column N.A., with no transaction fees on ACH transfers, checks, and domestic wires – plus international wires in over 40 currencies. Opening a Checking account is easy and can be done entirely online.

- Expand spending power with an updated and fully-integrated Treasury account, making it simpler to oversee and manage funds and earn yield from day one with auto-transfer capabilities and no fees, minimum balance requirements, liquidity restrictions, or waiting periods.

- Safeguard capital with the updated Vault account, where funds are diversified across more than 20 program banks with up to $6M of total FDIC insurance (20x the national average).

So what?

This seems competitive with (if not all that differentiated from) the business bank accounts offered by other modern B2B neobanks (Mercury, Arc, etc.) Fee-free domestic wire transfers, treasury management, expanded FDIC insurance, and all the rest.

Here’s the thing I don’t get – why is Brex offering a separate Vault account for expanded FDIC insurance protection?

The Treasury account being separate makes sense. That’s an investment account, not a deposit account. It’s the place to keep funds that you know you won’t need for your day-to-day operations.

But wouldn’t it be more convenient for the expanded FDIC insurance coverage to be offered directly through the checking account, which (I imagine) is likely to be the primary operating account for the business?

Why didn’t they build it this way? The infrastructure to do this exists. In fact, it predates this wave of modern B2B neobanks by more than a decade. What’s the reasoning for having a separate vault account? Is this a Column Bank limitation? Or just an odd product design choice?

2 FINTECH CONTENT RECOMMENDATIONS

#1: Coinbase’s quest to stay profitable throughout cycles (by Jevgenijs Kazanins, Popular Fintech) 📚

Coinbase is a fintech company (if we define fintech somewhat broadly) that I spend very little time thinking about. Jev got me all caught up in this article, which focuses on how Coinbase is trying to build a more durable business model.

#2: The Crazy Economics of the World’s Most Coveted Handbag (by Carol Ryan, Wall Street Journal) 📚

This isn’t a fintech story (though I did write an essay about Birkin Bags a while back), but it’s just too good not to share.

Here’s an amazing excerpt:

The unusual economics of the Birkin have upended the normal balance of power between shopper and store worker. At the Hermès boutique, it is the buyer who kowtows. Some of the wealthiest women in the world have brought homemade cookies to the store to cozy up to their sales assistant. They have offered tickets for Beyoncé concerts, trips to the Cannes Film Festival in a private jet and even envelopes stuffed with cash—all to get their hands on a Birkin.

Capitalism is weird!