Stablecoins are the topic du jour in fintech (or the topic du semestre, to be more precise).

I usually try not to follow the crowd when it comes to topic selection for the newsletter. However, as I wrote about a month ago, crypto enthusiasts are starting to use the reputation of stablecoins (safe! low cost!) to dress up some really bad ideas. Because of this and because of the undeniable momentum that stablecoins have gained over the last 12-18 months (thanks to a combination of institutional interest from companies like PayPal, Visa, and Stripe and the election of Donald Trump), I am making an exception.

In today’s essay, I will describe the very rough framework I have cobbled together for thinking about the real value that stablecoins can provide.

One quick note before we get started — my orientation for this exercise is the belief that stablecoins (like any new financial technology) need to earn their place in the stack. It’s very dangerous to allow the wish to become the father of the thought, but I see that mental mistake constantly among crypto advocates.

The wording of this tweet is a great example:

Assuming that any technology will soon power all financial services is a mistake. Computers don’t even power all financial services activity yet, and we’ve been working on that for a lot longer than 20 years!

We shouldn’t analyze stablecoins by working backward from a desired (and highly unrealistic) end state. Instead, we should work forward, from first principles, to figure out what stablecoins are, what they can do, and what value they can uniquely provide within a financial services stack that, let’s be honest, already works quite well.

Let’s start by defining what stablecoins are.

What is a Stablecoin?

To help us with this, I will turn (as I often do) to Matt Brown, an investor at Matrix and one of my favorite fintech writers, who published an excellent overview on the topic earlier this week.

I will liberally quote Matt’s post, but please promise me you’ll read the whole thing. It’s concise and extremely useful.

The most common type of stablecoin is fiat-collateralized: one stablecoin represents and can be redeemed for one unit of fiat currency – i.e., 1 stablecoin (USDT, USDC) = 1 USD. Other variations include asset-collateralized (e.g., gold), crypto-collateralized, and algorithmic stablecoins. We’ll focus on fiat-collateralized since it’s the most common and straightforward to understand.

Stablecoins are created by issuers, who create (“mint”) or destroy (“burn”) stablecoins in exchange for fiat, and partner with others to facilitate this exchange, increasing the use and indirectly the value of their stablecoin. Issuers monetize the float on these deposits.

Issuers mint stablecoins onto various blockchains, third-party (e.g., Ethereum) or first-party (e.g., Ripple). Different blockchains offer different features and benefits, such as increased throughput or security, and many stablecoins are compatible with multiple blockchains.

Like any cryptocurrency, stablecoins can function as a store of value, a medium of exchange, and a unit of account. What makes stablecoins uniquely interesting in the crypto world is that they are comparatively safe.

Here’s Matt again, using an analogy that made me professionally jealous:

Fiat currencies like US Dollars (USD) and Euros (EUR) are issued and managed by central banks and governments, who also help create and regulate their underlying rails. This centralization makes these currencies stable and useful, but it also restricts how the rails can be used and who can use them. Think of fiat currencies as safe, comfortable, and highly desirable railway cars that ride on rails that can be slow, opaque, and inaccessible to many. There are some differences between the rail systems of different countries, but they’re generally interoperable if you have enough time and money.

The blockchain and associated decentralized infrastructure gave rise to thousands of cryptocurrencies. While the infra was fast, global, permissionless, and transparent, the currencies themselves were often too volatile to pass the major tests of money. There’s plenty of value and utility in various cryptocurrencies. Still, none of them could be used as a day-to-day transactional currency – like there’s value and utility in assets like gold, but you still wouldn’t use it for transactions daily.

If fiat currency is an old-school railway system, blockchain is a magnetic levitation (maglev) train. It was open source, permissionless, and globally available, so anyone could build their own tracks and cars. This led to many valuable and interesting new vehicles and lines. Still, few wanted to ride them regularly or on long journeys since they weren’t comfortable, reliable, or safe at first.

Because this maglev system was so new, sometimes dangerous, and certainly long-term competitive, the older rail systems made interoperability difficult. They didn’t want maglev trains riding their rails.

But it was easy enough to retrofit the older but safer and more comfortable carriages to the fast, futuristic, and global rails. That’s effectively what stablecoins are: the best of both worlds. They are reliable cars that can ride on traditional or futuristic rails, switching easily between the two and connecting different rail systems.

Stablecoins — all the stability of fiat and all of the speed, interoperability, and innovation of crypto.

Right?

Maybe! Kinda! Sometimes!

The truth is that it depends on the answer to an important question.

For Who?

After recording an excellent episode of “Not Fintech Investment Advice” (check your podcast feeds in a few weeks), Simon Taylor and I were chatting about stablecoins. He used a question to frame the discussion that I loved — For who?

This question is missing from 99% of the discourse on stablecoins.

Stablecoins are more stable!

More stable for who?

Stablecoins are cheaper!

Cheaper for who?

Stablecoins are better!

Better for who?

When you ask, “For who?” you can get to a much more nuanced and useful discussion of stablecoins’ true utility relative to existing alternatives.

So … let’s do exactly that. Let’s start asking “For who?”

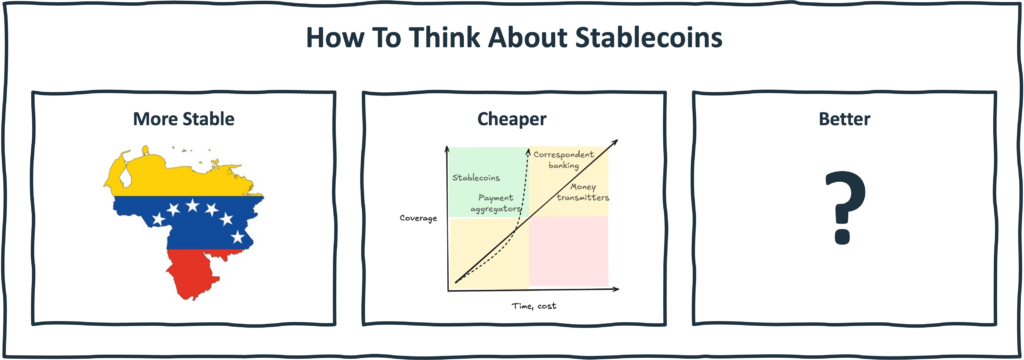

Stablecoins Are More Stable!

This is the most obvious benefit of a stablecoin (it’s right there in the name!), but it’s also the most difficult benefit to understand for those living in countries with stable monetary systems and easy access to traditional financial services.

Why would you want to store your money in a stablecoin?

Well, if you live in Venezuela, the answer is likely so apparent to you that you wouldn’t even think to ask the question.

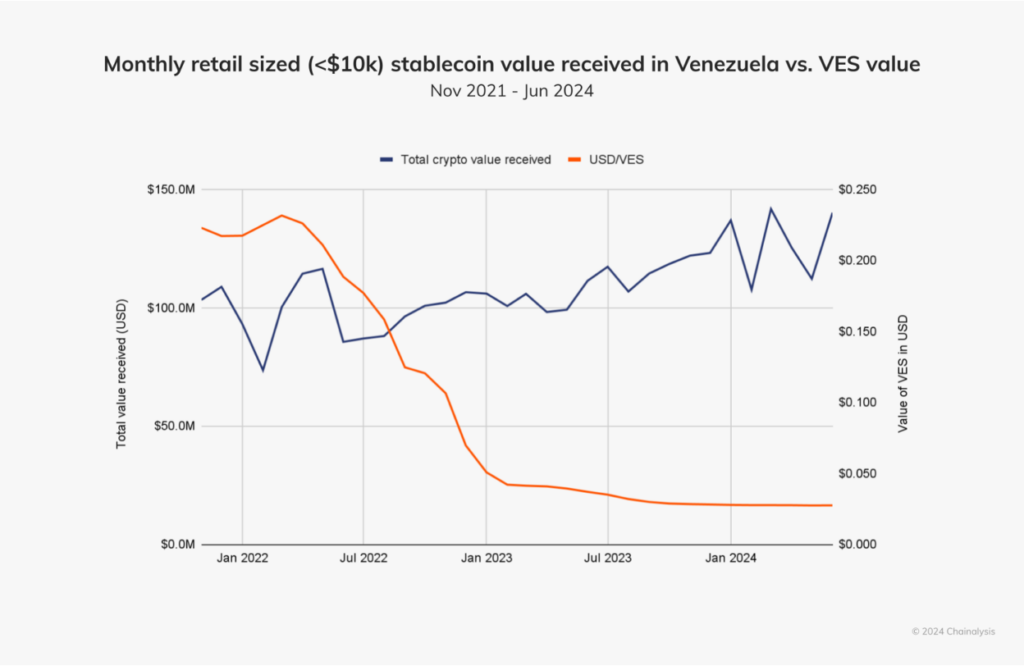

According to research by Chainalysis, Venezuela’s year-over-year growth of crypto use (110%) far exceeds that of any other country in Latin America.

What’s driving this surge in adoption?

Here’s Chainalysis:

It appears that Venezuelans are drawn to cryptocurrency to combat the plummeting value of the Venezuelan bolívar (VES). As we see below, there is a strong inverse relationship between the VES price in USD and monthly crypto value received. This is corroborated by a body of press reporting, suggesting that ordinary Venezuelans continue to seek stable stores of value and hedges against the country’s economic crisis.

Ayo Omojola, former product leader at Cash App, summarized the value prop of stablecoins in markets like Venezuela in a recent essay:

For decades, wealthy elites in poor countries have held excess savings in reserve currencies (GBP for much of the last 200 years, USD and EUR more recently) as “stable” stores of value. frequently the strategy was to hold a mix of liquid (securities) and hard assets (eg real estate in downtown London). With stablecoins anyone (and in particular, folks on the low end of the economic spectrum) in any of these countries can now save in a “stable” currency, with relatively low fees and transaction costs, regardless of their wealth level.

This is pretty transformational: in most countries you need to transact in the local currency, but it previously wasnt possible to save in non-local currency at any scale. Now it is.

It’s also worth noting that this demand for stability exists in other markets, not defined by geography. The decentralized finance (DeFi) ecosystem is a good example. Like Venezuela, the DeFi ecosystem is highly unstable. There are opportunities to trade and make money, but you want to conduct those transactions without worrying that the money you just made will disappear overnight. In a DeFi context, stablecoins provide a safe, on-chain haven for crypto traders to operate out of.

So, let’s return to our question: More stable for who?

Answer: More stable for users living or working in environments that lack an accessible and reliable store of value.

There are a couple of important caveats to that answer:

The stability of stablecoins depends heavily on the trustworthiness of the stablecoin issuers and the resilience of the blockchains the stablecoins are minted on. I’m less worried about the blockchains (particularly third-party ones like Ethereum), given that most major stablecoins are compatible with multiple blockchains. I am more worried about the stablecoin issuers, as there have been numerous examples of them failing (e.g., algorithmic stablecoins like TerraUSD), losing their peg (e.g., Circle’s USDC after the failure of Silicon Valley Bank), or just generally being shady and difficult to trust (e.g., Tether).

Countries with unstable monetary systems may dislike how much their citizens like (and use) U.S. Dollar-pegged stablecoins. Effective monetary policy depends, in large part, on having firm control over the currency that your citizens use, and if that control is weakened, it will pose an economic and political threat. If you want to see what this looks like in practice, study the recent history of Venezuela and the Maduro regime’s antagonistic and often self-serving approach to regulating the crypto market.

Be very wary of someone trying to sell the value of stability to consumers or businesses operating in already very stable environments. This is my primary concern with the stablecoin-based B2B neobank Dakota, which has argued that stablecoins are safer financial infrastructure than U.S. banks. This is, as you can read here, nonsense.

Stablecoins Are Cheaper!

This is the argument most frequently made by ill-informed crypto VCs. It goes something like this:

Merchants pay 2%-3% of every credit card transaction to Visa and Mastercard. → That’s insane. There’s no way it costs that much to facilitate that transaction. → Visa and Mastercard are ripping off merchants. Merchants will happily switch to a cheaper alternative. → Stablecoins are internet-native money. It costs $0.01-$0.10 to conduct a transaction on Solana or an Ethereum L2. → Stablecoins will inevitably destroy Visa and Mastercard.

Woof.

There are a few problematic assumptions there:

The actual “network cost” of authorizing a transaction (which is what Visa and Mastercard do) is very small and comparable to the costs of processing a transaction on a blockchain optimized for payments.

The lion’s share of the 2%-3% “merchant fee” doesn’t go to Visa and Mastercard (cue this great meme from Scott Wessman). It goes to the credit card issuers. That fee compensates the issuers for many expenses that they incur that have nothing to do with the actual payment authorization communication (electronic money movement is cheap, regardless of the type of database you use!) Nonetheless, these other expenses — customer incentives, fraud prevention, dispute management, credit risk, regulatory compliance, etc. — are essential for building and operating an effective payment network.

If you layer the same costs that credit card issuers and others in the card payments value chain incur to the base “network costs” for transactions run on Solana or an Ethereum L2, the all-in “merchant fee” that would need to be paid to use a stablecoin in place of a credit card would be as high or (more likely) higher than 2%-3%.

Very few merchants are obsessed with lowering their payment acceptance costs. Most not named Walmart and Amazon care more about facilitating commerce (which traditional payment tools like credit cards do very well). And even if merchants want to move their customers to cheaper payment rails, the customers may not want to (credit card rewards are extremely attractive).

So, does that mean that stablecoins will never be cheaper than existing payment methods? Does it mean they will never gain traction in the market by using cost as a competitive advantage?

No! It just means that you need to pick your target more carefully!

Merchants conducting domestic payment transactions over the card rails are a poor answer to the question, “Cheaper for who?”

Individuals and companies conducting cross-border payment (XBP) transactions using traditional XBP rails are a much better answer!

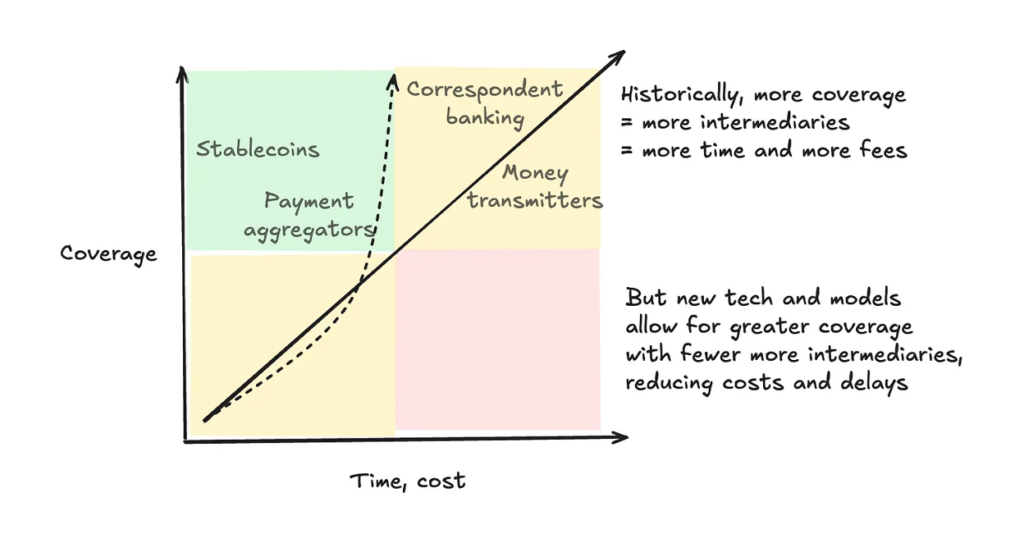

I will again rely on Matt Brown, who recently wrote a superb explainer on cross-border payments. As Matt explained in his piece, much of the $45 trillion in money that flows between parties in different countries each year uses one of three established XBP models.

I’ll attempt to very briefly explain each of the three models (but please do read Matt’s full article):

Correspondent Banking. Put simply, this is when a bank in one country opens a bank account with a bank in another country. This allows them to credit and debit payments to each other on behalf of their customers in their native currencies. The transactions are coordinated through a secure messaging system called SWIFT. Correspondent banking is dominated by a few very large banks in each of the 200+ countries SWIFT covers. In some cases, when banks don’t have direct correspondent relationships, they will go through intermediary correspondent banks that have relationships with both.

Money Transmission. This is what Western Union and MoneyGram do. It’s similar, conceptually, to correspondent banking but with a focus on serving underserved or unbanked customers across a large number of countries. The money transmitter coordinates the crediting and debiting of money from agents (convenience stores, currency exchange stalls, etc.) who interact with the senders and recipients (verifying identities, collecting and distributing cash, etc.)

Payment Aggregation. This is just a more efficient, digital version of money transmission. Rather than working with agents in different countries to collect and distribute physical cash from and to senders and recipients, a payment aggregator interacts with customers through a digital app and carries out their transactions by net settling across its own internal bank accounts, which it maintains in all the countries it supports. Wise is an example of a payment aggregator.

As Matt explains in his article, payment aggregation tends to be less expensive than correspondent banking and money transmission, which rely on expensive intermediaries:

Correspondent banking and money transmitters are often critiqued for being slow and expensive. This cost and slowness are the downsides of their broad geographic coverage, resulting from their reliance on intermediaries. Because many MT users lack formal banking, an agent network is necessary for first/last mile distribution. In contrast, the lack of 1:1 global banking connectivity necessitates the correspondent banking network for the middle mile.

Similarly, stablecoins can be used to coordinate transactions across borders instantly, at any time, with anyone with an internet connection. As such, they can provide the infrastructure to facilitate cross-border payments with comparable efficiency and coverage to what scaled-up payment aggregators like Wise have achieved.

This graphic from Matt illustrates this comparison effectively:

So, back to our question: Cheaper for who?

Answer: Cheaper for payments use cases in which the unique attributes of stablecoins (instant, always-on, global, etc.) reduce the need for expensive intermediaries.

(Editor’s Note — this tweet from Raagulan Pathy does an excellent job summarizing my key arguments on cost in a much more concise way!)

And again, there are some important caveats:

Stablecoins can help with the “middle mile” of cross-border payments — connecting senders and receivers in different countries. However, there are still a lot of costs associated with solving first and last mile distribution problems. It’s expensive to acquire and support users, comply with local regulations, and manage liquidity and FX risk. This is why Stripe bought Bridge (a cross-border stablecoin payment orchestration platform) for $1.1 billion rather than building all that first/last mile infrastructure itself. It’s also why scaled-up payment aggregators, which have already spent all the money to build coverage across countries (the middle mile), have shown little interest in stablecoins. Stablecoins aren’t cheaper than payment aggregation for cross-border payments. They simply allow the next company that wants to get into cross-border payments to reach Wise-level coverage faster.

The current costs of using USD-backed stablecoins like USDC and USDT are being subsidized by the high interest rates set by the Federal Reserve. It’s important to remember that stablecoin issuers like Circle and Tether primarily make money on the difference in the interest they pay depositors (0%) and the interest they get from the Fed on T-Bills (<4%). When rates meaningfully decrease (which might take a while!), we will see stablecoin issuers charging more to use their services and (in some cases) investing their deposits in riskier assets. These changes will negatively impact both the stability and cost advantages of stablecoins.

Stablecoins Are Better!

This is the third big argument for stablecoins, and it’s both the most compelling and the most difficult for advocates and skeptics to argue over. It’s difficult because the virtues of stablecoins as “better” financial services infrastructure can only be conclusively demonstrated by looking at the products and experiences built by developers using the “better” attributes of stablecoins, and almost none of those products and experiences exist today. It’s still mostly theoretical.

Simon Taylor has a fantastic piece coming out this Sunday on this exact topic. I’m grateful to him for sharing it with me in advance (it helped me nail down some of the details covered above), and I don’t want to spoil it for you. So I’ll just say that in his article, Simon compares the current state of stablecoins to dial-up internet in the 1990s — clearly something, but too early and too janky to say precisely what that something is.

I generally agree with this framing.

Stablecoins do have some unique(ish) attributes that have the potential to make them better for specific financial services use cases. These attributes include:

Instant and always-on. Stablecoins don’t go home in the evening. They aren’t closed on the weekends or over holidays. This is an attractive feature relative to pre-internet electronic payment infrastructure like SWIFT, which requires a lot of manual work. That said, other non-crypto rails that are always on and settle payments in real-time are starting to come online in various countries (e.g., Pix in Brazil, UPI in India, FedNow/RTP in the U.S.), so this isn’t a uniquely better attribute for stablecoins (though stablecoins could be the infrastructure that links these different domestic real-time payment networks together … TBD). Additionally, as many of the citizens in these countries have learned in recent years, faster payments = faster fraud. This will be true (perhaps especially true) for stablecoins as well.

Global by default. We already covered this one when talking about cross-border payments. It took Wise a long time to build global coverage for its service. The next Wise will be able to get there much faster using stablecoins. Ayo Omojola made a similar point in his piece regarding domestic fintech apps with global aspirations, “By providing USD balances to KYC-ed consumers around the world, digital wallets like Cash App and Venmo might have been able to reach global scale without having to invest in local stored balance infrastructure in each country.” All true; however, as I noted when discussing XBP, stablecoins don’t solve for last-mile delivery problems like compliance, especially if the end customer wants access to their funds in their local fiat currency.

Transparent by default. Criminals’ crypto use tends to mirror legitimate crypto users’ preferences and behavior. Until 2021, criminals rarely used stablecoins. However, just as legitimate users began to appreciate the hybrid fiat/crypto value of stablecoins for non-speculative use cases in the wake of the last crypto crash, a similar shift in thinking played out in the criminal underworld. According to Chainalysis, in 2022, the number of wallets holding stablecoins associated with illicit activity surpassed those holding illicit bitcoin for the first time. This trend accelerated in 2023 and (I’m guessing) in 2024. Turns out the bad guys also appreciate a stable, global, instant, and always-on mechanism for transacting! However, one thing that is true of all blockchain-based transactions (including those made with stablecoins) is that they are far easier to trace than their TradFi equivalents. One wonders if government officials responsible for monitoring money laundering are quietly appreciative of stablecoins’ potential to get and keep financial crime on-chain.

Programmable. “Code is law” is a prevalent mental model in crypto, meant to convey that anything permitted by a smart contract on a blockchain is “legal.” While this model is (rightly) rejected by regulators, it does hint at another possible advantage of stablecoins relative to TradFi alternatives — they can have automated rules baked into them. The potential of “programmable payments” for things like risk management and compliance is intriguing, though highly theoretical at this point.

I think it’s too early to have a concrete answer to our question. However, in the future, when you hear someone say, “Stablecoins are better!” make sure to ask them, “better for who?”

A Very Rough Framework

So, that’s my framework for thinking about stablecoins.

More questions than answers at this point, but hopefully it’s helpful!

If you are interested in learning more about stablecoins, I thought it would be useful to include the links to all the resources I cited throughout the essay (plus a few additional ones):

Stablecoins aren’t cheaper; they’re better — by Simon Taylor (This comes out on Sunday, so mark your calendars. Here’s the link to Simon’s newsletter, Fintech Brainfood.)

Tokenized — by Simon Taylor and Cuy Sheffield (This podcast has been a very valuable resource for me on all things crypto, especially stablecoins.)

Cross-border payments in ~1,000 words — By Matt Brown (This one is worth perusing if you want to understand more about how the XBP models I briefly described actually work.)

A Very Stable Conference (This is an event being put on by Ayo and Aaron Frank on February 12th, and it looks like it’ll be worth attending if you are building in this space or thinking about it.)

Created By

Alex Johnson

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

THe Fintech Takes Newsletter

Get breakdowns of the latest product launches, funding, acquisitions, and crypto news delivered to your inbox twice a week.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.