3 Fintech News Stories

#1: Closing the Homeownership Gap

What happened?

Fannie Mae and Freddie Mac are making some important and long overdue changes:

Fannie Mae and Freddie Mac are implementing big reforms aimed at helping disadvantaged communities become homeowners and making sure homebuyers of color stay owners.

The initiative from the two federally backed home mortgage companies announced Wednesday is the most sweeping overhaul since the housing crash in 2008. Some of the big-ticket items exclusively reviewed by USA TODAY include assistance with down payments, reserve funding for homeowners’ emergencies and lower mortgage insurance premiums.

Fannie Mae and Freddie Mac are also rolling out a new credit reporting system that factors rent payments into creditworthiness scores, one of the biggest systemic barriers experts say keep renters of color from being able to purchase a home.

So what?

Here are some facts:

- “Together with the Federal Housing Administration and Department of Veterans Affairs, Fannie Mae and Freddie Mac directly or indirectly guarantee 70% of single-family mortgage origination.”

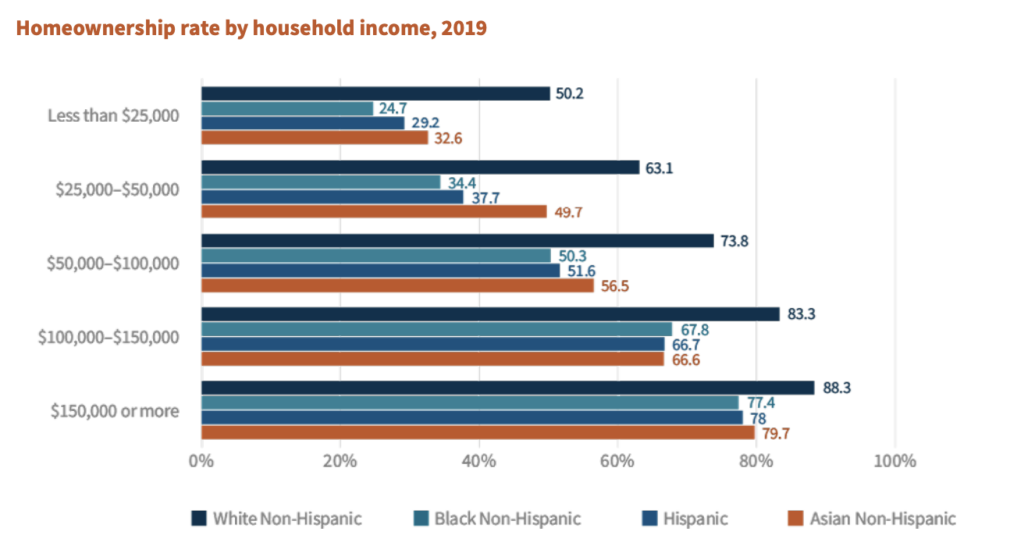

- “The median net worth of white families who are homeowners was $300,000, of which $130,000 was attributed to housing, according to the 2019 Survey of Consumer Finance, the most recently available. That number decreases to $113,000 for Black families who are homeowners, of which $67,000 is derived from home equity. And for Latino families, roughly $95,000 of their median net worth of $165,000 is tied to owning a home.”

- “the gap in homeownership rates between Black and white families is bigger today than when segregation was legal, according to a study by the Urban Institute. About 71% of white Americans own homes, compared with 41% of Black Americans.”

What does all that mean?

Homeownership is a key lever for building wealth. Access to homeownership has, historically, been denied to Black people in this country because of racist practices like redlining. Outlawing those racist practices didn’t, by itself, create equal access to homeownership for all Americans (in fact, the homeownership gap between black and white families has continued to grow). Fannie Mae and Freddie Mac occupy a uniquely important position within the housing ecosystem, from which to effect change.

These reforms are a very good thing.

Ohh, and one more interesting piece of news tucked inside in this announcement:

[Fannie Mae will] implement cash-flow underwriting into DU [Desktop Underwriter] by Q4 2022 for borrowers without a credit score.

The adoption of cash-flow underwriting (powered by open banking) is a huge deal. Traditionally, this form of underwriting has been used to approve credit invisible consumers for shorter-term, smaller dollar loans (unsecured installment loans, credit cards, etc.) where ‘ability to pay’ is more important than ‘willingness to pay’. Fannie Mae signaling its comfort with cash-flow underwriting for mortgages (where ‘willingness to pay’ signals have traditionally been of utmost importance to underwriters) is a big vote of confidence.

#2: BNPL Breakout

What happened?

Apple announced a new service:

During its WWDC speech, Apple announced a new service called Apple Pay Later that will allow consumers to make mobile and online purchases sliced into four payments over six weeks at the millions of U.S. retailers that already accept Apple Pay. The offering won’t include fees or other charges, the company said, requiring only a “soft” credit check and review of the user’s transaction history with Apple.

Join Fintech Takes, Your One-Stop-Shop for Navigating the Fintech Universe.

Over 36,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

So what?

As I wrote about a while back, Apple wants to make money in financial services. Real money. This isn’t just about selling more iPhones or making the Apple ecosystem slightly stickier.

How do I know that?

According to the latest reporting from CNBC (and in contradiction to earlier reporting from Bloomberg), Apple is doing the credit decisioning for this pay-in-4 service itself and is making the loans off of its own balance sheet through a wholly owned subsidiary that has obtained lending licenses in most U.S. states.

This is a huge risk. Lending comes with a lot of risks — credit risk (will Apple stick to just approving prime credit customers or will it try and extend this service to near-prime and credit invisible customers?), regulatory risk (the Director of the CFPB, a noted skeptic of big tech, must licking his chops at the news that Apple is directly doing the lending for this service), and reputational risk (I doubt that Apple is going to try and collect on any missed payments for this service because the reputational hit alone wouldn’t be worth it, but we’ll see).

Apple taking this risk tells us just how important financial services is to its future.

#3: A Nation with a Real (Bad) Economy

What happened?

The play-to-earn revolution, ushered in by Sky Mavis (creator of Axie Infinity), isn’t going great, as illustrated by one Axie breeder named Alejo Lopez de Armentia:

Armentia didn’t try to sugarcoat his performance to date. Popping open a sprawling spreadsheet he used to track his Axie operations, he determined that he could theoretically cash out his cryptocurrencies for a $5,000 profit, without touching the 100 or so Axies he was holding. “I’ve been at it since August, so $5,000 in that many months is not something to be proud of, right?” he said. “I could’ve worked at McDonald’s and made more.” But then he gave me his projections for the crypto markets—AXS, he said, would rise to $150 by May. He changed a few cells to account for these predictions, and suddenly his venture did indeed seem more lucrative than flipping burgers.

When the end of May actually came, AXS was at about $23. Armentia estimated his Axie investment was down about $15,000 but said he didn’t know for sure because he’d stopped looking at the spreadsheet.

So what?

Sky Mavis once wrote that “You can think of Axie as a nation with a real economy.”

In a sense, this is true. A lot of people (including Mr. Armentia) have tried to make a living by pouring all of their time into ‘playing’ Axie Infinity.

The trouble is that the game isn’t actually fun to play. This matters because the economy that Sky Mavis designed (and that lots of investors like Andreessen Horowitz have invested in) only functions if a steady supply of new players start playing the game.

This was an easy problem to see coming, as I wrote last year:

At a fundamental level, the in-game tokens are only valuable to the extent that there is demand from new players for them right? What happens when people get tired of playing the game or move on to something new (which isn’t, like, unheard of in the video game world)?

2 Things to Read and/or Listen To

#1: Fintech Layer Cake (by Matt Janiga & Reggie Young, Lithic)

Lithic has seemingly cornered the market on smart fintech regulatory/compliance brains and now those brains have teamed up to create a podcast — Fintech Layer Cake.

I learned a ton from episode 1 — Compliance 101 — and I’m 100% confident that I’ll find future episodes to be just as valuable. This is one of those recommendations from me that meets the coveted Ron Swanson level — it’s a guarantee.

#2: Predictably Unpredictable: Navigating the Volatility of Transactional Revenue (by Medha Agarwal and Emily Man, Redpoint Ventures)

As a general rule, I try to read everything that Emily Man writes. It’s smart stuff.

This article does a great job explaining the deteriorating performance of public fintech companies by illustrating the underlying characteristics of most B2C fintech companies’ business models and how those business models benefited enormously (but not permanently) from pandemic tailwinds.

The article also puts a fine point on an argument that I’ve been making for a while — fintech companies aren’t SaaS companies:

Fintech founders often say that their revenue is not technically SaaS because while it is not recurring, it is SaaS-like because it behaves predictably month over month in aggregate across their customer base at scale. While there are certainly elements of truth to this, the data above shows that this is likely to be the exception and not the rule.

1 Question to Ponder

#1: I’m outsourcing this week’s question to the CEO of Plaid, who asked this on Twitter last week:

If you have thoughts on this question that you didn’t already share on Twitter, please DM me on Twitter or LinkedIn.