Editor’s Note — This article is sponsored by LoanPro and is the third and final article in a series exploring trends in the credit card market (check out Part 1 and Part 2). As with all sponsored content in Fintech Takes, this article was written, edited, and published by me, Alex Johnson. I hope you enjoy it!

I ended the second article in this series with a prediction:

Over the past five years, regulatory pressure and customer demands have ushered in a new modular approach to launching a credit card, where a card issuer can deconstruct aspects of the card technology stack and ecosystem for their benefit.

This is the more difficult path, but it has become significantly easier over the last 5 years, and my hypothesis is that it will become a much more popular path for companies aspiring to make the U.S. credit card market a more competitive place over the next 10 years.

It’s never been easier to build a credit card, from scratch, than it is today.

That’s not to say that it’s easy. It’s not. Just because the pieces are available to assemble your own proprietary credit card “stack” doesn’t mean the assembly process is straightforward.

But that’s OK!

As Tom Thibodeau likes to say, “The magic is in the work.” Doing stuff that’s hard is how you build competitive differentiation and positive unit economics.

So, in this article, I will outline the main steps for building a credit card, leveraging the abundance of modular infrastructure and partners that are now available.

Start With Why

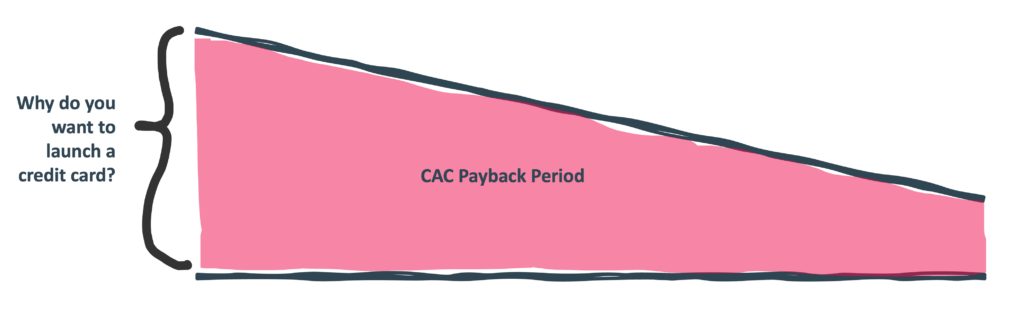

Before we get into the nitty-gritty, it’s worth stepping back and asking yourself a more fundamental question — why do you want to launch a credit card?

This question is important because your motivation for launching a card will determine, in large part, the best approach for how you want to go about building it.

Is the card going to be your first product? Or is it a product that you are going to cross-sell to your existing customers? Is the primary purpose of the card to generate revenue with a healthy profit margin? Or is it to increase share of wallet and/or improve customer retention?

There are no right or wrong answers to these questions, but it’s important to ask them and to be honest in your answers.

If you are planning to make the credit card your initial wedge product, you will need to think very carefully about how you are going to compete with the products offered by the top five issuers (Chase, American Express, Citi, Capital One, and Bank of America), which control 70% of the market. Product differentiation is crucial in this case, because you do not want to get into a CAC war with these behemoths.

If the purpose of your credit card is to generate revenue with a healthy profit margin (and this is a very common reason why fintech companies and non-finance brands launch credit cards), you will need to be incredibly disciplined in choosing the different modules for your product stack, to ensure that your unit economics will work and will improve as you scale up.

Start with why. Then work backwards into the how.

Now, let’s talk about the how.

| Sponsored by LoanPro If card program managers want to win in a highly competitive market, you need a product that doesn’t look like every other card out there. You need personalization to win. LoanPro enables you to tailor each card to your customers, from transaction-level credit to pre-built servicing workflows to flexible repayment schedules. LoanPro has the modern infrastructure to enable you to win market share. |

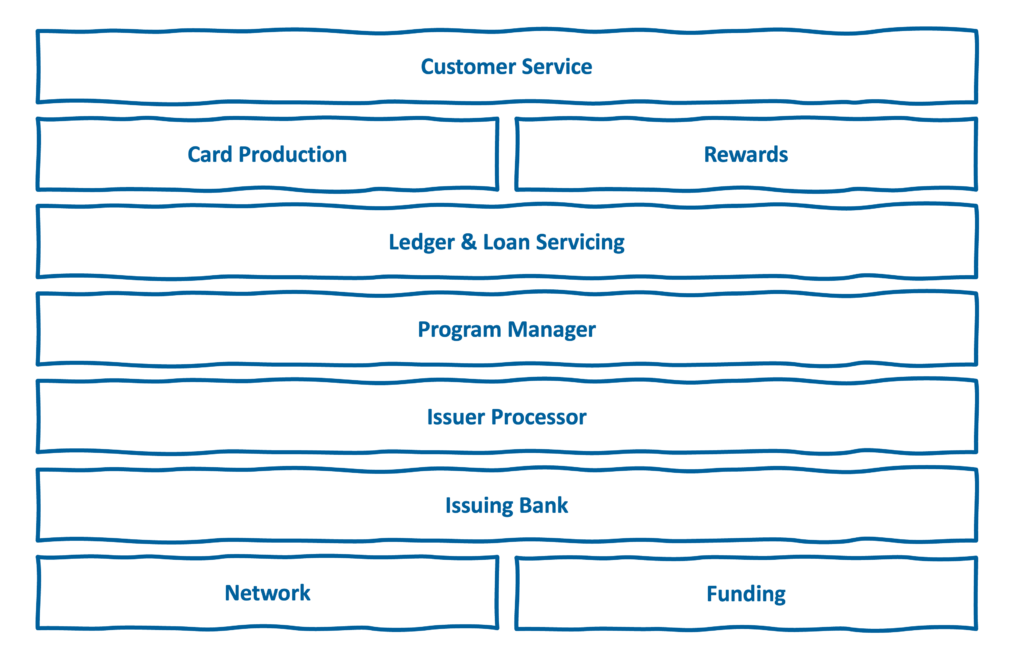

The Stack

Here are the primary modules in a credit card stack:

This isn’t a comprehensive list of every single component required to build, launch, and manage a credit card, but these are the big ones. Let’s talk through each briefly.

Network

Theoretically, the options here include Visa, Mastercard, American Express, and Discover, although almost all issuers go with either Visa or Mastercard. If your product is sufficiently attractive to the networks, they may offer you incentives to choose them. They may also bundle these incentives with services delivered in other parts of the stack (such as processing, see below).

Funding

Fintech companies and non-finance brands issuing cards don’t have access to customer deposits to fund their credit card lines. So, they must line up funding from private credit firms or other investors. This is generally one of the biggest cost drivers in a credit card program, especially when the program is first starting and doesn’t have any portfolio performance history. Fortunately, the private credit space is booming right now, with players like Fortress, Keystone Financial, Moore Capital, SoundPoint Capital, Victory Park Capital, and Encina Private Credit. Some banks (like Cross River Bank) also provide funding, which they may bundle in if you choose them as your issuing bank to provide BIN sponsorship.

Issuing Bank

Credit cards in the U.S. market must be issued by a financial institution, even if it’s being done on behalf of a fintech company or non-finance brand. That means you need a partner bank. There are a lot of banks to choose from — Coastal Community Bank, Column Bank, Continental Bank, Cross River Bank, FinWise Bank, WebBank, First Electronic Bank, TAB Bank, Pathward Bank, Focus Bank, Celtic Bank, Bancorp Bank — to name just a few. However, what you will find is that many banks will be easy to cross off of your list because your product concept and target customer base aren’t a fit with their business goals and risk tolerance. When choosing between the banks that are left, resist the temptation to make the decision solely about price. Your bank partner is existentially important, and it isn’t worth taking risks here to save a few basis points.

Issuer Processor

The issuer processor is the integration layer between the issuing bank and the card networks. It creates accounts and authorizes and settles payment transactions. This area of the stack has become significantly more competitive over the last 20 years, with modern issuer processors like Lithic, Highnote, and Stripe gaining traction with companies that opt for modularity over the all-in-one approach to launching a credit card. Visa also has an issuer processor (Visa DPS), which they will bundle together with network incentives for programs that they really want to win. If your product depends on sophisticated authorization and spend control capabilities, it might be worth paying a bit more for this module. If not, this can be an area to save on costs.

Program Manager

Every credit card program requires program management, which is a catch-all term for all the work that needs to be done to design, launch, and manage the ongoing operations, compliance, and risks of a card program. If you have opted to build your own credit card program rather than go with an all-in-one provider (like Cardless or Marqeta), this will typically be work that you do in-house, although there are excellent external consultants like iLEX, SightSpan, and FS Vector who can help you figure it out.

Ledger & Servicing

This is the nerve center of the credit card stack. This system is responsible for tracking all card issuing and payment processing activity, and functioning as the single source of truth for the issuer. As a loan product, credit cards also require a system that can track payments and calculate outstanding balances and interest. It can be tempting to build ledgers and servicing systems internally (your engineers will always say they can do it), but there’s a surprising amount of nuance that isn’t obvious (unless you’ve done it before), and the fault tolerance in this area is extremely low. For example, if a cardholder gets deployed to active duty, you are required, according to the Service Member Civil Relief Act (SCRA), to lower their interest rate to 6%, and depending on their start date of service, you may be required to backdate this interest rate adjustment. For these and many other reasons, usually, it’s best to work with an established provider that specializes in this module, like LoanPro.

Card Production

Despite steady growth in digital wallet adoption and use, credit cards are still physical products at the end of the day. You will need to work with a company like CPI, ABCorp, TAG Systems, or Arroweye Solutions to print, package, and ship physical cards. Beware of up-sells in this area. You can spend a lot more than you think trying to create an impressive-looking card.

Rewards

Many credit card customers expect rewards, and building a rewards and loyalty program from scratch is a heavy lift. It might be worth it if rewards are a key part of your competitive differentiation (although beware of going head-to-head with the big issuers in this area). If not, opting for an external partner like ampliFI or Kard might make more sense.

Customer Service

Competing in the credit card market requires a significant investment in customer service. You need a phone number that customers can call when they inevitably have questions or problems that can’t be solved with a chatbot or FAQ section on a website. You need a call center with customer service reps who are trained to respond to these questions and resolve these problems, while remaining in full compliance with all applicable regulations (which are especially strict regarding chargebacks and dispute management). There are lots of service providers that specialize in business process outsourcing for credit card customer service, including Alorica, Ubiquity, CardWorks Servicing, Bill Gosling, Firstsource, and Genpact.

| Sponsored by LoanPro Between CFPB chaos, the Hawley/Sanders proposed 10% rate cap, and new state-level regulations, compliance in 2025 might go in a dozen different directions. Are your credit and lending operations ready to adapt to rapid regulatory changes? LoanPro can help you adjust your strategy, making compliance the default. Reach out to our team of experts here. |

How to Assemble The Stack

So, those are all the pieces of the puzzle.

The last question we need to answer is, how do you assemble them?

There’s not a specific answer I can give you here, because it depends on your goals for your credit card program and the choices you make at every level of the stack.

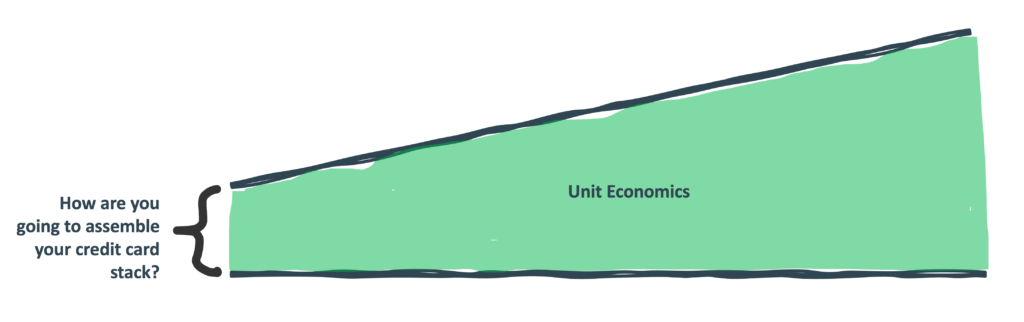

However, I can offer a guiding principle — your unit economics are your destiny.

There are a lot of unknowns in launching a credit card. The truth is that your success isn’t entirely under your control. It is subject to a lot of macro factors (interest rates, credit environment, regulation, competition, etc.) that can’t be controlled or even sometimes predicted.

That’s why it’s so important to focus on your unit economics. That is something that you can control!

If you can build a product that generates a (small) profit even when those macro factors are unfavorable, you will be well-positioned to weather storms and thrive once the clouds clear.

A good way of thinking about how this principle applies to credit cards is spend margin, the amount of money you make or lose on the payments side, without factoring in revenue or losses on the lending side. If you can assemble your credit card stack so your product has a positive margin on spend alone, you will be in a strong starting position.

How do you do that?

The focus should be on two main areas at the beginning.

First, how do you drive down costs as much as possible? Unless it’s a key area of competitive differentiation or a job-to-be-done that’s extremely risky to screw up (like ledgering and servicing or picking the wrong bank partner), do whatever you can to save money.

Second, find differentiating aspects of your card program that increase top-of-wallet spend. You need to find a way to stand out in a highly competitive market, and personalization can be a great way to do so.

Building a profitable credit card business is, fundamentally, a race between two different metrics that will move in the opposite direction.

On the customer acquisition side, your margin (i.e., CAC payback period) will get worse as you scale up and transition from cross-selling to existing customers (if the credit card is an add-on product) or product-led growth (if the credit card is your wedge product) to competing with the big, established issuers for net-new mass market customers. Having a good answer to the “why do you want to launch a credit card?” question will help ensure you are starting in the best possible position here.

On the operations side, your margin (i.e., unit economics) will improve as you scale up. More volume will allow you to negotiate better prices with your transactional service providers (ideally, you want to already have this baked into your contracts), and more experience operating the program (and the data that comes with that experience) will improve your ability to mitigate fraud and secure better-priced funding for your loans. Having a good answer to the “how are you going to assemble your credit card stack?” question will help ensure you are starting in the best possible position here.

The Opportunity

Gen Z’s enthusiastic embrace of credit cards, combined with the progress that we have made over the last two decades in building more modular infrastructure for launching and managing credit card programs, has created an unprecedented opportunity for fintech companies and non-finance brands to challenge the biggest credit card issuers.

Seizing that opportunity won’t be easy, but it is possible.