3 Fintech News Stories

#1: Totem

What happened?

A new neobank focused on serving Native Americans was announced:

[Amber Buker, member of the Choctaw tribe] and Richard Chance, a member of the Cherokee tribe, co-founded Totem, a neobank designed to serve the needs of the growing Native American market

Totem stands out from many other neobanks because of how Buker and Chance plan to generate earnings. Many depend heavily on the interchange income from their debit or credit cards. Totem plans to offer a debit card as well as a credit-builder credit card, but that won’t be its sole means of support.

Many tribes offer extensive benefits programs to members coming to millions of dollars in some cases — remember Buker’s quest for that downpayment — but running those programs can present challenges for tribes. The challenges include making benefits easy to find, and some are on the back-end, getting funds from tribe to member in the most efficient and least-expensive way.

Totem hopes to work with numerous tribes to bring their benefit lineup into the app itself

So what?

Niche neobanks focused on serving a specific community are a challenging proposition. To do it well, you need:

- A tight-knit community that is durable and efficient to market to.

- A community with unique, unsolved financial services challenges.

- A plan for making money, above and beyond debit interchange.

Totem has all three of these boxes checked.

What a great idea. I’m rooting for this one.

#2: Read/Write Access & Irreversibility Don’t Mix Well

What happened?

Plaid added support for several leading cryptocurrency exchanges:

Plaid … today announced that it’s adding support for leading crypto exchanges to its data network. While Plaid previously integrated with large exchanges on an ad hoc basis, the move is an indication that the company sees crypto as important to its growth.

As of today, through Plaid, users can share crypto account information, including asset types, balances and transactions with other services they use. Developers can incorporate the data through the Plaid Investments API, which now supports crypto accounts for use cases like tax advisory services, financial planning and net worth calculations.

Binance.US, Kraken and Gemini are among the newly integrated exchanges. Support for additional platforms including Blockchain.com and BitGo is planned for later this year

So what?

Sign up for Fintech Takes, your one-stop-shop for navigating the fintech universe.

Over 41,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Crypto is an obvious area of expansion for the data aggregators given its growing importance in many consumers’ financial portfolios (although the data being aggregated today is likely to just bum out those consumers … but I digress).

The interesting bit to me is that this consumer-permissioned access is apparently read-only:

Plaid’s newly introduced support for crypto accounts is read-only, meaning developers don’t have access to move money on behalf of users. In addition, he said, all crypto exchanges had to go through a due diligence and risk assessment process by Plaid’s risk team before joining the Plaid network.

Ohh right! Crypto is filled with scams and fraudsters and the transactions are irreversible.

Read/write access is universally seen, within the world of open banking, to be superior to read-only access. The ability to initiate transactions is a really powerful capability in the hands of developers (see, for example, what’s being built in the world of payroll APIs). But we can’t enable that capability in crypto without running the very real risk that all of our customers’ money would get stolen. Shoot!

#3: This is Getting Abstract

What happened?

A new fintech Infrastructure-for-Infrastructure-as-a-Service (IfIaaS?) launched a public Beta program:

Quiltt is wrapping its warm low-code fintech infrastructure blanket around startups and small businesses that want to create financial services for their customers, but don’t have the budget resources for a big engineering team.

[Quiltt] includes API integrations with fintech providers, like Plaid, Spade and ApexEdge, and a suite of no-code user interface modules for users to experiment with on top of its data platform.

The company is also building out some bonus adds, like billing and subscription management, so that users can start with off-the-shelf, white-label apps and then transition to more specialized offerings when needed, or when they want to control the full experience without interrupting its back end data or services

So what?

Let’s say you wanted to build a consumer-facing fintech app, but you aren’t an engineer (nor do you have any hired yet), and you don’t know the first thing about all these APIs and BPIs and CPIs. There’s a panoply of fintech infrastructure — the exact tools that you need — sitting right in front of you, but you’re not qualified to pick any of it up.

What do you do?

Well, apparently, you use Quiltt (A+ name, BTW).

I haven’t seen anything like this before. It appears to be an abstraction layer sitting on top of the many abstraction layers that have already been built in this golden age of fintech infrastructure, which allows non-engineers to drag and drop their way into a fully-featured fintech app.

How strange. How wonderfully strange.

2 Fintech Content Recommendations

#1: Predictably Bad Investments: Evidence from Venture Capitalists (Diag Davenport, University of Chicago)

Diag Davenport, a behavioral science PhD student at the University of Chicago, wrote a fascinating paper.

He studied 16,000 startups (representing over $9 billion in investments) using machine learning to evaluate the decisions of early-stage investors. His analysis showed that approximately half of the investments were predictably bad, meaning that they could have been avoided if investors had relied on information known at the time of investment. The cost of these poor investments was over $900 million.

And what was the biggest contributing factor to these poor investment decisions?

An over-reliance on founders’ backgrounds and prior experiences.

In my essay last week, I wrote about the need to bring more diverse, less experienced founders into fintech. Mr. Davenport’s paper suggests there’s very little downside to doing exactly that.

#2: Clubhouse Isn’t Dead Yet (Kaya Yurieff, The Information)

OK, first a confession — I still kinda like Clubhouse. I don’t go on it a ton anymore, mostly because a lot of creators have fled from the platform, but I think the app itself is actually pretty good. And I give them a lot of points for being first into a new product category that seems to have some legs.

Second, I thought this reporting from Kaya Yurieff on Clubhouse’s healthy cash reserves and modest burn rate was interesting. It sounds like the company is positioned to try and make a comeback.

Will Clubhouse succeed?

That’s a question that every consumer-facing fintech company that saw explosive, but temporary growth during the pandemic and has managed its burn rate relatively well should care about the answer to.

1 Question to Ponder

#1: Which fintech companies are best at recruiting remote talent (especially in highly creative and specialized fields) and what makes them so good at it?

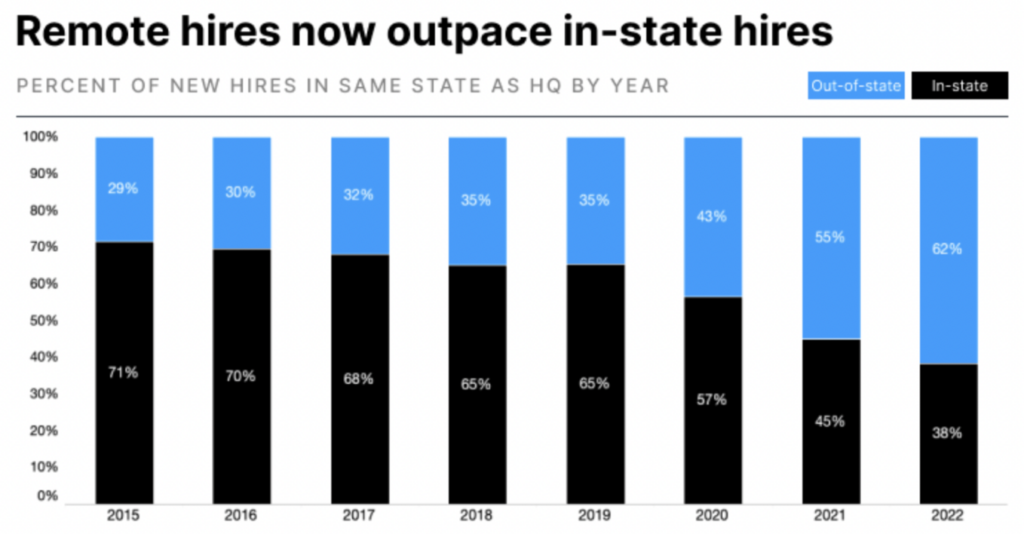

Last year, for the first time in recent history, the number of remote hires at venture-backed companies outpaced the number of in-state hires. In 2022, this trend is expected to continue to accelerate.

This change masked a more important shift — away from full-time work to more creative, project-based work where specific skill sets are only needed for short periods of time (apparently this is a very common employment model in Hollywood).

I’m curious how fintech (and banking) might adapt to these changes. What approaches to recruiting and retaining talent will work best? Are there particular models already in use (accelerators, communities like Cambrian Fintech, etc.) or being built right now (Twali) that will be particularly successful in this new environment?

If you have thoughts on this question or examples of companies and/or specific HR folks doing this really well already, please DM me on Twitter or LinkedIn.